Mid-cap companies should be a key component of a well-diversified portfolio, in my opinion. While mid-cap stocks are positively correlated with small- and large-cap stocks, they still offer diversification benefits for a multi-asset portfolio.

Furthermore, mid-cap stocks as an asset class have demonstrated better historical returns than small- and large-cap equities.

Investing in mid-cap stocks gives you exposure to mid-sized companies ranging in size between $1 and $10 billion in market capitalization.

Some of today’s leading brand names such as from Alaska Airlines (ALK), Autozone (AZO), Domino’s Pizza (DPZ), Hershey’s (HSY) and Under Armour (UA) are all mid-cap companies.

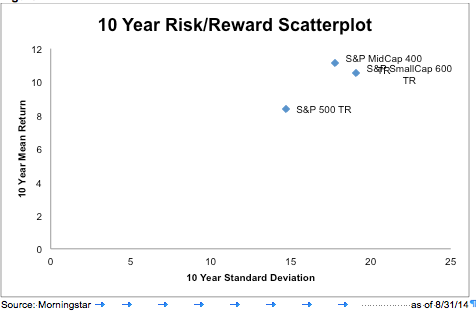

These middle-of-the-pack players often come with less risk than small caps and comparable risk to large caps.

Mid-cap advantage

Mid-cap companies tend to receive less coverage by Wall Street analysts, giving investment savvy active managers the ability to add significant value. In my opinion, a quantitative approach is particularly effective as it can objectively identify opportunities among rising star small-cap names and fallen-out-favor large cap names.

Furthermore, I believe mid-cap names generally have more robust growth characteristics than their large-cap counterparts, with more seasoned management teams, better operating histories, and greater liquidity than small caps.

Including mid-cap exposure in an overall portfolio allocation is a proven diversifier for increasing returns while minimizing risk given its favorable risk-reward characteristics.

In my opinion, Covestor’s EQM Capital Midcap Quant portfolio is one way provide active exposure to mid-cap stocks in your investment portfolio. The portfolio is about 5.1% net of fees versus 6.5% for the S&P Midcap 400 Index through September 15.

Relative to the benchmark, the portfolio is more concentrated than the S&P index, typically holding 20 to 25 names in the portfolio and thus providing more opportunity for generating alpha.

Bottom-up stock picking is the foundation of EQM Capital’s investment process. Companies in the mid-cap universe are ranked based on multiple factors that drive excess return including: fundamental forecasts, financial results, and market sentiment. Based on those inputs, companies become candidates for purchase.

Top performers

Although market results can never be assured, some of the top-performing mid capitalization names identified by our investment process this year include Emerge Energy Services (EMES) and Phillips 66 Partners (PSXP).

Another top name in the portfolio is consumer packaged food and beverage company Whitewave Foods (WWAV), whose soy-based and organic product mix is generating strong growth and higher margins.

Specialty pharma company Salix Pharmaceuticals (SLXP) has also produced strong results fueled by its strong gastrointestinal drug franchise. It has also been the subject of merger speculation.

Some of the retail-related names in the portfolio have underperformed year-to-date as the consumer environment continues to be selectively challenged. Designer handbag and clothing manufacturer Kate Spade (KATE) and barcode scanner manufacturer Zebra Technologies (ZBRA) both fall into that category.

Going forward, there are exciting opportunities within the mid-cap segment as EQM Capital’s investment process continues to identify high growth companies with stable company characteristics and reasonable valuations.

Whereas year-to-date the mid cap index trails the S&P 500 Index, on a longer term basis it is possible, in my opinion, to make the case mid cap stocks should be a key component of a well-diversified investment portfolio.

Photo Credit: royalscottking, Flickr Creative Commons

DISCLAIMER: The investments discussed are held in client accounts as of August 31, 2014. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.