A potential “face-ripper”: That’s the kind of rally technical analyst JC Parets thinks we could see for natural gas at some point, possibly benefiting stocks in that sector.

It’s true, gas is historically cheap relative to oil. And gas prices are on the upswing relative to crude in recent weeks.

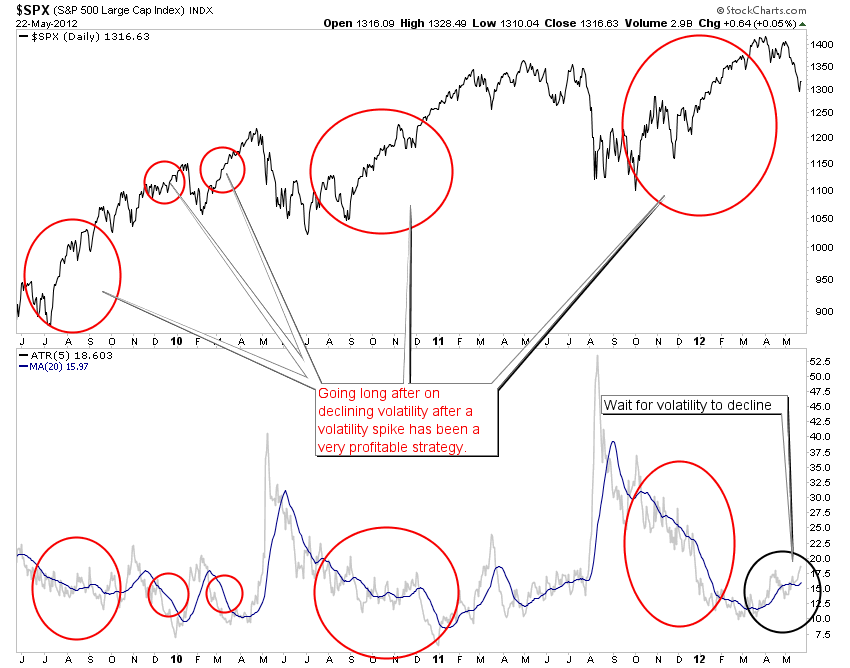

Source: Stockcharts.com

What is not clear, though is if there is a fundamental catalyst that will change the industry dynamic any time soon. Some of the big pipeline projects that would allow more liquefied natural gas to be exported from the U.S. are not scheduled to be on line for several years. It might happen for a long time, if it happens at all.

But you don’t have to time the face-ripper to invest in the sector, says manager Tyler Kocon, who runs the Covestor Bakken Shale model. Some of his investments in the energy group are companies that have exposure to both gas and oil, and can switch production between the two.

One such stock in his model is Synergy Resources (SYRG). Kocon says 43% of its reserves are in natural gas, and 53% in oil. Yet in the first quarter, oil accounted for more than 80% of its total oil and gas revenue, as the company was able to benefit from relatively high oil prices.

Contract driller Patterson Energy (PTEN) can switch back and forth, as well. It’s been under lots of pressure amid a gas pumping downturn. Yet Kocon notes that there has been “lots of value destroyed” in the stock. From a technical viewpoint, volume support rests at around $14. Also, here is a recent defense at SeekingAlpha.

Source: Stockcharts.com

Source: Stockcharts.com

One additional name to keep an eye on is Heckmann Corp. (HEK), a provider of services including water for fracking. The company had been garnering almost all its revenue from the gas side of the business, although Kocon says it has now switched and is garnering 62% from the liquids side.

So even if the face-ripping gas rally never materializes, Kocon says there is the potential for strong oil revenue from many of his energy investments.

{kind=link}