By Chelsea Rodstrom, Research Analyst, Global X

For decades, investors have been attracted to China’s impressive growth story. Yet as China’s economy matures, its potential growth opportunities are becoming more narrowly concentrated in specific areas and themes.

Among the most powerful are those areas tied to the rising impact of China’s consumers, who have experienced years of high wage growth, migration into cities, and an expansion of internet connectivity. The government has also made consumption a priority as the economy transitions away from export-led industries.

As a result, China’s middle class, which is larger than the entire population of the United States, is spending time and money on goods and services, spanning travel and leisure, e-commerce, social media, gaming, and health and wellness. In this piece, we look at how the Global X MSCI China Consumer Discretionary ETF (CHIQ) is positioned to seek to capture this trend.

Key Stats

China’s Consumer Discretionary sector is the country’s largest by total market cap, yet it is still just half the size of its US counterpart.

This is despite the fact that China’s population is four times larger than the US’s and is experiencing a rapidly growing middle class, suggesting that the sector is still in its early stages of growth.

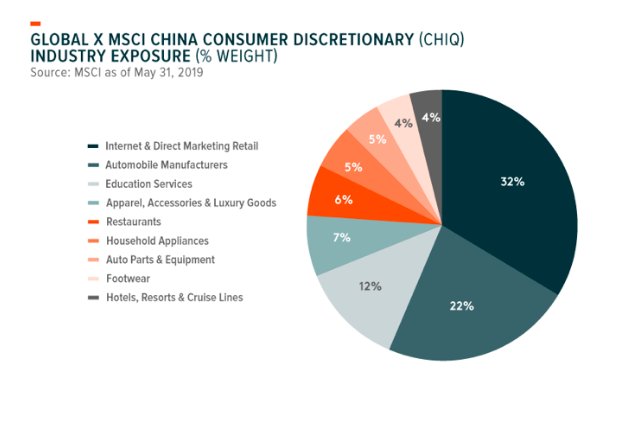

The largest industry group is Internet & Direct Marketing Retail, representing nearly one-third of the sector, followed by Auto Manufacturers, and Education Services. Analysts expect the sector to experience 12% overall sales growth in the next year, compared to just 6% in the US.1

Despite higher growth expectations, the Chinese sector has lower debt burdens and is cheaper across forward price-to-earnings, forward price-to-sales, price-to-book metrics.

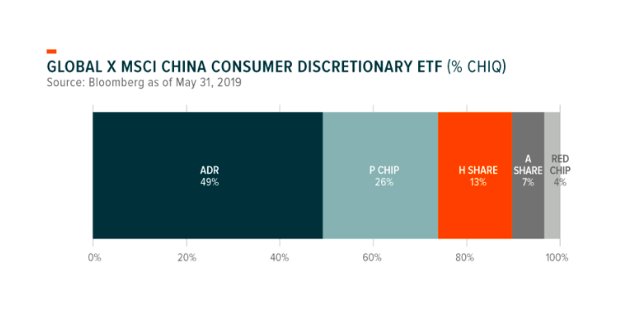

While more than half of the sector is listed in the US via ADRs, the recent inclusion of onshore China-listed A shares into MSCI’s indexes broadens foreign investor access to the Consumer Discretionary sector in China.

American Depositary Receipts (ADRs) are stocks of Chinese companies listed on American stock exchanges. A shares are listed on domestic stock exchanges in China and have been historically difficult to access. P Chips are stocks of companies operating in China, listed in Hong Kong, and incorporated in the Cayman or British Virgin Islands. Red Chips are stocks of companies based in China, incorporated abroad, and listed in Hong Kong. H shares are stocks of companies incorporated in China and listed in Hong Kong.

Background on Consumer Discretionary Sector in China

Consumer Discretionary is one of China’s “new economy” sectors, with only 3% of the sector represented by state-owned enterprises (SOEs). Despite less government ownership, many of the companies in the sector benefitted from recent government policies designed to pivot China from an export-led economy to a consumption-oriented growth model.

Accordingly, the sector’s performance and composition differs greatly from old economy sectors like Energy, Materials, or even Financials sectors, which tend to be more export-oriented and have between 34-40% SOE representation.2

The Consumer Discretionary sector is largely comprised of growth-oriented companies hailing from the e-commerce, automotive, education, and travel & luxury segments.

- E-commerce: As the world’s leading e-commerce market, China accounts for more than 40% of the world’s e-commerce transactions, up from just 1% from a decade ago.3 With rising highspeed internet coverage and broad adoption of mobile payments, e-commerce platforms in China are growing fastest in the country’s smaller Tier 3 and 4 cities, where access to online stores provides greater convenience and wider selection to customers.4

- Automobile Manufacturers: China is the largest automobile market in the world, selling 28 million cars in 2018, which outpaces the US by 11 million vehicles.5 National policy has promoted a shift towards developing new energy vehicles (NEVs), like electric and autonomous vehicles, by providing favorable lending conditions to startups, creating an easier path for licenses to purchase these vehicles, and offering subsidies.

- Education: The growth of China’s middle class has supported China’s booming education industry, which has benefited from families’ commitments to education and government policies aimed at promoting international competitiveness. This industry includes for-profit education programs focused on foreign languages, as well as test prep for admissions exams. Although programs are available to students of all ages, businesses have also begun adopting professional education platforms.

- Travel and Luxury: Although a smaller segment of the Consumer Discretionary sector, tourism in China has been a fast growing industry, owing to the growth of high-income earners, the spending habits of younger consumers, and the proliferation of Chinese hotel chains, airlines, luxury resorts, casinos, and travel agencies.

Long Tailwinds

- Urbanization: Much of China’s population has moved to cities in pursuit of higher wages and greater disposable income. Since 2010, the percentage of the population living in cities has increased by nearly 3% annually and the disposable income of urban households has increased by nearly 10% per annum.6 With greater urbanization and disposable income, China’s rising middle class has become increasingly consumer-oriented and connected online. Internet penetration has reached 55%, rising nearly 20% in a decade, but still has much further room to grow compared to the US, which stands at 87%.7

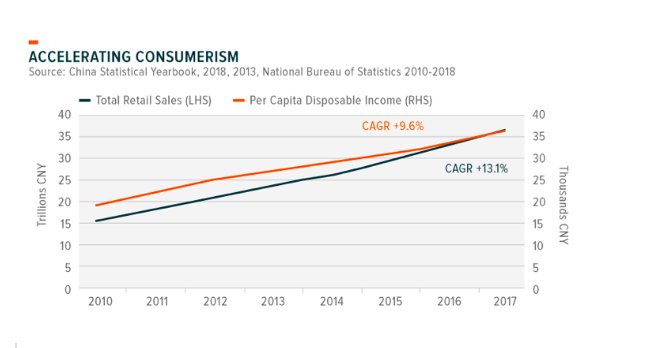

- Consumer Trends: As a percent of GDP, consumption has risen faster than overall GDP growth, yet remains lower than most other middle-income countries. According to the National Bureau of Statistics (NBS), retail spending alone rose 9.1% y-o-y in 2018 while GDP increased 6.6%. Looking forward, consumption is forecasted to continue growing by an average of 6% annually as the country becomes more consumption-oriented.8

- Consumption Stimulus: Broad policies in China aim to reduce the country’s reliance on export-driven growth and high savings-model towards one driven primarily by consumption. Chinese fiscal stimulus, including the recent Individual Income Tax (IIT) cuts, VAT tax cuts, and corporate tax cuts, are designed to increase overall consumption spending, especially across areas that dovetail China’s broader national strategy. This includes the expansion of telecom infrastructure, enabling consumers to connect to e-commerce, travel and entertainment platforms. Key national strategies like the Made in China 2025 (MIC), Belt and Road (BRI), Broadband China, and Internet Plus initiatives, all complement the consumption story by facilitating a greater build out of infrastructure integral to the growth of the Consumer Discretionary sector.

- Deeper Pockets: China’s youth tend to have deeper pockets to fund their more liberal spending habits and benefit from steadily rising wages and the lingering impact of China’s one child policy. According to Bain & Company, 57% of funding for luxury spending by Chinese millennials come from their parents, and around 38% coming from their own pockets.9 Recent trends suggest that this spending may be most concentrated within the luxury goods, retail, and travel segments. 10 Despite recent trade tensions and decelerating economic growth, the luxury market experienced its second straight year of 20% growth in 2018, with Chinese consumers projected to account for half of luxury good purchases by 2025.11

- Technology Adoption: Despite a lower percentage of internet penetration, China’s substantially larger population and avid adoption of new technologies has resulted in 3x as many internet users, 3.75x more mobile phone users, and 7.5x amount spent on mobile transactions compared to the US.12 These online consumers’ rapid 4G adoption rates provide the backbone for data-intensive media consumption, mobile payments, and chat features.

Leapfrogging

Part of this adoption speed is due to technology ‘leapfrogging’, which enables developing markets to quickly adopt the latest technology, rather than needing to replace well-entrenched habits or infrastructure.

For example, Chinese consumers have leapfrogged credit cards, spending over $15 trillion in mobile payments during 2017, compared to $2 trillion spent in the US or $377 billion five years earlier.13

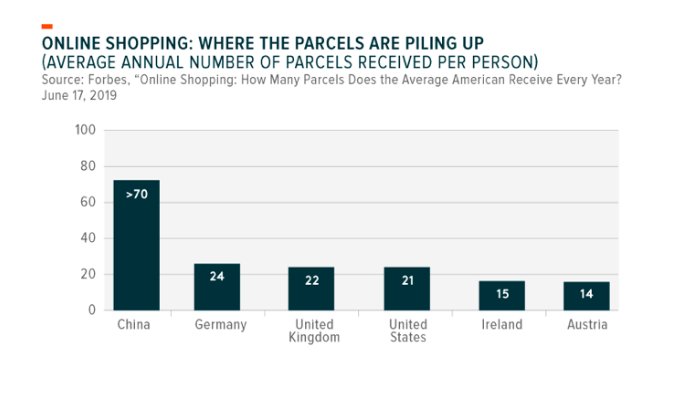

According to a recent study, China has the highest adoption rate of fintech globally, explaining the rapid growth of mobile payments and e-commerce in China. From the e-commerce perspective, data on parcel deliveries globally reflect booming demand for e-commerce with Chinese consumers receiving on average 70 packages a year in Beijing and Shanghai, compared with just 21 on average across the US.14

Conclusion

The future of the Consumer Discretionary sector is inherently tied to major macro-economic, demographic, and political trends, which will affect segments like e-commerce, travel, education, and health and wellness.

As China transitions to a middle-income economy, the government will increasingly count on the enormous middle class to continue to drive the country’s growth via increasing levels of consumption.

Given the size of the consumer base and their unique preferences, we believe domestic firms within the China Consumer Discretionary sector are among the best positioned to benefit from this shift, making an allocation to the sector a potentially attractive way to play this long-term theme.

Related ETFs

CHIQ: The Global X MSCI China Consumer Discretionary ETF seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the MSCI China Communication Services 10/50 Index.

Photo Credit: Michael Gwyther-Jones via Flickr Creative Commons

1. Bloomberg as of Jun 4, 2019.

2. Ibid.

3. The World Economic Forum, “Five trends shaping the future of e-commerce in China,” Sep 17, 2018.

4. PwC, “The continued momentum of e-commerce growth in China,” 2018.

5. China Daily, “China Auto Sales expected to Drag in 2019,” Jan 14, 2019.

6. China Statistical Yearbook, 2018, 2013. The National Bureau of Statistics, 2010-2018.

7. The Center for Strategic and International Studies (CSIS), China Power Project, as of Jan 25, 2019.

8. The World Economic Forum, “Future of Consumption in Fast-Growth Consumer Markets: China,” Jan 2018.

9. Bain & Company, “What Powering China’s Market for Luxury Goods,” Mar 18, 2019.

10. Bloomberg, “China’s 300 Million Senior Citizens Need Health Care,” Jul 28, 2018.

11. The Financial Times, “Luxury brands focus on China’s younger consumers,” Apr 12, 2019.

12. KKR, “China: A Visit to the Epicenter,” Aug 7, 2018; and United Nations ITU, Data as of Jan 27, 2019.

13. The Wall Street Journal, “Alibaba and Tencent Set Fast Pace in Mobile-Payments Race,” Sep 22, 2017; iResearch; Forrester Research.

14. Forbes, “Online Shopping: How Many Parcels Does the Average American Receive Every Year?” Jun 17, 2019.

A slightly longer version of this article appeared in the Global X Research & Insights blog on July 9, 2019:

Disclosure:

Investing involves risk, including the possible loss of principal. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Securities focusing on a single country and narrowly focused investments may be subject to higher volatility. CHIQ is non-diversified.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. Global X NAVs are calculated using prices as of 4:00 PM Eastern Time. The closing price is the Mid-Point between the Bid and Ask price as of the close of exchange. Closing price returns do not represent the returns you would receive if you traded shares at other times. Indices are unmanaged and do not include the effect of fees, expenses or sales charges. One cannot invest directly in an index.

Carefully consider the Fund’s investment objectives, risks, and charges and expenses before investing. This and additional information can be found in the Fund’s summary or full prospectus, which may be obtained by calling 1-888-GX-FUND-1 (1.888.493.8631), or by visiting globalxfunds.com. Please read the prospectuscarefully before investing.

Global X Management Company LLC serves as an advisor to Global X Funds. The Funds are distributed by SEI Investments Distribution Co. (SIDCO), which is not affiliated with Global X Management Company LLC. Global X Funds are not sponsored, endorsed, issued, sold or promoted by MSCI, nor does MSCI make any representations regarding the advisability of investing in the Global X Funds. Neither SIDCO nor Global X is affiliated with MSCI.

{kind=link}

{kind=link}