President Donald Trump’s promised tax reform and infrastructure spending splurge have given global investors reason for cheer in 2017.

Yet, when it comes to future global growth and commodity prices, the economic slowdown in China is arguably the bigger story long-term.

And it’s one investors would be wise to pay attention to, in my view.

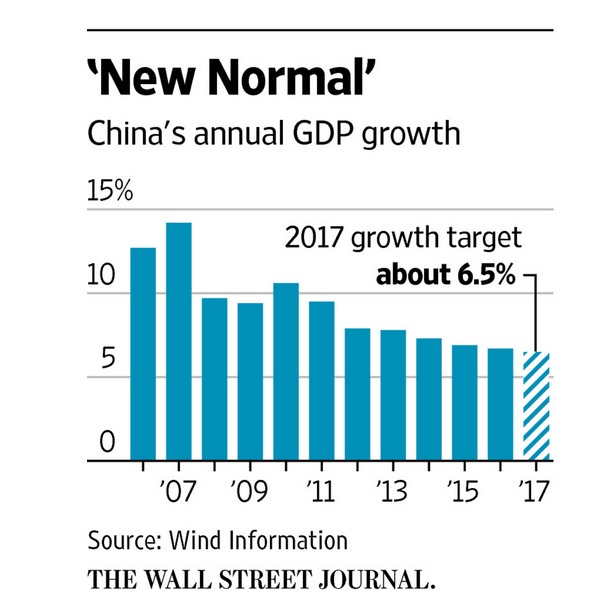

Cooling Off

China remains a big contributor to the world economy, but it’s no longer the high-flier it once was.

The days of double-digit GDP growth are over and it can no longer afford debt-fueled, infrastructure spending to keep the economy in high gear.

In a speech before the National People’s Congress, Premier Li Keqiang set a new blueprint for the Chinese economy.

Slippery Slope

Chinese leaders are now aiming for growth of 6.5% rather than last year’s range of 6.5% to 7%.

That’s still impressive, until you consider that China is still a developing economy and has seen its growth steadily decelerate since the 2008 global financial crisis.

Stock Slump

Chinese stocks traded at domestic exchanges in Shanghai and Shenzhen are up about 14% over the last year.

But that’s way off the highs in mid-2015. Chinese stocks cratered in early 2016.

Take a look at this chart of the Shanghai Shenzhen CSI 300 Index.

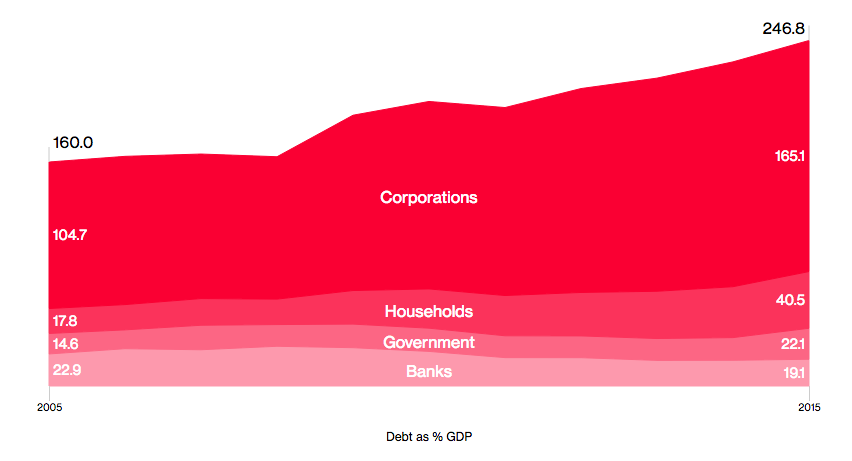

Debt Bubbles

Chinese authorities are trying to defuse what many believe is a property bubble in major cities along coast.

Easy credit has resulted in a surge in home loans and household debt.

That matters because the property market accounts for about 15% of China’s economy.

Zombies

What’s more, China’s total debt load has spiked up since 2008 and is now approaching 250% of GDP.

The heaviest debt concentration is in the corporate sector, particularly among state-owned enterprises (SOEs.)

I think China isn’t facing an immediate crisis. But no longer can it rely on borrow-and-spend, infrastructure projects to power the economy.

Capital Outflows

Finally, Chinese leaders have to worry about a big exodus of money out of the country.

Since China’s shock yuan devaluation in August 2015, some $1.2 trillion-plus has left the country, according to estimates from Bloomberg Intelligence.

That’s a worrisome trend if it accelerates, in my opinion.

Takeaway

I think global investors need to pay attention to China as it slows down and transitions to a more sustainable growth path.

This risk is that the transition is a bumpy one or triggers a hard landing.

Yes, Trump’s management of the US economy is crucial to asset prices over the next few years.

The China story, however, will matter for decades to come.

Photo Credit: Danijel-James Wynyard via Flickr Creative Commons

{kind=link}