By Steve Sosnick, Chief Strategist at Interactive Brokers

During early August, I bestowed an unofficial gold medal on Mr. Market for his remarkable ability to climb a wall of worry. Throughout the past year and a half, markets rose despite myriad worries about the economy, the virus, and other concerns large and small.

This week, however, we have seen a slip during that climb. The questions on many investors’ minds are “why today” and “how far”?

In the piece referenced above, posted on August 3rd, we wrote:

The key conundrum that I’ve been wrestling with is why VIX is consistently lower now than it was earlier this year. We have far less consensus about the paths of monetary and fiscal stimuli, yet the relatively elevated 19 VIX is below the low end of the 20-22 trading range that persisted throughout much of the year.

Fed Policy

It is quite possible the recent move and the relatively slight but steady declines that we have seen throughout this month are the result of investors’ recognition that this week’s Federal Reserve meeting could signal an end to the extraordinary monetary accommodation that we have seen since the Covid crisis just as the questions about the federal debt ceiling and proposed infrastructure spending come to the fore.

There is broad based selling in commodities, which may reflect investor fears about the pace of monetary policy and the anticipated economic rebound. Remember also that we wrote about the changing patterns of afternoon trading in the US markets over a week ago, noting that it was quite possible that US markets were seeing less support from large institutional buyers. Sometimes the cracks are building, just hard to spot.

China Worries

The proximate cause of Monday’s fall is the potential default of China Evergrande Group (3333.HK), a heavily indebted real estate developer who has a payment due this week. Yet this is not a new problem.

China Evergrande has been under pressure for months, as the chart below shows. Furthermore, we have asserted for months that China has been pursuing policies that appear to take little consideration of investor concerns, particularly when those investors are foreign. If markets efficiently discount future events, how did this suddenly become a problem today?

Source: Bloomberg

Market dislocations occur when investors become more concerned about return OF capital than return ONcapital. Bond holders in Evergrande and a wide range of Chinese property developers suddenly developed that concern this week. When those concerns become widespread, investors tend to seek safe havens like government bonds.

Although we see 10-year Treasury yields falling by 4 basis points to 1.32%, that is hardly a major flight to safety. Gold, another traditional haven, is up about $11 – nice, but not significant. (Bitcoin, which some have touted as a safe asset, has recovered slightly from a 10% loss, belying that status.) Meanwhile, US high yield bonds are lower, but hardly enough to dent their recent stellar returns. The chart of the iShares iBoxx High Yield Corporate Bond ETF (HYG) demonstrates that:

Technical Indicators

If this week’s tumble truly was about investor fears, we would likely see more aggressive selling in risky corporate bonds of all stripes, rather than seeing those fears constrained mostly to the country and the specific sector that is most highly affected.

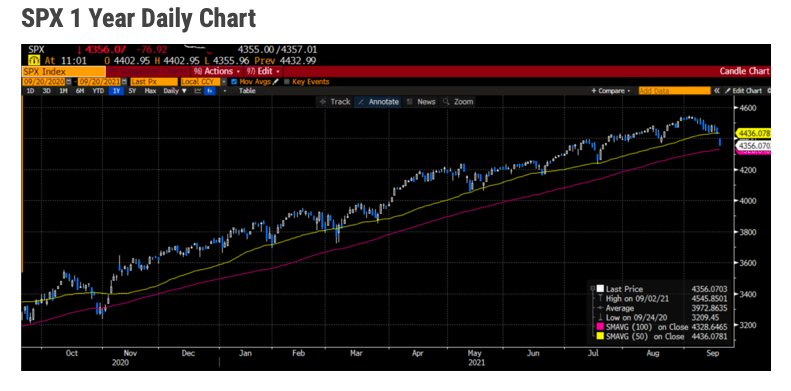

We see that the S&P 500 Index (SPX) broke through the 50-day moving average that has supported its rise throughout the past year. It would not be at all surprising if traders and investors alike were using that as a level for stop loss orders. The next logical support would be provided by the 100 day moving average, which is currently at 4328:

Source: Bloomberg

Also worth noting is that both the 50 and 100 day moving averages are pointing upwards. That indicates that we remain in an uptrend until proven otherwise.

Monday’s slump, while the largest intraday drop in two months if we close at or below current levels, is still not sufficient to bring us to even a 5% correction from the record high set early this month or the point where we are breaking our longer-term uptrends.

Takeaway

This week may or may not be the start of something larger. We can’t and won’t know that for some time. As of now, the first round of reflexive dip buyers are licking their wounds, many learning for the first time that not every minor dip is an immediate buying opportunity.

But until or unless we see a pattern of continuing declines and weakening sentiment, we have to take a look at the next support level and gather more evidence about whether it is the start of a larger fall or simply a minor slip as markets climb that wall of worry.

This post first appeared on September 20 on the Traders’ Insight blog.

Photo Credit: XXX via Flickr Creative Commons

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers LLC, its affiliates, or its employees.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

DISCLOSURE: ORDER TYPES / TWS

The order types available through Interactive Brokers LLC’s Trader Workstation are designed to help you limit your loss and/or lock in a profit. Market conditions and other factors may affect execution. In general, orders guarantee a fill or guarantee a price, but not both. In extreme market conditions, an order may either be executed at a different price than anticipated or may not be filled in the marketplace.

DISCLOSURE: FOREX

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

DISCLOSURE: DIGITAL ASSETS

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

DISCLOSURE: FUTURES TRADING

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

{kind=link}