By: Yale Bock, Y H & C Investments

Bananas are an interesting food for a number of reasons. According to the all-knowing and noted philosopher ChatGPT, its unique characteristics include being nutritionally rich, botanically unusual, widely available, and potentially vulnerable to genetic uniformity. Specifically, bananas are rich in potassium and high in fiber. They contain tryptophan, a parent of serotonin (can boost your mood). Probably more important for those of us with a sweet palate, some of their most noteworthy presentations include the banana split sundae, banana cream pie, banana bread, frozen bananas, chocolate dipped bananas, and the state fair original, fried bananas.

With this information about bananas, a curious reader might be asking themselves, what gives? It is nice you are telling me about bananas, but why does that matter to someone who is interested in the financial markets? Well, I’m glad you are curious.

You see, for anyone involved with money, two important considerations are risk and return. In the current environment, where the idea of risk has been frowned upon, what the vast majority of investors care about are the big R. Returns. Returns. Returns. Returns. The only thing that matters, ignoring the two months ago period of April, is you guessed it, RETURNS. I would argue that is an incomplete approach, but this is what we currently have, so let’s link these two subjects, bananas and returns.

According to the legendary businessperson HB, when asked “How is business?” he replied, ‘It is like bananas, it comes in bunches.’ Guess what? The same thing can be said for returns, especially in the capital markets, specifically the stock market. It is my experience that maybe the most difficult part of investing is the long lag time of investment returns relative to when money is laid out to purchase an asset. Stocks can sit dormant for a long time with nothing happening to the price. They will trade in a range which is not glamorous and make no headlines. Note, we are not talking about the underlying business, which is what is important. It is not that the stock is not important, but it ultimately is a reflection of what takes place in the business. Business performs well; stock goes up. Business does not do well, stock goes down. Me Tarzan, you Jane. Oops, I digress.

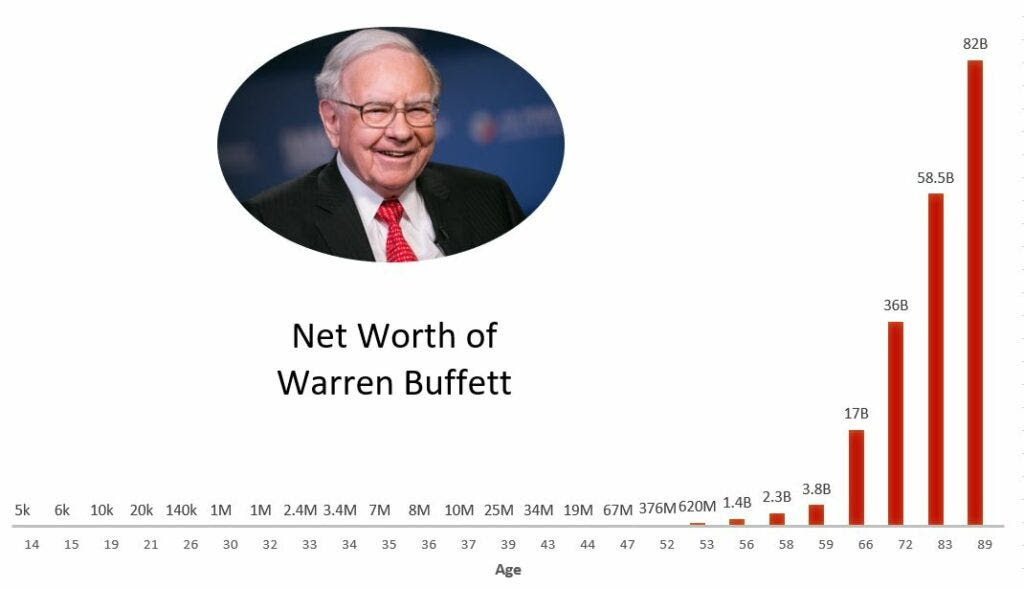

In looking at returns, probably the best example to use is the chart of the net worth of Warren Buffett. Here you go-

Source: https://yhcinvestments.substack.com/p/y-h-and-c-investments-july-2025-update

One notices those big red lines at the end of the chart. With this astute observation in hand, a key point is the GOAT continued to amass money throughout his career. Buffett constantly saved, tucking businesses and cash away, reinvesting capital into stocks and within each of the owned subsidiaries, and took profits opportunistically. Notice we did not mention tax efficiency. Don’t think Uncle Warren wasn’t tax efficient, either. Growing wealth is actually pretty straightforward: save, invest, save, invest, save, invest, save, invest. Please understand this is a simple but difficult task. It is hard to save, be disciplined, and not worry about keeping up with the neighbors. It is unreasonable to expect anybody to be as good an investor as Warren Buffett. It is reasonable to believe with discipline, one can save, invest, and be patient. Do it for a long time. Try and be understanding about the unpredictability and timing of returns. Remember, they come in bunches, just like bananas.

Originally posted on July 1, 2025 on Yale Block’s blog/ newsletter

PHOTO CREDIT: https://www.shutterstock.com/g/Ivan+Zelenin

VIA SHUTTERSTOCK

DISCLOSURES:

Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.

Past performance is no guarantee of future results, and all investments involve the risk of loss, including loss of principal and a reduction in earnings.