Matthew J. Bartolini, CFA, Head of SPDR Americas Research

As the first half of 2019 is coming to a close, the year-to-date market rally has extended beyond most investors’ expectations. Our 2019 Midyear Investor Survey gave us a great opportunity to hear how investors are feeling about this surprisingly strong rally—and how they’re positioning their portfolios for the rest of the year.

Here’s what we learned after surveying more than 500 investment professionals:

Cautious optimism abounds

Investors are still feeling optimistic about US equity markets, with the majority of respondents indicating they believe that the S&P 500® will increase by over 5% for the year. If this holds, given that the market was up around 15% when the survey was taken, it would translate into a roughly 20% return for 2019.

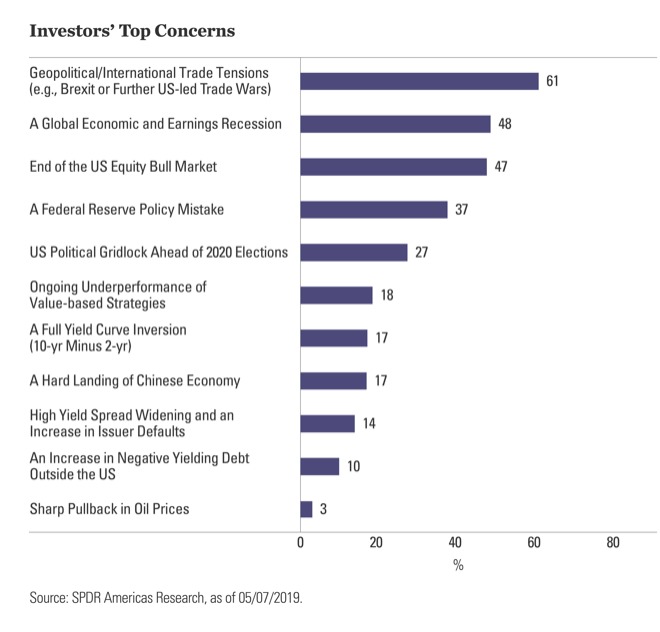

This would be the best single-year return since 2013—a time when interest rates were still held to the zero bound and the Federal Reserve was still conducting quantitative easing. As monetary policy is different today, however, investors’ optimism is tempered by a healthy dose of caution—mainly for macro reasons—as evidenced by their top three reported concerns:

- Geopolitical/international trade tensions

- A global economic and earnings recession

- End of the US equity bull market

For more, please read the rest of the post originally published on the SPDR Blog on May 16.

Photo Credit: Teresa Boardman via Flickr Creative Commons

About the Survey – A total of 529 investment professionals completed State Street Global Advisors’ online midyear survey, the goal of which was to determine the investment concerns and client portfolio considerations that are in the forefront of their minds. The survey was fielded in May 2019. The respondents represent a variety of investment professional segments, holding a wide range of assets under management.

This material is from State Street Global Advisors and is being posted with State Street Global Advisors permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Advisors is not endorsing or recommending any investment or trading discussed in the material. The opinions expressed may differ from those with different investment philosophies. This material is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed or relied on as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation to buy, sell or hold such security. This material does not and is not intended to take into account the particular financial conditions, strategies, tax status, investment horizon, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}