This week’s market decline that led to rising volatility and implied correlations does not scare John Gerard Lewis, manager of the Stable High Yield investment model at Covestor.

This week’s market decline that led to rising volatility and implied correlations does not scare John Gerard Lewis, manager of the Stable High Yield investment model at Covestor.

It’s simply a microcosm of things to come, he says. Market gains spurred by economic stimulus are not going to last forever, which is why he is positioned to try to ride out a mediocre stock market over the next several years.

“The market has been so good this year because of artificial stimulus,” Lewis says. More quantitative easing is simply not a valid reason for a rally. At some point, the chickens have to come home to roost on easy money.”

Lewis says his market outlook is close to that of Bill Gross at PIMCO, as well as Forbes columnist Gary Shilling, who says if we aren’t in a recession already, we are getting very close.

Lewis is not suggesting that stocks are overlooking a cliff, though. He expects to see a middling stock market over the next several years that will be kept somewhat afloat by loose Fed policy.

Yet it won’t be a cyclical bull market, he says, meaning that gains on the S&P 500 may be disappointing.

As a result, Lewis has positioned his Stable High Yield strategy in low volatility investments that he says still have high return potential. About 55 to 60% of his model is in mortgage REITs, and the other 40 to 45% are in short-term bond investments that tend to move less than the S&P 500.

“For investment purposes, I view mREITs collectively as a desirable component of a portfolio that can, if properly constructed, produce returns that approximate the average annual historical return of stocks during protracted periods of middling stock market performance,” he says. “As the stock market declines, my investment model should not fall as much — just as it doesn’t rise as much when the stock market is on an upswing.”

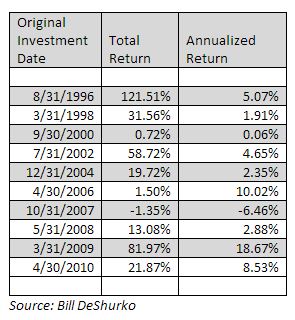

His target annual total return for the investment model is 10%; you can find his latest performance data here, or call us for more information.

Certain of the information contained in this presentation is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The manager believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

![Marty Leclerc: Bonds no, Cisco and Dupont stock yes [Video]](/content/default.jpg)