By:

Kyle Murray, Investment Strategist

Dane Smith, Head of North American Investment Strategy & Research

AI investment fuels a $1.1 trillion capex surge in the S&P 500, with IT returns soaring post-tariff. Meanwhile, AI transforms marketing by making high-quality ad creation affordable and narrowing the gap between big brands and small businesses.

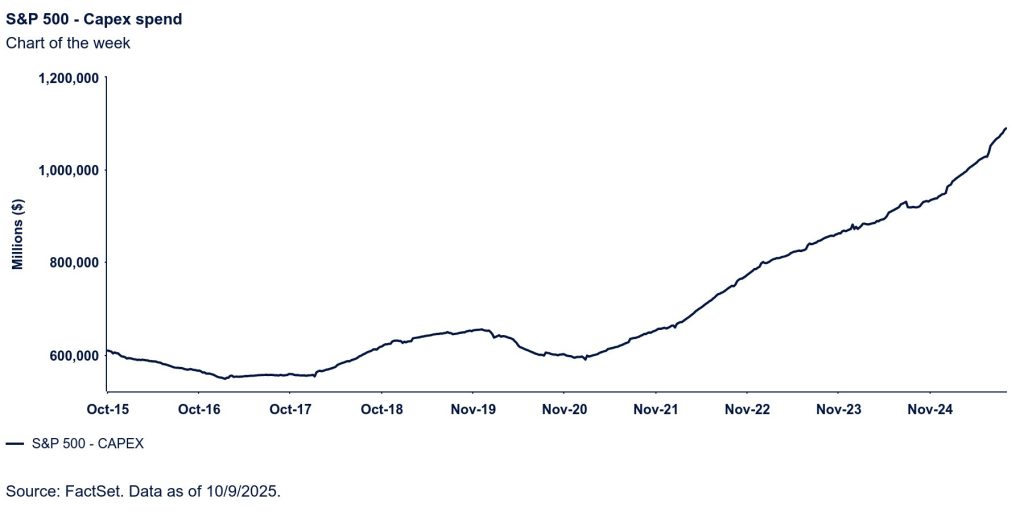

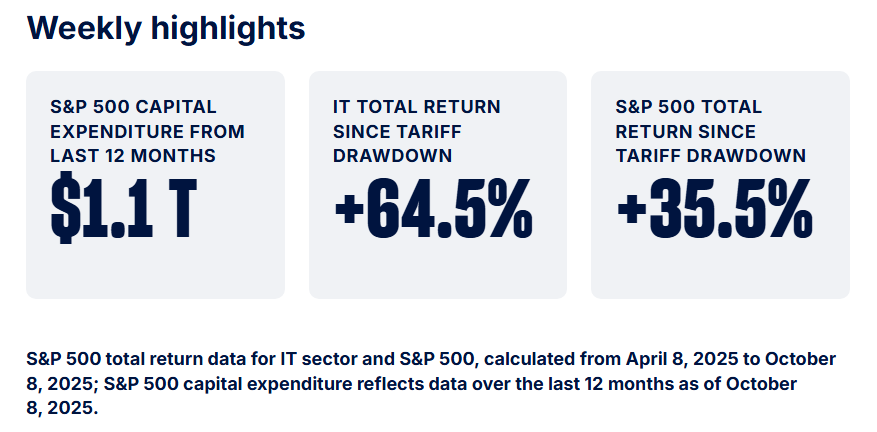

The surge in S&P 500 capex spending in 2025 has surpassed even the highest expectations for the year, with estimates putting total AI-focused US Capex at ~$400 billion, up from $320 billion in February.

This extraordinary hype and investment have drawn critics in droves. Many point to AI’s “circular economy” dynamic, where top companies trade billions of dollars back and forth, resulting in no real gain. Others argue that the technology will not be as impactful as predicted.

So, where will AI’s impact be felt? Will it manifest in new revenue streams or improved margins? Additionally, which sectors will benefit from this revolutionary technology—and when?

The attention economy

One area already undergoing significant transformation is the attention economy. Each year, over $300 billion is spent on online advertising, while households contribute another $57 billion toward digital entertainment via streaming services. The attention economy centers on the idea that while the supply of information has surged, the demand for that information has remained relatively static. In fact, consumer attention has become increasingly fragmented, with preferences shifting toward short, easily digestible formats. In this landscape, attention—not information—is the true currency. Companies now compete not just to create content, but to capture and retain consumer attention, which ultimately determines what gets consumed and how it shapes behavior.

It’s no surprise, then, that brand recognition is critical. Platforms that capture the world’s attention can recommend tailored content—often preemptively—outside of a consumer’s conscious awareness. Additionally, AI can be used to optimize both the timing and the amount spent, helping to maximize return on investment in advertising dollars. Rough estimates suggest that high-end users consume as many as 5,000 to 7,000 advertisements per year. The steady revenue stream from advertisers enables larger players to remain formidable competitors, backed by substantial capital resources.

However, marketing R&D budgets are poised for a massive deflationary cycle, as AI video creation continues to exceed expectations. For example, ChatGPT’s latest “Sora” development has crushed forecasts. Now, even small businesses can produce high-quality, complex video stories that would have been impossible prior to 2025 due to high costs and extensive time commitments. Storyboards can come to life with a simple prompt, and some—such as the Coca-Cola AI-Generated Christmas Ad—are already employing the technology for final cuts.

In short, the cost of producing ad campaigns is falling dramatically, and the gap between what a resource-rich conglomerate can create versus what a small company can achieve is narrowing. Nevertheless, the CPM (Cost per 1,000 ad views) is expected to rise, as the number of companies seeking to advertise grows faster than the available digital attention.

Originally posted on October 13, 2025 on State Street Investment Management blog

PHOTO CREDIT: https://www.shutterstock.com/g/Best4best

VIA SHUTTERSTOCK

DISCLOSURES

State Street Global Advisors Worldwide Entities

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of Kyle Murray and Dane Smith through the period ended October 09,2025 and are subject to change based on market and other conditions. and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

Investing involves risk including the risk of loss of principal.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Currency Risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.

{kind=link}