By Jeremy Schwartz, CFA, Global Head of Research

One of the market implications of the COVID-19 pandemic has been the remarkable performance of large-cap growth and technology names, particularly those impacted by the work-from-home trend and cloud computing, and the underperformance of small-cap stocks that were more or less shut down during the economic lockdowns.

Positive vaccine news boosted hopes for an economic reopening in 2021, which flipped market signals, and small caps and value stocks rallied strongly in November. The Russell 2000 Index, a gauge of U.S. small-cap equity performance, delivered some of the strongest gains in its history.

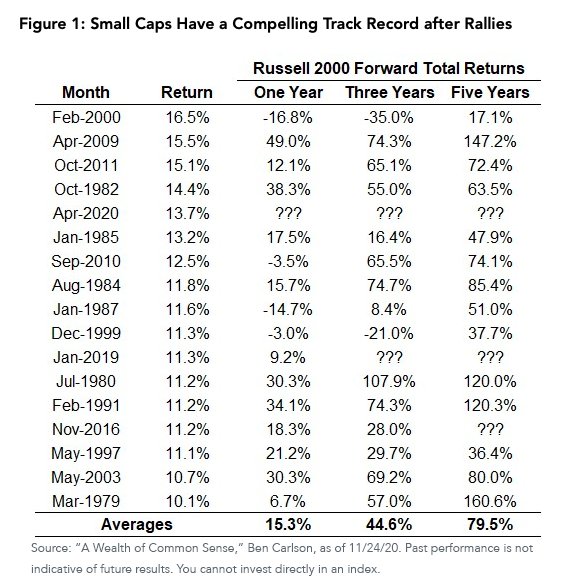

Ben Carlson, author of the blog “A Wealth of Common Sense,” has evaluated what happened in the aftermath of past small-cap surges, like the one we saw in November.

- The forward returns over one-, three- and five-year intervals were, on average, quite compelling, especially for the five years following the small-cap surges that Carlson studied. The average five-year cumulative return was almost 80%. Notably, the minimum return was 17.7%, following the peak of the market in February 2000.

- The shorter time periods had more risk of negative subsequent returns. But even in the three-year analysis, only two periods had negative returns: around the 1999–2000 peak and into 2002–2003 market trough.

- The average one-year return of 15% is quite positive for a forward-looking one-year interval.

While the future is always uncertain, the data makes a strong case that we had an inflection point for small-cap stocks—and that while investors will inevitably feel they ‘missed’ this large turn, this past analysis indicates there’s reason to believe more is to come.

Figure 1: Small Caps Have a Compelling Track Record after Rallies

There is also research that suggests January is a particularly strong time for the performance of small-cap stocks. This “January Effect” does not work every year, and small caps generally have faced a tough stretch for quite an extended period.

But some of the arguments for why small caps perform well in January may be relevant this year. In years with large drawdowns, there can be some sharp tax loss selling. This drives prices down even further and below their fair value, resulting in them snapping back in January to correct for that selling as investors reestablish positions.

WisdomTree rebalances its fundamentally weighted indexes in late December to capitalize on similar trends of selling unrelated to corporate fundamentals creating noise and opportunities to pick up value trades.

Small-cap dividend-payers were particularly impacted during the 2020 pandemic and faced some of the strongest selling pressures all year. We believe small caps are ripe for Christmas shopping lists, particularly to get ahead of the January Effect in small caps.

Photo Credit: XXX via Flickr Creative Commons

DISCLOSURE

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.

![What $315 billion in gold looks like [video]](/content/default.jpg)