By Mark Barnes, head of investment research (Americas) and Christine Haggerty, global investment research

Equity markets were broadly higher in August, propelled by a late-month resurgence in risk appetite. But this impressive finish belies the powerful risk-off tensions on display for much of the month.

Those tensions rose with mounting worries about the rampant Delta variant, stubbornly high inflation (particularly in the US) and related uncertainties about the Fed’s policy response. Market anxieties culminated in a sharp ‒ yet short-lived ‒ downdraft across global markets mid-month.

But sentiment turned bullish in the final weeks, as a growing chorus of Fed officials signaled a more vigilant stance on the recent surge in inflation, which it views as transitory, while remaining committed to its low-rate policies and focus on job growth.

The US 10-year Treasury yield ticked lower as inflation concerns eased, relinquishing most of its earlier gains.

Bipolar Dynamics

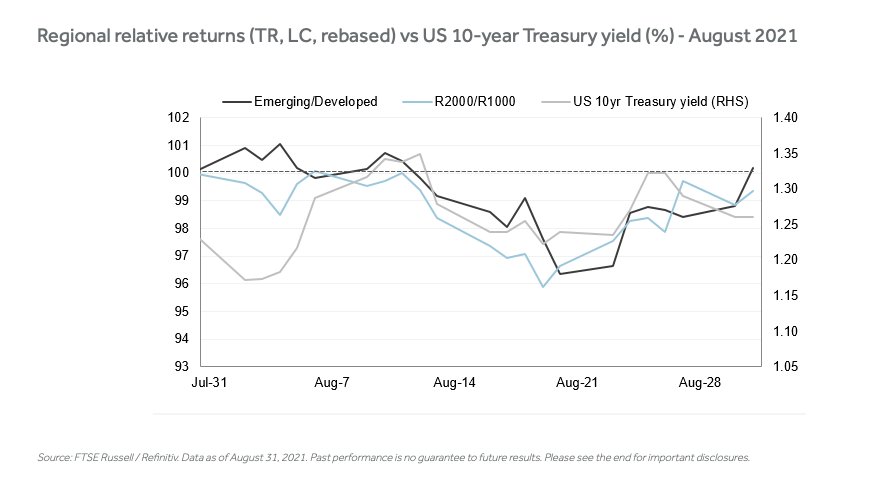

This bipolar behavior is best illustrated in the stunning late-month rebounds in emerging-market and small-cap stocks to the top of the performance rankings from the bottom of the list only weeks earlier.

The FTSE Emerging index rose 2.8% for all of August, and along with Japan and the US, outperformed the FTSE Developed index gain of 2.6%. At its trough in mid-August, the EM index had been trailing by more than four percentage points.

Small-caps enjoyed a similar renaissance. Though the Russell 2000 still lagged the Russell 1000 by 70 basis points in August (up 2.2% vs 2.9%, respectively), its late-month sprint significantly narrowed that gap, which had been as wide as 3.4 percentage points just 10 days earlier.

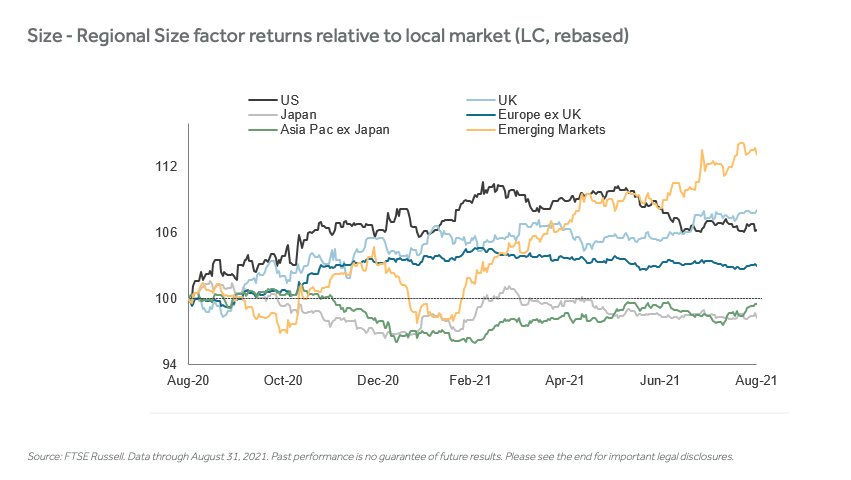

The small-cap comeback was more pronounced elsewhere, as shown below. Based on our global factor data, Size (smaller-cap) built on its strong YTD and 12-month outperformance in Asia Pacific ex Japan, EM and the UK in August, while upholding its lead in the US and Europe.

This post first appeared on September 9 on the FTSE Russell blog.

Photo Credit: Laura Wolf via Flickr Creative Commons

DISCLOSURE

The FTSE Emerging Index provides investors with a comprehensive means of measuring the performance of the most liquid large- and mid-cap companies in the emerging markets. The FTSE Developed Index is a market-capitalization weighted index representing the performance of large and mid cap companies in Developed markets. The Russell 2000 Index is a small-cap stock market index of the smallest 2,000 stocks in the Russell 3000 Index. The Russell 1000 Index is a stock market index that tracks the highest-ranking 1,000 stocks in the Russell 3000 Index. Investors can’t invest directly in indexes.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.