By Matt Wagner, CFA, Associate, Research

Investors who withstood last spring’s volatility have a good problem to solve for.

S&P 500 returns since its March 23, 2020, low have been remarkable—over 90%. But with this head-spinning rebound have come unattractive valuations. Multiples have expanded from 13 times forward 12-month earnings last March to over 23 times forward 12-month earnings today.

With valuations on the S&P 500 the highest they have been since the early 2000s, investors may want to consider “opening up the playbook”—reducing a home country bias toward large-cap U.S. equities in favor of allocations toward more moderately valued international equities.

Headwinds Bring Opportunity

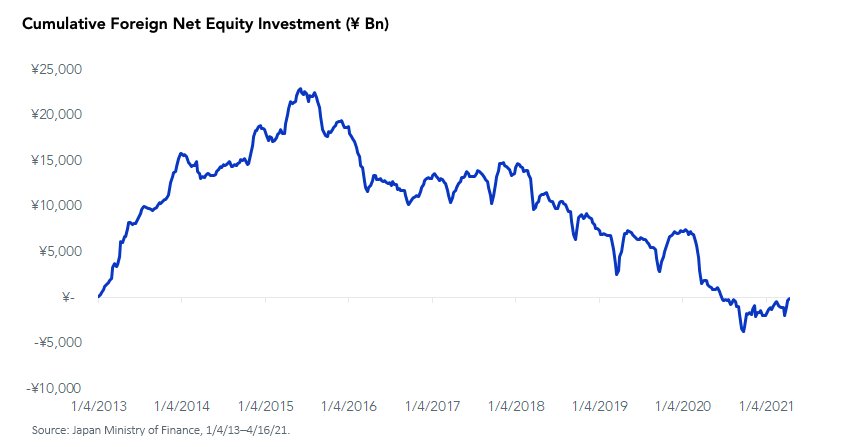

Arguably no market has been more unloved by international investors in recent years than Japan. There are a few theories as to why:

- Sector composition: A lack of domestic tech mega caps in favor of cyclical sectors—like Autos and Banks—has been a headwind for Japanese indexes during a global rally in growth stocks

- Policy mistakes: A government that has made a handful of policy missteps, particularly with consumption tax hikes in 2014 and 2019

- Aging population: Demography is destiny, or so it is said. There has been fear that an aging population in Japan will put a lid on the country’s long-term growth potential, coupled with chronically low equity investment from a notoriously conservative domestic investor base

Most recently, a surge in coronavirus cases has added to near-term economic uncertainty. Several of Japan’s largest cities recently enacted a lockdown for the next several weeks—coinciding with the Golden Week holidays—to curb the virus. Unsurprisingly, the lockdowns have dented Japanese equity returns over the past week.

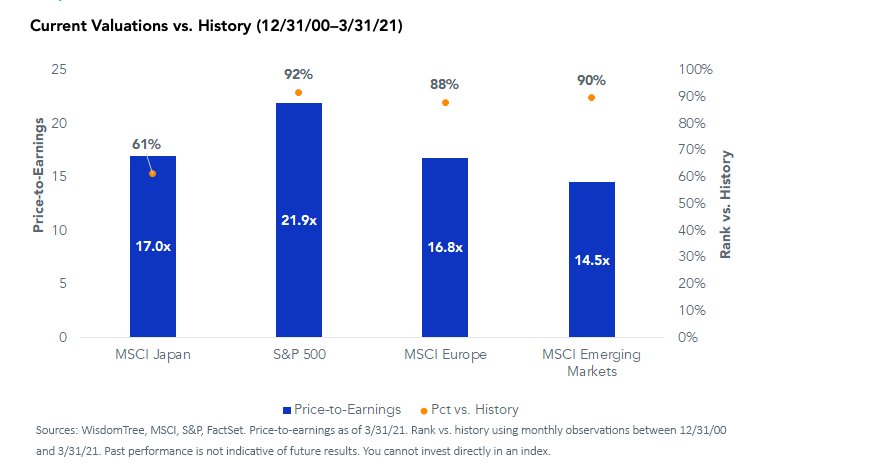

In part as a byproduct of low international investor interest, Japanese equities are significantly discounted relative to the U.S., and have a much lower valuation relative to its own history than most other major markets.

These valuations are what attracted Warren Buffett to initiate a 5% stake in five Japanese trading houses in August of last year.

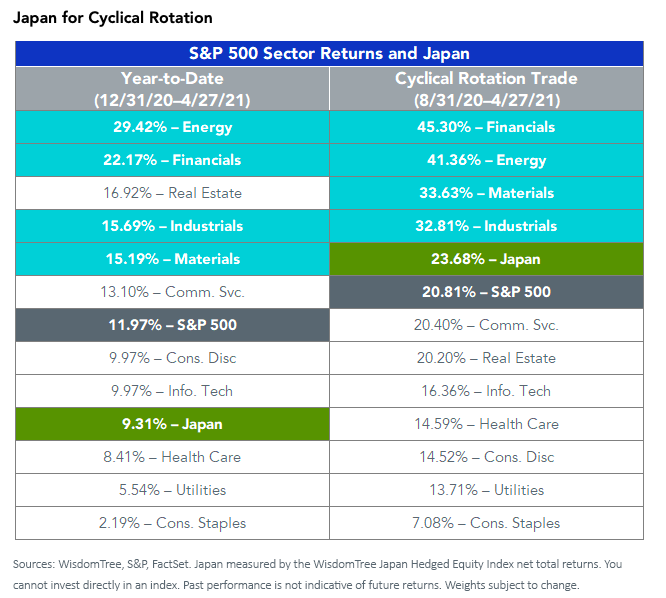

While Japan’s position as a market more tilted to cyclical sectors was a headwind during a global rally in growth stocks, it may be perfectly primed for an environment in which economic growth is expected to make a significant recovery in the coming years.

For example, WisdomTree’s Japan Hedged Equity Index—which tilts more toward cyclical sectors than the broad MSCI Japan Index and neutralizes yen fluctuations—has outperformed the S&P 500 by nearly 300 basis points since the end of August. The recently enacted lockdowns have been a headwind to year-to-date returns.

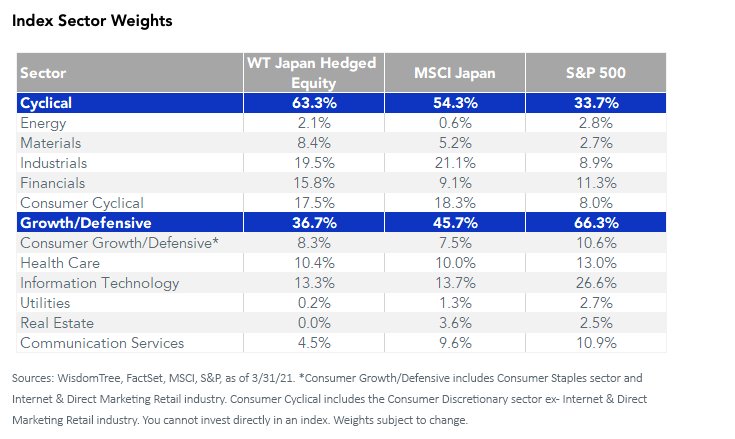

The S&P 500 only has about a 34% weight in the cyclical sectors most likely to benefit from an accelerating economy. The WisdomTree Japan Hedged Equity Index has almost twice as much weight and nearly 10% more than the MSCI Japan Index.

The S&P 500 is up more than 11% to start the year despite concerns over rising interest rates. Nonetheless, the potential for higher rates becoming a headwind to both fixed income and equity returns remains a top concern among asset allocators.

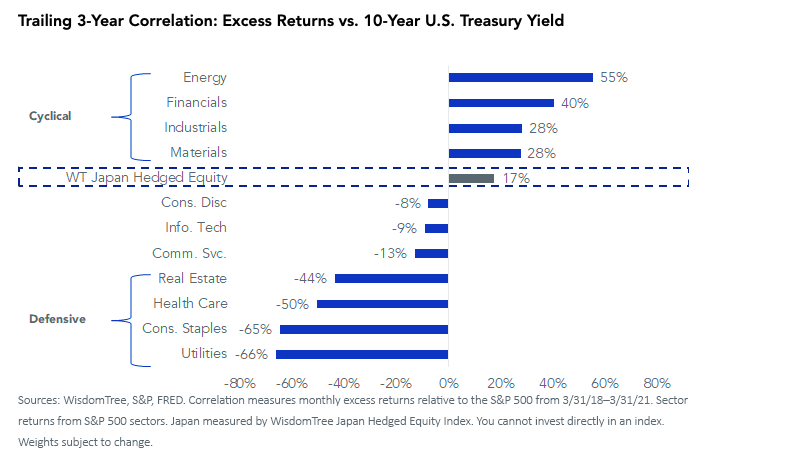

Given the cyclical tilts of the Japanese equity market, as well as the tendency for the yen to weaken alongside a rise in U.S. rates, the WisdomTree Japan Hedged Equity Index has had a positive correlation between its outperformance and rising Treasury yields.

Conclusion: Follow Buffet’s Playbook

The steady and reliable earnings growth from U.S. mega caps powered U.S. indexes higher over the past several years. With U.S. valuations now near two-decade highs and the potential for a synchronized global recovery on the horizon, investors may want to consider Buffett’s “Buy Japan” playbook.

This post first appeared on April 29 on the WisdomTree blog.

Photo Credit: Ray in Manila via Flickr Creative Commons

Disclosure

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. The MSCI Europe Index captures large and mid cap representation across 15 Developed Markets (DM) countries in Europe. The MSCI Emerging Markets Index captures large and mid cap representation across 27 Emerging Markets (EM) countries. The Standard and Poor’s 500, or simply the S&P 500, is a free-float, weighted measurement stock market index of the 500 large companies listed on stock exchanges in the United States. Investors can’t invest directly in indexes.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates. The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)