By Emerald Yau, Head of Equity Index Product Management, Asia

Which less-explored market has been delivering stellar equity performances in recent years, performances on par with or better than those of global equities, developed market equities, emerging market equities, and frontier market equities?

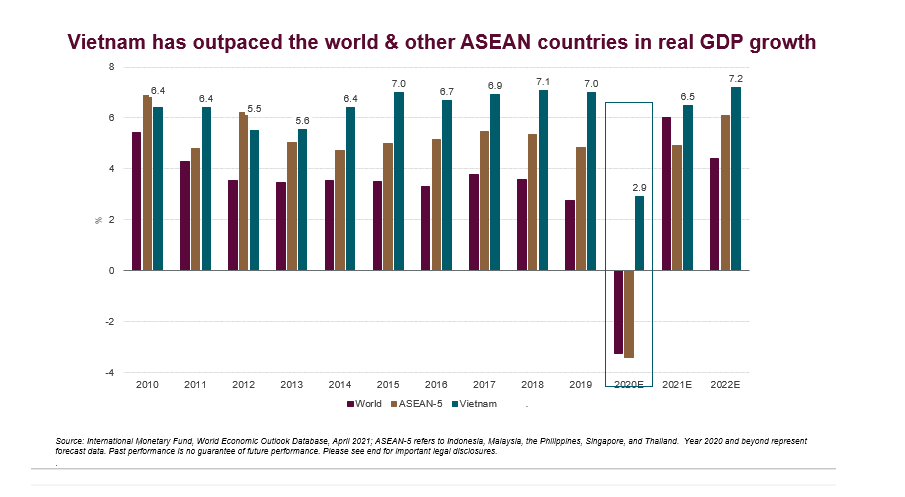

What market represents one of the few countries in the world to have posted positive growth in 2020 amidst the COVID-19 pandemic? It’s a country market that is also a well-positioned manufacturing hub ready to benefit from supply chain relocations due to US-China trade tensions, and boasting cheaper labor costs. It enjoys substantial road, airport and seaport transportation infrastructure, all of which is being rapidly upgraded to cater for increasing export demand. And it’s a market that is also currently on FTSE Russell’s watchlist as under consideration for advancement from frontier to secondary emerging market status.

The country we’re talking about is Vietnam.

Pandemic Proof

Vietnam’s economic development and industrialization over recent decades have been remarkable. Economic and political reforms have propelled the country forward, transforming what was once one of the world’s poorest nations into what is today a solidly lower middle-income one.

In recent years, multinationals looking to diversify their manufacturing bases and relocate their supply chains have been attracted to Vietnam because of its cheaper labor costs and improving infrastructure. Companies such as Samsung and Apple supplier Foxconn have both recently announced plans to expand production in Vietnam.

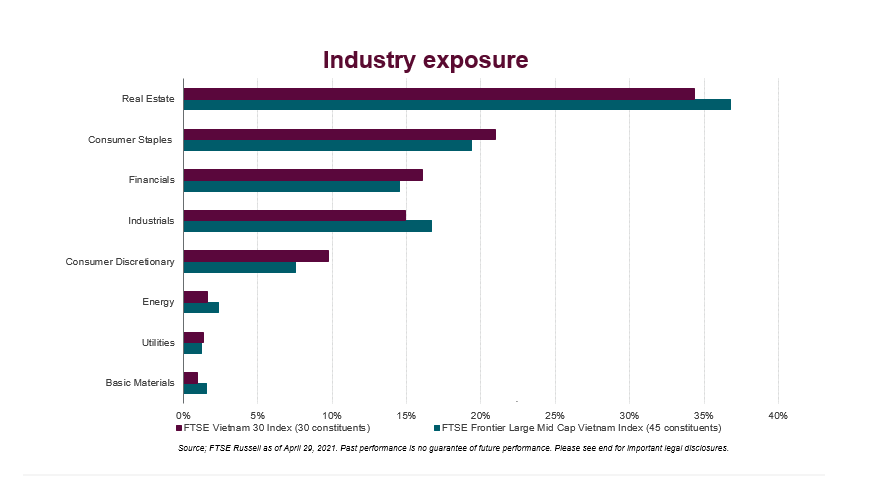

This increasing foreign direct investment also brings new wealth to the local population. According to World Bank estimates, 26% of Vietnam’s population is expected to make up the country’s emerging middle class by 2026, up from the current 13%. Both these factors could lift consumption and real estate demand, the two areas with the most exposure in FTSE Russell’s Vietnam indices.

Strong Performance

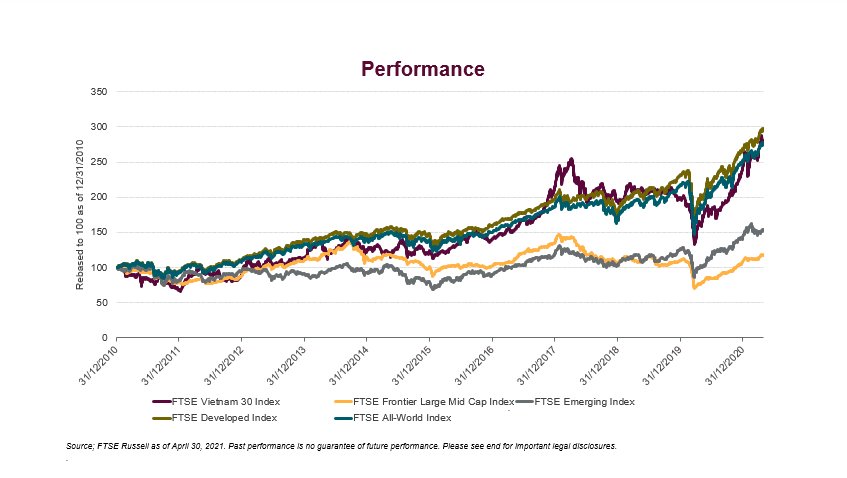

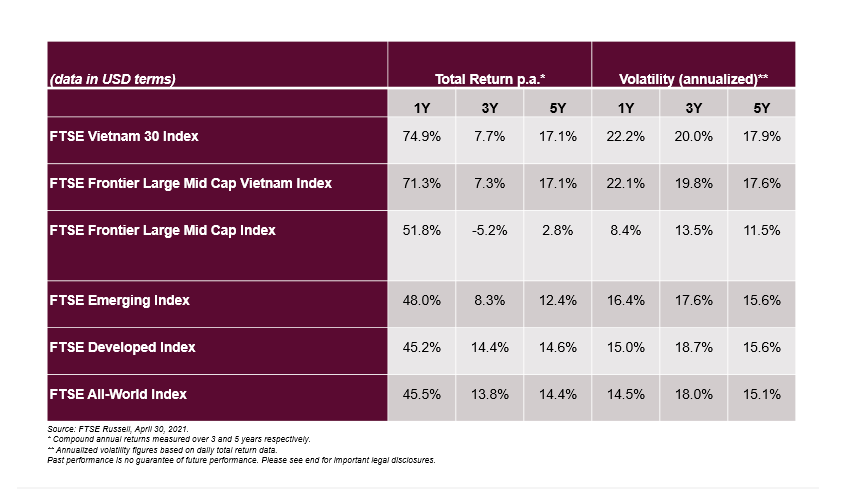

Some investors may be surprised to learn that the Vietnam market has in fact delivered better or similar in terms of per risk return by comparison with overall frontier equities, emerging market equities, development market equities, and global equities over the longer term[1]. Vietnam equities have performed strongly, delivering a 5-year cumulative return in US dollar terms of over 120%. During the same period, global stocks only delivered a 96% total return on a cumulative basis.[2]

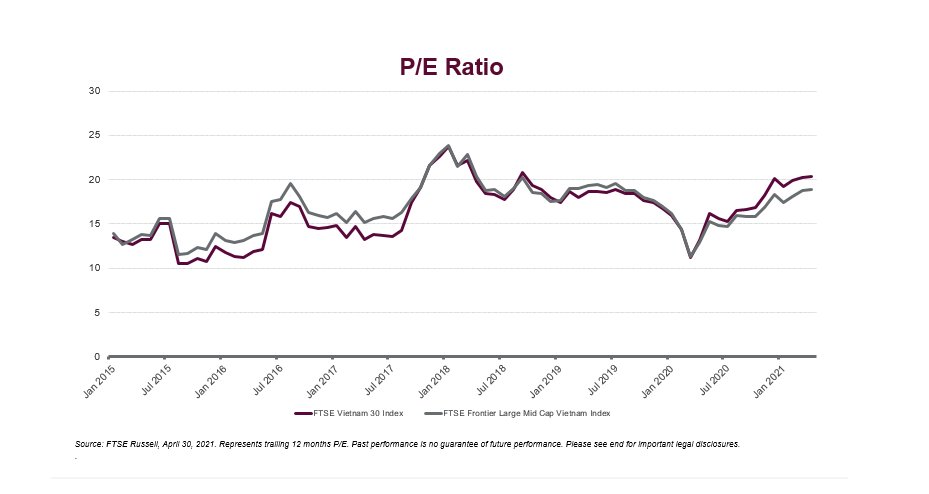

It is true that Vietnam stock valuations have been edging higher. However, they remain reasonable compared to those of many neighboring emerging Asian countries – for example, those of Thailand (over 40x) and Malaysia (over 25x)[3].

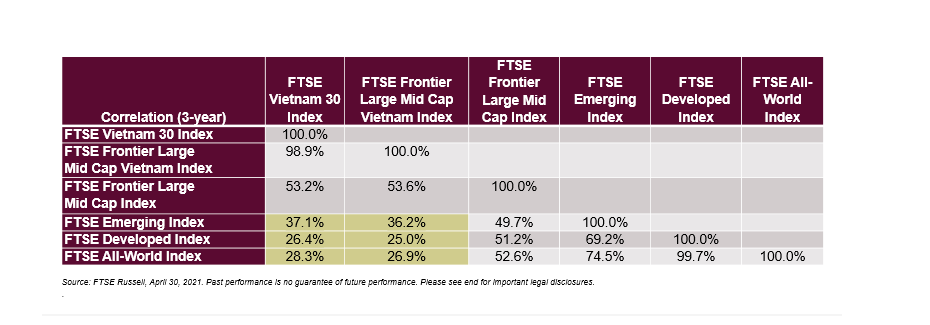

While volatility is also higher in the Vietnam market – not unexpected given the market’s frontier nature – the low correlation of Vietnam equities with emerging, developed, and global equities could provide diversification benefits to investors already holding a global portfolio.

Investment Ecosystem

In 2020, FTSE Russell entered into partnership with Singapore Exchange to develop a comprehensive Asian and Emerging Markets focused, multi-asset index derivatives offering. Since then, the Singapore Exchange has launched multiple index futures based on FTSE Russell indices, including two Vietnam equity index futures. These index futures have made it easier for investors to manage the risk associated with Vietnam equities.

The two index futures, together with a newly launched ETF benchmarking the FTSE Vietnam 30 Index, have created an ecosystem that now gives international investors an efficient way of accessing or hedging this market.

In addition, Vietnam is currently on FTSE Russell’s watchlist for reclassification from frontier to secondary emerging market status. Before this happens, though, the country will need to implement a true delivery versus payment (DvP) settlement mechanism and address issues such as foreign ownership limits. See our March 2021 Country Classification Review for more details.

Long-Term Play

When looking to capitalize on the macro trends driving Vietnam’s future, investors should be aware of certain risks, particularly as Vietnam is still a frontier market for now.

Firstly, Vietnam regulates the foreign ownership limits for Vietnam-based companies. While this is taken into account in FTSE Russell’s Vietnam indexes, the limitations could constrain the growth capacity of the Vietnam market, and restrict international investors’ access to the most popular companies once the ownership limits on such companies are reached.

Secondly, domestic investors have been piling into Vietnam stocks as deposit rates edge lower. Foreign investors are also increasingly tapping Vietnam opportunities. The recent surge in trading volumes on the Ho Chi Minh Stock Exchange has caused order overload issues for Vietnam’s main bourse.

The exchange has been working towards a system upgrade resolution which is expected to be ready later this year. Despite concerns associated with this overload, risk-tolerant foreign investors have not stopped engaging in a long-term investment strategy that gives them exposure to this rapidly growing economy.

Vietnam offers a compelling growth story. With an export-oriented economy that is likely to benefit directly from global recovery from the pandemic, the Vietnam market seems poised to continue its rise from the frontier horizon in the years ahead.

This post first appeared on May 31 on the FTSE Russell blog.

Photo Credit: guido da rozze via Flickr Creative Commons

FOOTNOTES

[1] Based on 5-year daily total return data in US dollar terms.

[2] Refers to FTSE Frontier Large Mid Cap Vietnam Index and FTSE All-World Index, respectively; return data as of April 30, 2021.

[3] CEIC data; as of May 2021.

DISCLOSURE

© 2021 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) MTSNext Limited (“MTSNext”), (5) Mergent, Inc. (“Mergent”), (6) FTSE Fixed Income LLC (“FTSE FI”), (7) The Yield Book Inc (“YB”) and (8) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “MTS®”, “FTSE4Good®”, “ICB®”, “Mergent®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, FTSE Canada, Mergent, FTSE FI, YB or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

The FTSE Vietnam 30 Index comprises the largest 30 Vietnam companies by full market capitalisation that are constituents of the FTSE Frontier Vietnam Index and trade on Ho Chi Minh Stock Exchange.The FTSE Frontier Index Series provides a comprehensive and transparent series of benchmarks for the performance of large, mid and small cap equity securities from eligible Frontier markets in Europe, Americas, Asia-Pacific, Africa and the Middle East. FTSE Frontier Indexes can be segmented by Size, Region, Country and Industry Sectors and are calculated on a price and total return basis. Further information on FTSE Russell Country Classification is available here.

The FTSE All World Index measures the market performance of large- and mid-capitalisation stocks of companies located around the world. Includes approximately 3,900 holdings in nearly 50 countries, including both developed and emerging markets. The FTSE Developed Index is designed for use in the creation of index tracking funds, derivatives and as a performance benchmark. Investors can’t invest directly into indexes.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.