By: Olivia Engel, CFA, CIO, Active Quantitative Equity, State Street

“We just pick good stocks.” This short phrase encapsulates an investment approach that worked so well for so long that it avoided scrutiny. In Active Quantitative Equity (AQE), our process for picking “good stocks” typically translates into identifying reasonably valued, high-quality companies that have an improving earnings outlook.

In my February commentary I cautioned investors against letting macro trends distract them from a focus on fundamentals, and in March I noted some of sector trends that we have been following that are powerful enough to buck macro trends during extreme market conditions. For a balanced view, it is also important to understand how AQE’s thinking acknowledges and incorporates the impact of macro trends on equities – an impact that has been rising for quite a long while.

Evolving Landscape

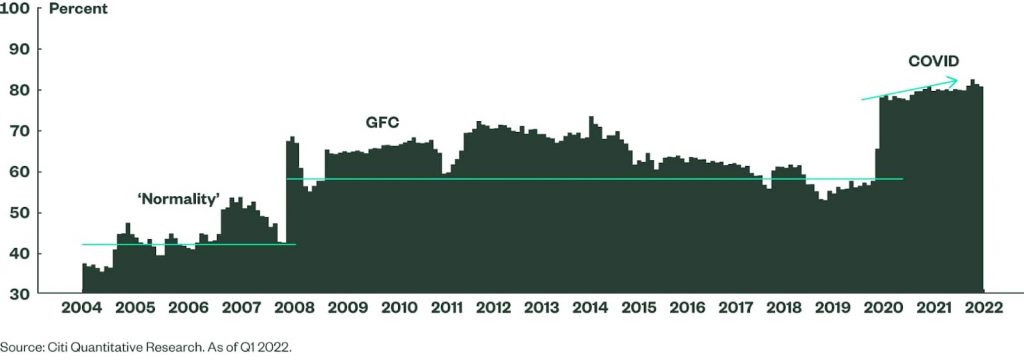

The policy moves triggered by the Global Financial Crisis, the COVID-19 pandemic, and now the Russia-Ukraine War appear to have changed the influence that macro factors typically have on the investing landscape. Figure 1 tracks the evolution in the amount of stock volatility that can be explained by general macro factors. Currently, over 80% of the variance in equities can be explained by factors such as interest rates, credit spreads, and oil/commodity prices. In effect, the three “C’s” of Crisis, COVID, and Conflict have upended traditional analysis of stock risks. A fourth “C,” Climate, is on the horizon as well, with impacts we are assessing. Investors may hope for a return to the halcyon days when stock picking was everything and the only thing, but we don’t see that happening soon.

Figure 1: Macro Factors Are Dominating Stock Risks

Percentage of Stock Volatility that Can Be Explained by General Macro Factors

Takeaways for Today

For example, in the context of the current macro environment, it is important that investors be careful about their inflation hedges. While the recent data point on inflation is indeed eye-catching, traditional inflation hedges are starting to get pricey. If the medium-term gauges of inflation are correct (most notably, the 5-Year, 5-Year Forward Inflation Expectation rate), investors should be careful how they use equities to balance inflation risks. It may take longer, or require higher changes in price levels, to get rewarded.

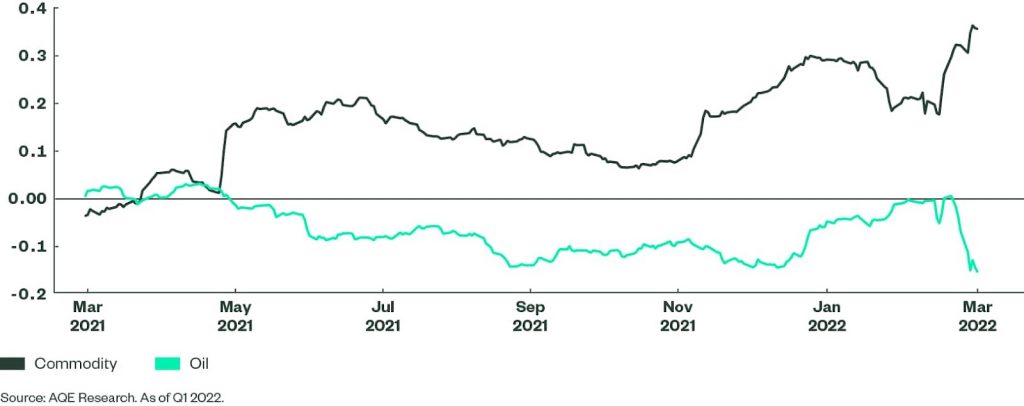

We still like most commodity plays (preferring industrial commodities over oil), but the easy money has already been made here. Figure 2 shows the correlation of AQE’s investment signals and the Axioma Oil and Commodity factors. Oil, in particular, has become a riskier segment of the market and is our least preferred inflation hedge. The Russia-Ukraine War has been dominating related headlines, but COVID shutdowns in China and renewed diplomacy with Iran/Venezuela/Libya to bring on new oil supply have dampened the upward moves. The supply/demand balance may well remain fragile.

Figure 2: Where Oil and Commodity Investment Signals Are Pointing

Correlation of AQE Investment Signals and the Axioma Oil and Commodity Factors

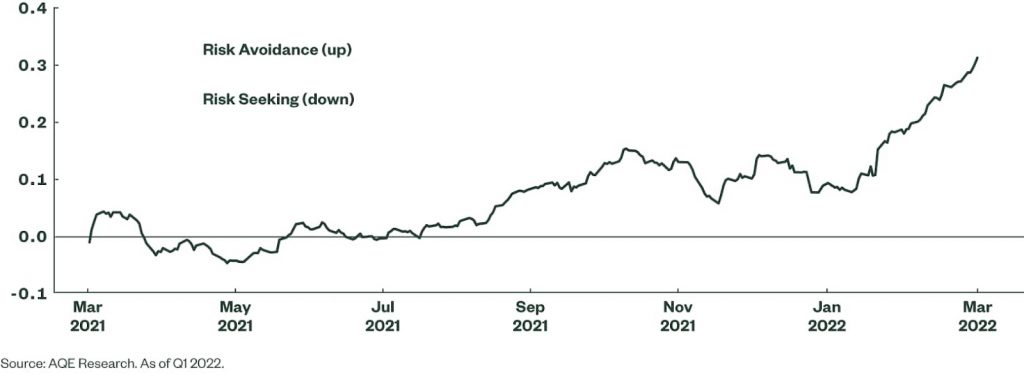

Our models also suggest a more defensive (lower risk) positioning in this environment, which seems appropriate given the rising level of macro risks we are seeing. Figure 3 shows the correlation of our investment signals and the investment grade corporate bond spread. It appears from this analysis that the fixed income markets are suggesting more risk, and the equity market (overall) is just coming to this realization. It is interesting to note that our model suggested a more defensive positioning even prior to the invasion of Ukraine.

Figure 3: Time to Win by Not Losing

Correlation of AQE Investment Signals and the IG Corporate Bond Spread

The Bottom Line

It is clear that macro trends will continue to influence markets, and AQE’s models are adjusting to this reality – even as we continue to focus on identifying outperforming sectors and companies. It is also clear that macro’s importance will be elevated for a while, so we are working carefully on evaluating and then balancing the risks as we see them. For example, we keep our inflation risks contained by having some commodity positioning, but if economic and earnings growth falter we are covered through our avoidance of credit exposure.

Adaptation, diversification, and assimilation of new investing styles and skills will always be needed to keep pace with market realities, particularly in the AQE space. We are meeting that challenge daily.

This post first appeared on April 22, 2022 on the State Street Global Advisors blog

PHOTO CREDIT: https://www.shutterstock.com/g/Myndziakvideo

Via SHUTTERSTOCK

DISCLOSURE

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit nor guarantee against a loss.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.

{kind=link}