By Steven Levine, Senior Market Analyst, Interactive Brokers

The outlook for the global semiconductor sector appears upbeat, despite gloomy earnings outlooks and potential slowdown in consolidation in my view.

Trade tensions between the US and China have infiltrated the semiconductor space, spurring fears about companies’ future financial prospects.

Uncertainties over China’s production capabilities and dependency on high-end chips have risen, for example, along with jitters about protracted feuds and tariffs between the world’s two dominant economies.

Trade Tensions

Tammy Kiely of the Goldman Sachs Investment Banking Division recently noted that as “trade tensions continue to intensify, semiconductors, one of the world’s most important and complex industries, have emerged as a key point of contention.”

These frictions raise the stakes for an industry that has received heightened attention from a regulatory perspective, and Kiely said that given the size of the sector, as well as “its importance from a technology and military perspective, many countries are very focused on their semiconductor assets.”

Indeed, trade-related uncertainties appear to have increased risks related to the global supply chain, as well as international product sales, while generally posing a threat to the recent wave of consolidation in the industry.

Share Slide

South Korea’s Samsung Electronics, for example, saw its stock shed around 3% recently after it unleashed a profit warning for the fourth quarter of 2018.

The company released relatively rare expectations of a quarterly operating profit decline of roughly 29% year-on-year, as well as a sales decline of about 11% over the same period.

The news followed hot on the heels of U.S. tech giant Apple’s (AAPL) downwardly revised earnings guidance earlier in January, including around 10% less revenue than initially expected.

The alert, which was the firm’s first in almost 20 years, was largely a casualty of U.S.-China trade relations.

Tim Cook

Apple CEO Tim Cook noted that while the company anticipated “some challenges in key emerging markets, we did not foresee the magnitude of the economic deceleration, particularly in Greater China.”

In fact, the majority of Apple’s revenue shortfall to its guidance, and over 100% of its year-over-year international revenue decline, occurred in Greater China across iPhone, Mac and iPad.

Cook said that as China’s economy began to slow in the second half of 2018 – marked by the second lowest GDP growth during the September quarter in the past 25 years – was impacted by rising trade tensions with the U.S.

He added that as “the climate of mounting uncertainty weighed on financial markets, the effects appeared to reach consumers as well, with traffic to our retail stores and our channel partners in China declining as the quarter progressed.”

FX Headwinds

Meanwhile, other factors for Apple’s downbeat guidance included foreign exchange headwinds. as well as some supply constraints due to the introduction of several new products.

These constraints included sales of the Apple Watch Series 4, iPad Pro, AirPods and MacBook Air.

Dave Novosel, a senior analyst at corporate bond research service firm Gimme Credit, noted that the trade disputes “have not helped,” although the US has not imposed tariffs on smartphones from China. He suggested the tensions will likely pose potential future pressure on sales as well.

Revenue Drop

Gimme Credit expects Apple’s full year revenue will drop by around 1.5%, and that margins will continue to weaken as they have over the past couple of years.

Novosel said that part of the margin erosion may come from lower pricing as Apple strives to maintain its market share, with EBITDA likely to fall by US$2.5bn or more.

He added that “amazingly enough, since debt is not likely to change, leverage will remain at 1.4x.”

Trade Spat

In addition to earnings scares, trade disputes have also thrown a wrench into deal-making, notably after President Donald Trump prohibited Qualcomm (QCOM) in March 2018 from completing its proposed $117 billion merger with semiconductor supplier Broadcom (NAVGO).

The decision came after Trump issued an executive order in mid-March citing “credible evidence” that Singaporean domiciled Broadcom, along with its partners, subsidiaries, or affiliates, “might take action that threatens to impair” U.S. national security through exercising control of Qualcomm.

As such, he quashed the proposed takeover of Qualcomm and sent the chipmaker a presidential order to immediately and permanently abandon the deal.

Reversing course

In the meantime, while the industry has undergone a bout of deterioration, recent developments between the two world powers seem to have helped the PHLX Semiconductor Sector (SOX) reverse course.

Asbury Research chief market strategist John Kosar, for example, observed in late December that broad market weakness had pushed the market-leading SOX below 1150 support.

Although a test of 1020 appeared to be the next step, the index had retraced some of those losses, gaining around 7.35% since December 24.

Growth Prevails

Moreover, growth in the semiconductor space is likely to continue, despite gloomy earnings outlooks and potential slowdown in consolidation.

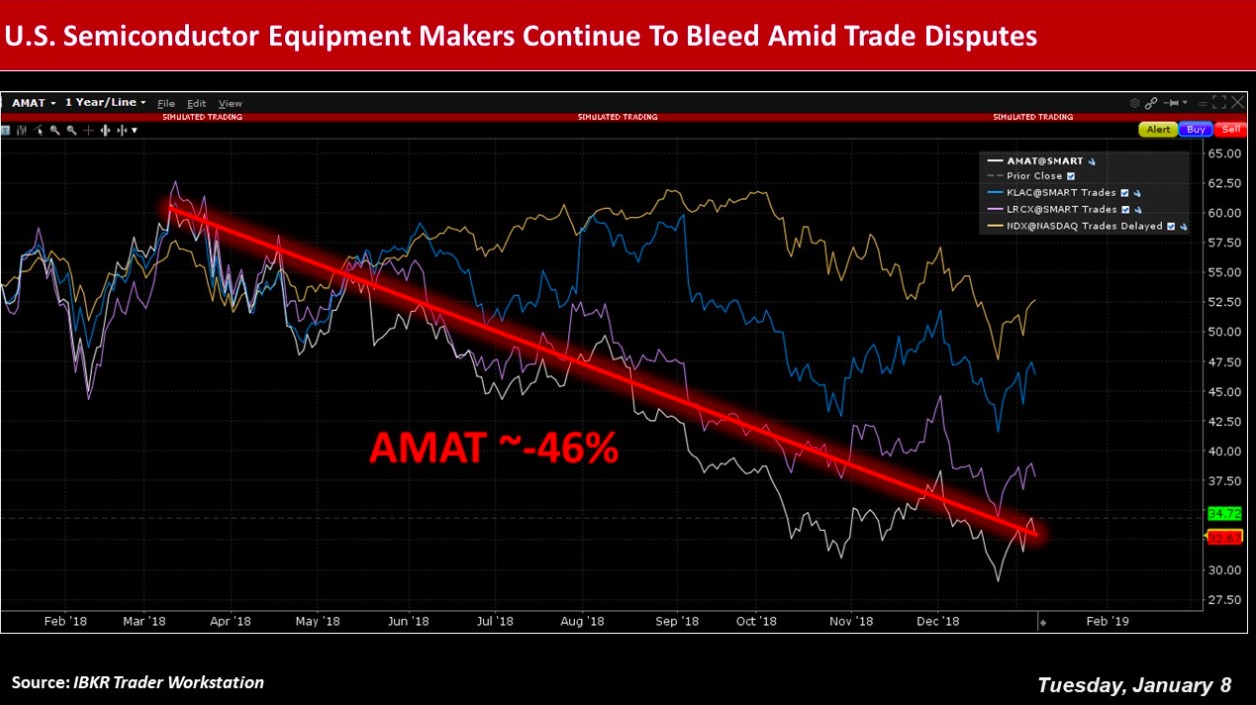

According to Moody’s Investors Service, Chinese tariffs, for example, would have only a small impact on US semiconductor equipment makers.

Moody’s analyst Richard Lane recently said that “China’s tariffs and/or trade restrictions would have only a limited impact” on Applied Materials (AMAT), Lam Research (LRCX) and KLA-Tencor (KLAC) given that indigenous Chinese customers represent only 6%, or $1.8 billion, of their annual aggregate revenue.

China Exposure

Among the three rated semiconductor equipment makers, Moody’s noted that Applied Materials is the most exposed to the Chinese market.

Including equipment, services, spare parts and flat panel display equipment, the firm currently derives about 7% of its revenue from indigenous Chinese customers.

Including equipment, services and spare parts, Lam Research generates an estimated 5% and KLA-Tencor 4% of revenue from China.

Headwinds

Despite the material losses, Applied Materials’ earnings have been decent.

In fiscal 2018, Applied grew its net sales by 19% to $17.25 billion, with gross margin of 45.3%, operating income of $4.8 billion, and earnings of $3.23 per share.

Applied Materials CEO Gary Dickerson noted that each of the company’s major businesses delivered double-digit growth “despite challenging conditions in the second half of the year.”

He added that while “near-term market headwinds remain, overall industry spending remains robust, and we are focused on positioning Applied Materials for the long term, expanding our role in the A.I.-Big Data era and winning the major technology inflections ahead.”

Takeaway

In fact, World Semiconductor Trade Statistics (WSTS) expects the global semiconductor market to grow nearly 16% in 2018 to $478 billion, with growth anticipated across all geographic regions.

The organization said its upbeat outlook reflects growth in all major categories, with “extraordinary growth” from Memory at 33.2%, followed by Discretes with 11.7% and Optoelectronics with 11.2%.

WSTS added that for 2019, all regions are expected to grow, with the overall market up 2.6% to US$490bn.

Photo Credit: Ian Peters via Flickr Creative Commons

The author does not hold any positions in the financial instruments referenced in the materials provided.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR or IBKRAM to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The author believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

{kind=link}

{kind=link}

{kind=link}