By: Michael W. Arone, CFA, Chief Investment Strategist

“You must spend money to make money.” — Titus Maccius Plautus

One of the biggest surprises of the first quarter is that European stocks clobbered US stocks. Riding the coattails of the Trump administration’s America First agenda, boundless US exceptionalism was universally forecast for 2025. Yet, European stocks have outperformed US stocks by about 15% year to date.1

It’s difficult to identify the reasons for such lopsided European outperformance. According to the latest GDP estimates from the Organisation for Economic Co-operation and Development (OECD), the US economy is expected to grow by 2.2% this year compared to 1.0% for the euro area. Germany, Europe’s historic engine of economic growth, is forecast to grow at a modest 0.4% this year. Admittedly, the pace of US economic growth is predicted to slow year-over-year while Europe’s is likely to accelerate. But all else equal, higher absolute economic growth should be better for stock market investors than lower economic growth.

Sure, more than a decade of persistent underperformance created a steep relative value advantage for European stocks. In fact, US stocks trade at a 50% price-to-earnings (P/E) premium to European stocks. But this substantial P/E premium may be warranted. US earnings-per-share (EPS) growth is projected to exceed European EPS growth by more than 45% this year. A 50% P/E premium for a nearly equal amount of excess EPS growth is reasonable.

So, if US economic and earnings growth are expected to be better than Europe’s this year, why did European stocks wallop US stocks in the first quarter?

When considering that question, investors should avoid linear thinking. Correlation doesn’t always equal causation. Markets are dynamic. And a number of factors are likely driving Europe’s first quarter outperformance. US stocks are expensive and the economic and earnings outlook is deteriorating. Meanwhile, European stocks are inexpensive and the economic and earnings outlook is improving. After years of trailing US stock market performance, European stocks may finally be experiencing long-anticipated mean reversion. The potential for a ceasefire in the three-year-old Russia-Ukraine war may also be boosting investor enthusiasm for European stocks.

But it’s hard not to conclude that the powerful one-two punch of Mario Draghi’s September report on the future of Europe’s competitiveness and the Trump administration’s early attempt to create a new world order have bullied previously stingy Europe into becoming a spendthrift. Draghi’s recommendations challenged Europe to take the necessary steps to improve its global competitiveness. Trump’s new world order was a wakeup call that forced Europe to reduce its military reliance on the US.

Germany responded strongly in March with an unprecedented $1.08 trillion spending package for civilian and defense investments. European stock prices have soared on expectations that massive fiscal spending and increased competitiveness would produce higher economic and earnings growth throughout the region.

After all, the formula has worked well for the US since 2008.

Whatever It Takes Redux

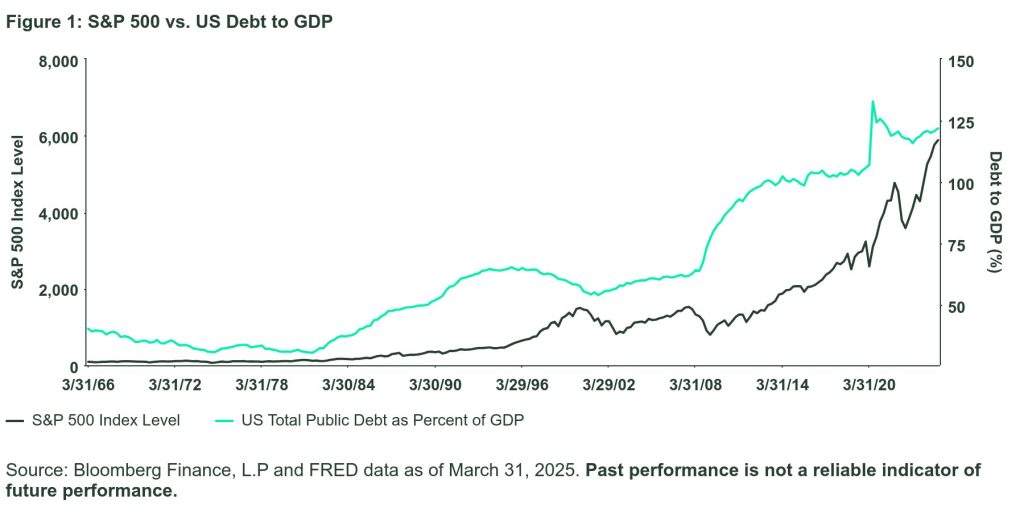

The US debt and deficit as a percentage of GDP has been rising steadily for more than a decade, driven by extraordinary fiscal stimulus in response to the Global Financial Crisis (GFC) and COVID pandemic. During that period, the US economy grew faster — and its stock market performed better — than its developed market peers.

It’s important to reiterate the linear thinking warning. The US economy and stock market have outperformed for a variety of reasons. Falling interest rates, lower corporate taxes, globalization, and the incredible earnings power of technology companies, especially the Mag 7, have led to an almost doubling of US profit margins this century. Other countries also spent aggressively to neutralize the negative consequences from the GFC and pandemic.

But it’s impossible to ignore the significant role that US government spending in cooperation with easy monetary policy has played since the GFC, particularly when the economy was on the brink of catastrophe. According to Strategas Research Partners, US government and government adjacent sectors (i.e., education and healthcare) contributed 73% of job creation in 2023 and 2024 combined. Exorbitant government spending combined with accommodative monetary policy has distorted the business cycle and repelled recession.

Europe has taken notice. Draghi’s report on the future of competitiveness forged a new path for Europe. The Trump administration’s hardball tactics on trade and defense forced Europe to realize what the America First policy meant for its future. Europe must be more innovative, lower energy costs, increase investments, reduce regulation, spend on its own defense, and strengthen trade policy. This will require a stronger, more coordinated fiscal union. Europe is finally demonstrating greater willingness to regroup, reform, and rearm through massive fiscal expansion. This is a big change.

With a number of obstacles in its new path, the rest of Europe may not be able to follow Germany’s early lead. Unlike Germany, many European countries already have large fiscal deficits with negative or no current account surpluses. Structural challenges in the European economy include labor market rigidity, generous social safety nets, and oppressive regulation. Enormous fiscal spending will require a sizeable increase in sovereign debt issuance. This could lead to an unintentional increase in interest rates and stoke inflation.

But these challenges haven’t prevented European stocks from racing far ahead so far this year.

The rise in European stocks has been led by cyclical sectors such as Financials and Industrials. Contrast that with a US stock market decline led by defensive sectors such as Health Care, Consumer Staples, and Utilities. European investors are pricing in a cyclical recovery while US investors are bracing for an economic slowdown, possibly recession.

Admittedly, European stocks may reflect a too perfect outcome. As always, stock prices will adjust accordingly as the economic reality unfolds. But, for now, investors expect greater fiscal spending assisted by European Central Bank (ECB) rate cuts to bolster the economy, earnings, and stock prices. A recipe that has worked well for the US for more than a decade.

My, How Things Have Changed

In the aftermath of November’s US election, investor sentiment was downright euphoric. US exceptionalism was expected to continue unabated. Investors celebrated anticipated tax cuts, deregulation, and fiscal expansion. Instead, post-Inauguration Day the Trump administration prioritized tariffs, immigration, and fiscal constraint through the Department of Government Efficiency (DOGE). This has resulted in heightened policy uncertainty, stock market declines, and growing fears of a US recession.

Investor hopes that Trump’s tariffs would be more bark than bite have given way to the reality that the administration intends to dramatically reset global trade. DOGE has been reshaping the federal government by slashing large numbers of civil servant jobs. And Treasury Secretary Bessent has been preparing markets for a reduction in the US fiscal deficit from more than 6% of GDP to 3% in the next few years. Trump administration officials have made it clear that they are willing to accept some short-term pain for long-term gain and that a little stock market volatility will not deter them from their policy goals of Making America Great Again.

This isn’t an endorsement or an indictment on the Trump administration’s policies. The president’s policies are fundamentally contradictory. Some are likely to boost economic growth and inflation while others could curtail growth and be disinflationary. Pro-growth policies such as tax cuts, deregulation, and fiscal spending are likely coming later this year.

The key point is that for the first time since the GFC, the fiscal stance between the US and Europe is diverging. Shockingly, the US is on a path hurtling towards fiscal austerity. At the same time, Europe is exhibiting a greater appetite for fiscal spending. This is a significant factor behind European stocks outperformance relative to US stocks this year. It also helps explain why US Treasury yields are falling, while German bond yields are rising.

Germany has acknowledged that the post-GFC economic model focused on domestic manufacturing funded by cheap energy costs and an undervalued currency generously supported by the ECB is broken. Wildly, this is exactly what the Trump administration wants to do in the US.

But investors are anxious. Allocations to US equities fell 40% month-over-month in March, the biggest monthly drop on record, according to Bank of America’s latest monthly Global Fund Manager Survey. Fund managers reported being about 23% underweight in US stocks while 39% now hold an overweight position in European equities, up from just 12% last month and the highest level since mid-2021.2

Investors must also take a good long, hard look in the mirror. Capitalist theory proponents believe that government spending is inefficient, wasteful, and sometimes fraudulent. Exactly what DOGE and the Trump administration is trying to eliminate. Most investors believe that capital held in private hands with a profit motive is more impactful for the economy than money spent by the government. Trump administration policy is attempting to shrink the federal government and return that capital to private hands where it will generate much higher rates of return than the government could achieve, boosting economic growth in the process.

So, why have investors flocked to stock markets where governments are spending extravagantly? As the US has passed the fiscal spending baton to Europe, investors have punished US stocks and rewarded European shares.

Regrettably, everybody’s antenna is way up in this uncertain environment. With the temperature and division rising, it feels like everyone wants to fight. I’m not claiming that one fiscal policy is better than another policy. I don’t know what the outcome of all of this will be this year or in the next few years. But I can observe that attitudes toward fiscal spending are diverging between the US and Europe. I can observe how the capital markets are reacting to that divergence. To me, it’s strange. As an investor, I believe that more capital in private hands will produce greater rates of return and economic growth than inefficient government spending. What’s jaw-dropping to me is — why haven’t stock market returns behaved that way? This is worth watching.

Originally posted on April 1, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/FAHMI98

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES:

1 Bloomberg Finance, L.P., as of April 1, 2025.

2 Global Fund Manager Survey, Bank of America, March 7 to March 13, 2025. 171 survey respondents.

DISCLOSURES:

Important Risk Information The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The views expressed in this material are the views of Michael Arone through the period ended April 1, 2025, and are subject to change based on market and other conditions.This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions. Diversification does not ensure a profit or guarantee against loss.

Past performance is not a reliable indicator of future performance.

All material has been obtained from sources believed to be reliable.There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

{kind=link}