The market continued to perform well for the first quarter with the S&P index up 10% and the Alerian MLP Index (AMZ) up a very robust 18.0%. Given the large move upwards in the Alerian MLP Index, the coming announcements for first quarter distributions need to meet or exceed the market’s collective estimate to continue to support the higher prices of MLPs.

Even with the strong general uptrend, the market still does occasionally react incorrectly to information, in my opinion, especially if the entity contains something unique. Case in point, QR Energy, LP (QRE).

On March 6th before the market opened, QR Energy announced its fourth quarter 2012 results and 2013 outlook and hosted its conference call during that morning. QRE is rather unique since it is the only MLP to have a “management incentive fee” structure, which is somewhat similar in a big picture sense to the more traditional Incentive Distribution Right structure but I believe is different enough that the market reacted with confusion on March 6th.

QRE’s management incentive fee structure provides for a 0.25% quarterly fee to be paid to the General Partner based upon QRE’s total proved oil and gas reserve value and the fair market value of any of its other assets. Subject to certain conditions, the General Partner also has the right to convert up to 80% of its management incentive fee payment stream into Class B common units.

The Conversion Election by the General Partner then adjusts the future calculations for the management incentive fee such that QRE does not pay additional management incentive fees on the effective value that was converted into Class B units. There is a more detailed explanation of this structural aspect of QRE in its IPO Prospectus on pages 100 through 105 that also includes a walkthrough of hypothetical calculations for a Conversion Election.

For the fourth quarter of 2012, QRE’s General Partner made its first Conversion Election, as evidenced by this footnote from the press release:

“(2) The GP elected to convert 80% of its 4Q12 management incentive fee into 6.1 million units, which are entitled to the 4Q12 distribution. The conversion was offset by a reduced cash management incentive fee in 4Q12.”

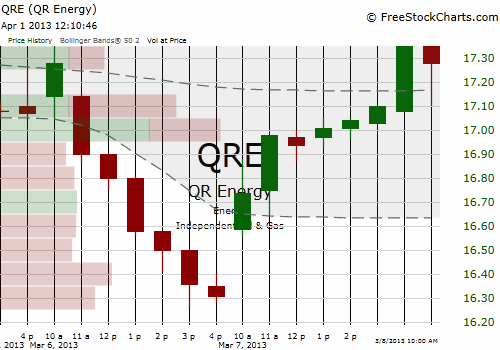

The footnote seems to have caused some confusion in QRE unitholders and when people are confused they tend to hit the sell button, as shown in the chart below:

The investments discussed are held in client accounts as of March 31, 2013. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.