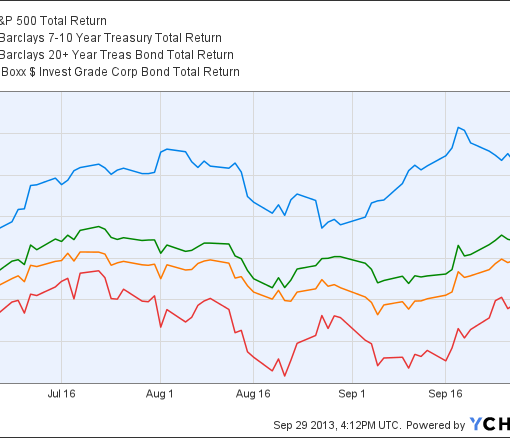

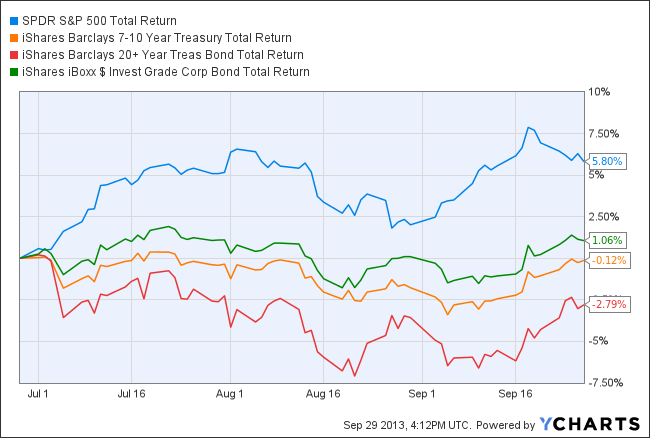

After the recent sudden downward market volatility, we believe that inflation fears are much less present in the current market environment.

This is a change from our thinking as recently as a few weeks ago.

The argument for an inflationary environment, including a growing economy, a small rise in interest rates, and increasing velocity in the money supply, have been eclipsed by a slower global economy, particularly in emerging markets.

Fed Shift

We also believe that the Fed will not raise rates in September as previously thought.

Lower commodity prices, rising oil production, and a strong dollar are all contributing factors to this intermediate term view.

As a result, and to hedge against further declines in equities (which, we believe will result in lower interest rates), we have removed the short term inflation-protected Treasury (TIPS) position in the model portfolios.

Bond Positions

Instead, we have bought more of our intermediate term bond positions and increased our allocation to our tactical bond allocation ETF managed by DoubleLine.

While we may give up some loss in the longer duration of the aggregate bond position should rates increase, this trade is intended to hedge against losses from further equity declines rather than to gain more yield from fixed income.

We retain our fixed income exposures in short corporates and non-US sovereign hedged bonds and some smaller exposures to high yield bonds in our more conservative ETF models.

These moves also move us closer to the aggregate bond index exposure.

Photo Credit: Day Donaldson via Flickr Creative Commons

The investment holding discussed in this article are current as of August 31. There is no assurance that the investment adviser still holds these investments.Further, the reader should not assume that any investments identified were or will be profitable or that any investment recommendations or that investment decisions we make in the future will be profitable.

{kind=link}

{kind=link}