By:Elliot Hentov, Ph.D., Head of Policy Research

In this latest commentary on the Russia-Ukraine War, we review the effectiveness of economic sanctions imposed on the Russian economy, catalogue the effects of volatility spikes in key global commodity markets, and detail the most likely ways in which the conflict will ultimately play out.

Effects of Sanctions

Sanctions against Russia have been relatively effective at economically isolating the country and imposing high macroeconomic costs. Some of these costs (e.g., severe recession, high inflation) will naturally rebalance in the short term. Longer-term macroeconomic costs, such as the erosion of the technological foundation of Russia’s industry and the amplification of the country’s brain drain, will probably persist regardless of the how the war ends.

That said, the Western sanctions network is far from comprehensive. Several Russian banks (e.g., Gazprombank) were not delisted from the SWIFT messaging network, and Russia’s current account balance is reaching record levels, driven by import compression and high commodity prices. Having announced that it will not publish any weekly updates to their foreign exchange (FX) reserves at least until June, the Russian Central Bank is allegedly working to surreptitiously rebuild FX reserves using a chain of banks to conceal ownership and the links between all correspondent banks.

The natural next step is to sanction the actual energy trade. In this regard, we do not believe the EU will manage to implement an oil and gas purchase embargo unless the conflict escalates further. Moreover, the actual damage from such an energy embargo would be digestible by Russia given the higher oil price, weaker currency, and the boost to demand from non-Western economies.

In fact, several countries are only passively cooperating with sanctions, which creates substantial pathways for Russian business as usual, albeit with much higher transaction costs. China and the BRICS (ex-Russia) haven’t imposed any sanctions of their own, and few emerging market (EM) countries have pulled back from relations with Russia, which sees sanctions evasion as proof of political cooperation. Above all, sanctions will not determine the outcome of the war, but simply the extent of macroeconomic damage to the global economy.

Effects of Elevated Volatility

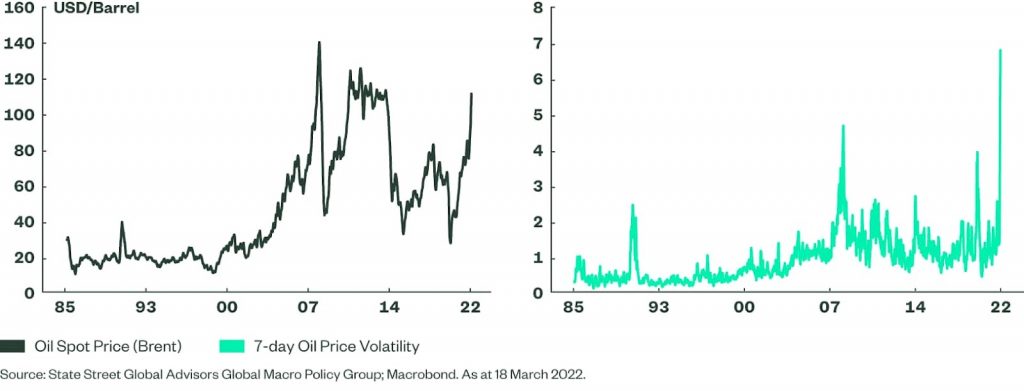

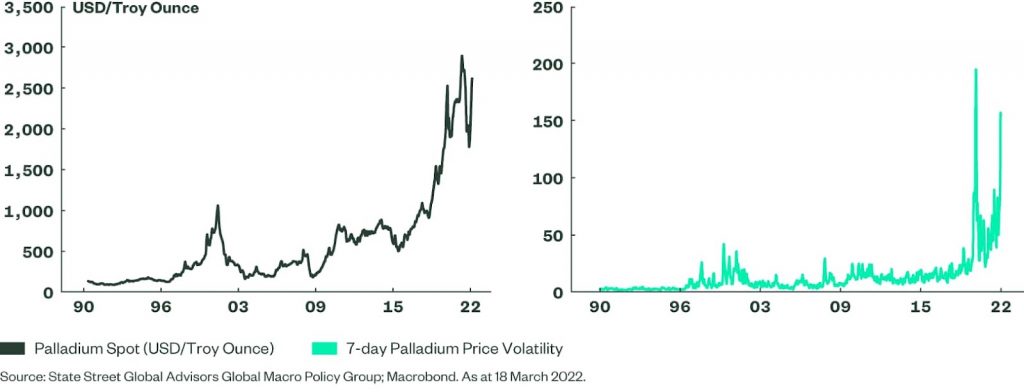

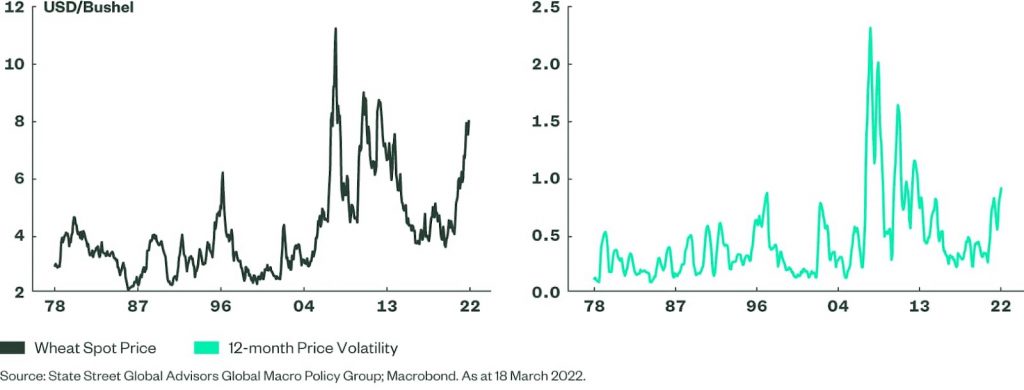

Uncertainty from the war and the effect of sanctions has kept commodity price volatility very elevated. Figure 1 shows the all-time highs in the volatility of select commodities, which logically correlate with high FX volatility as well. This environment could persist for some time given the uncertainty of war.

Figure 1: Historical Prices and Volatility for Oil (Brent), Palladium, and Wheat

Oil (Brent)

Palladium

Wheat

EM countries’ resistance to sanctions has also served to delay the OPEC+ oil production response. A phlegmatic response by Saudi Arabia and the UAE to boost output is becoming a factor in prolonging oil price volatility.

Commodity trading houses may themselves become victims of volatility. The recent trading disaster in nickel markets implies that other balance sheets could be caught out by price spikes as well. There is no lender of last resort for these types of institutions, and institutional failure could have other systemic knock-on effects.

Elevated oil prices typically accompany USD depreciation, especially in the context of the Fed rate-hiking cycle. Also, the war’s supply-side shock will prevent inflation normalization absent aggressive monetary tightening. Yield curve inversion is likely this year as well, as any de-escalation (on the ground, in commodity markets, and in supply chains) will likely not be timely enough to prevent it. Given that this was definitely a negative shock (albeit with uncertain magnitude), it is surprising that global equity markets have approached pre-war conditions again.

Lastly, 2022 may become the “Year of Coal” by virtue of its being the only fuel type with substantial swing capacity and substitutability for natural gas. Increased coal production could help lower broader energy prices and may save Europe next winter if EU sanctions make Russian gas supplies unavailable. Such a substitution would be heavily dependent on increased Chinese coal production (which is currently near an all-time high) and would likely trigger some EU-China tension on carbon emissions in the post-Ukraine war era.

Likely War Scenarios

Russia’s actions in recent weeks do not foreshadow a cessation of hostilities. Recent developments, however, can be seen as signaling either an early cease-fire or a prolonged war (see Figure 2). Taking all information into account, we still believe that some form of partition of Ukrainian territory will likely provide the basis for a cease-fire during the spring.

Figure 2: Signals of Early Cease-Fire versus Signals of Protracted War

The Russians have hinted that sanctions relief must be part of any cease-fire discussion. If a cease-fire is agreed to, we think it is most likely that President Putin would use it as an opportunity to follow one of more of these non-exclusive paths:

- Demand additional concessions from President Zelensky

- Consolidate the captured territories into Russian/quasi-Russian republics and declare victory

- Consolidate the captured territories militarily and undertake a renewed round of fighting in new areas using a stronger strategic base for resupply

Escalation risks for the current conflict remain very high, and potential triggers could include: use of chemical weapons in Ukraine, direct attack on NATO supply lines in Western Ukraine, or “accidental” bombing of NATO territory, especially Poland. Any of these would, at a minimum, extend the conflict and ratchet up Western sanctions, disrupt Russian gas supplies to Europe, and force an emergency EU fiscal- and energy-policy shift. Markets are currently not priced for such an outcome and we therefore recommend that investors not take a directional bet on the war’s endgame in any asset class.

This post first appeared on March 30th 2022 on the State Street Global Advisors Blog.

PHOTO CREDIT: ]https://www.shutterstock.com/g/rospoint

Via SHUTTERSTOCK

DISCLOSURE

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit nor guarantee against a loss.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.