By Steve Sosnick, Chief Strategist at Interactive Brokers

This week, the highly anticipated Consumer Price Index (CPI) for August was released. Traders and investors are keenly focused on any inflation statistics because the Federal Reserve has told us that the return of sustained 2% inflation, alongside a return to full employment, is a key factor in its decision whether to maintain monetary stimulus.

Even though CPI is not the Fed’s preferred inflation measure – they prefer the Personal Consumption Expenditures price index (PCE) – CPI is the most widely followed measure by the public.

It is built into many employment contracts and Social Security payments. We can argue whether it is the best measure of inflation, but it is what comes to mind for most of the public [1].

The Fed

US Federal Reserve Chairman Jerome Powell has been asserting that many of the worst inflationary pressures are transitory, meaning that they are prone to reverse if circumstances change.

Once he put the concept of “transitory” into the financial zeitgeist, investors have been poring through inflation statistics in the hope of getting clarity about whether price increases are likely to ebb, reverse, or persist.

We wrote extensively about this topic two months ago, and here we are doing it again.

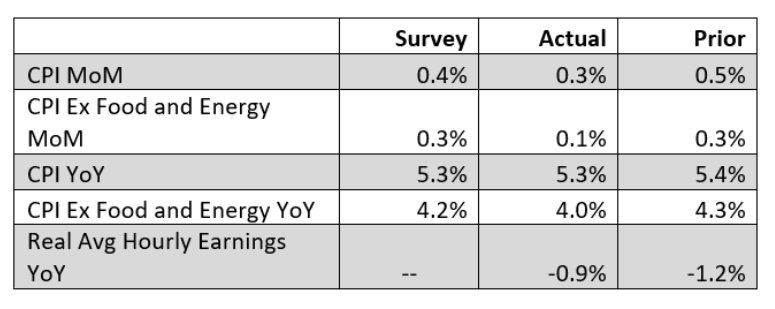

Here are today’s numbers:

Encouraging Signs

We see that all the relevant numbers declined from last month, and most came in below expectations. Although this is just a single data point, the signs are encouraging to those who are concerned about inflation.

Why then do we see a lackluster response from equity markets today? If we were seeing truly transitory inflation, that would bode well for a market that appears fully dependent upon continued monetary accommodation. The problems are these:

- It is indeed a single data point

- Some of the causes for the monthly decline were in sectors like travel and tourism that could be taking a hit because of Covid fears

- The numbers are still relatively high. Remember, the Fed wants to see persistent 2% inflation, not 5%

- Markets have been generally lackluster, and we have seen a new pattern where early rises in stock prices are a trigger for profit-taking rather than the base for an afternoon rally

- The 6 basis-point rally in 10-year treasury prices may be signaling economic woes rather than strictly enthusiasm about lower inflation

So, we can score this round for the transitory team. But today represents merely one inning in a very long game.

This post first appeared on September 14 on the Traders’ Insight blog.

Photo Credit: Kurtis Garbutt via Flickr Creative Commons

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers LLC, its affiliates, or its employees.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.