By Philip Lawlor, managing director, Global Markets Research

As attention starts to shift towards when and how the lockdown exit will be implemented, there are a litany of important questions and themes that need to be considered in a post-lockdown world. In this blog, we pose ten questions, which are top of mind for market participants.

1. From a macroeconomic perspective, the most fundamental question is what will be the long-term economic impact from Covid-19 on growth?

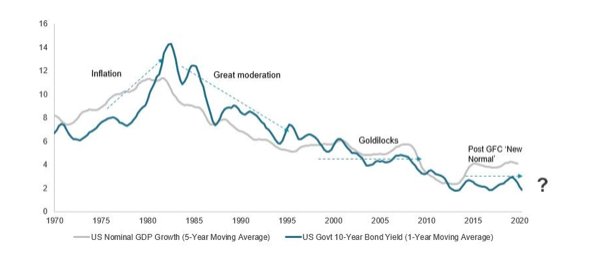

Looking at the long-term historical trend, the moving average of US nominal GDP and bond yields over a fifty-period shows that the US, like many other economies, have encountered four major economic regimes: In the 1970s, the US economy experienced a period of significant inflation; then followed a period of so-called Great Moderation under Paul Volcker, which stripped inflation out of the system; then encountered 10-year of Goldilocks under Alan Greenspan, with nominal GDP averaging about 6% p.a.; and finally, a new normal, post global financial crisis, which have seen nominal GDP averaging about 4% p.a.

The close relationship between bond yields and nominal GDP and the continued decline in bond yields suggest that the US economy could be ratcheting towards a fifth lower trend growth regime.

US Nominal GDP Growth vs US 10-Year Govt Bond Yield

Source: FTSE Russell / Refinitiv. Data as of April 2020. Past performance is no guarantee to future results. Please see the end for important disclosures.

income data lags equity markets, the Fed is well aware that, if equity weakness persists, it could create a vicious spiral.

2. In a lower for longer economic growth environment, what does this imply for Climate and Carbon Emissions Targets financing. Could lower growth result in lower carbon output levels?

Lower trend growth could do a lot of the heavy lifting by way of carbon emissions reduction. However, one of the main consequences for moving towards a lower growth trend trajectory is that it exacerbates debt financing and solvency issues.

3. Will there be many more years of financial repression?

As learnt post the global financial crisis, negative real interest rates combined with central bank balance-sheet expansion had crowded out savings, which has been a persistent theme since then and could have a long duration.

4. Will central banks further extend asset purchases to equities and turn Japanese?

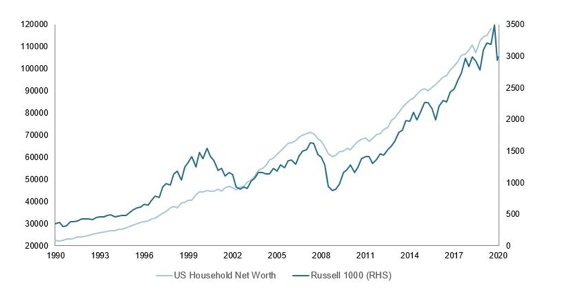

There is a strong relationship between US households’ net worth and equity performance. With US consumption representing 70% of GDP growth, the Federal Reserve is acutely aware that US households’ net worth is very important to its economy. While household

Source: FTSE Russell / Refinitiv. Data as of April, 2020. Past performance is no guarantee of future results. Please see the end for important legal disclosures.

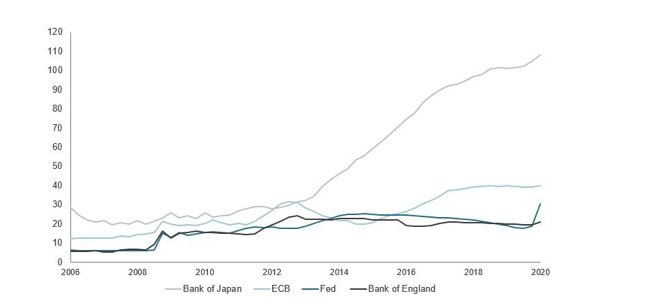

5. What firepower do central banks still have to deploy?

Central banks have already undertaken massive liquidity injections in response to the Covid-19 shock and both the Fed and ECB have extended their QE asset purchases from government bonds, to include mortgage-backed securities, municipals, investment grade, and more recently, high-yield (fallen angels) credits.

Using the Bank of Japan as a proxy, the Bank of Japan has been by far the most aggressive to date, with the size of its balance sheet rising to 110% of its economy (see chart below). Even allowing for recent expansion, the Fed, ECB and BOE still have comparatively significant room in their balance sheets to expand QE programs substantially.

Central Bank Balance Sheets as a Percentage of GDP

Source: FTSE Russell / Refinitiv. Data as of April, 2020. Past performance is no guarantee of future results. Please see the end for important legal disclosures.

6. Therefore, this poses second order questions, such as will central banks end up monetizing debt (helicopter money)?

Given that fiscal deficits are likely to easily surpass levels seen in 2009, post GFC, this infers that central banks might need to embark on some debt monetization process, where debt is transferred to the balance sheets of central banks.

7. How worried should we be about inflation as supply shortages kick in?

The recent upturn in Chinese CPI forecast has shown that supply-chain disruptions could induce some price increases. However, referencing 2010 and 2011 when this last occurred, the period resulted in negative real earnings growth, which ended up being disinflationary. Therefore, central banks will be most concerned about declining household income and deflationary risks.

8 & 9 Will there be an intensification of localisation (versus globalisation) to build more resilience into supply-chain mechanisms? Will business strategies adopt Just in case’ not ‘Just in time’ inventory model?

Manufacturing processes have been finely tuned to minimize the working capital tied up in inventories. Will this business model still be suitable given the disruption risks to supply chains?

10. The recalibration to working from home is going to highlight the need for major business adjustments (i.e., real estate, airlines, transportation).

The biggest themes in coming months will be identifying winners and losers?

This article, first published on May 4, appeared on the FTSE Russell blog.

Photo Credit: Yuri Samoilov via Flickr Creative Commons

© 2020 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) MTSNext Limited (“MTSNext”), (5) Mergent, Inc. (“Mergent”), (6) FTSE Fixed Income LLC (“FTSE FI”), (7) The Yield Book Inc (“YB”) and (8) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “MTS®”, “FTSE4Good®”, “ICB®”, “Mergent®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, FTSE Canada, Mergent, FTSE FI, YB or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a licence from FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and/or their respective licensors.

{kind=link}