By: Kevin Flanagan, Head of Fixed Income Strategy

Key Takeaways

- The U.S. Treasury (UST) 10-year yield could trend toward 5% in 2025, supported by a combination of historical averages and a steepening Treasury yield curve.

- While inflation improvements remain uneven, we believe the Federal Reserve’s (Fed) path of modest rate cuts and economic resilience creates a conducive environment for elevated yields.

- Investors should monitor the spread between the Fed Funds Rate and the UST 10-Year yield, which historically averages +130 basis points (bps), as a key indicator for potential moves in long-term Treasury rates.

With a return to a normal U.S. interest rate setting, the most obvious question that comes to mind is: Where is the UST 10-Year yield headed? As we enter 2025, there has been a lot of conjecture about a return to the 5% threshold. Against this backdrop, I thought it would be a useful exercise to provide the reader with some perspective, and what I feel investors should be looking for in the year ahead.

In my opinion, when trying to determine where yields may be going, one should start at the cornerstone for rates—the macro/Fed landscape. Our baseline case looks for the U.S. economy to continue on a modest/moderate growth path, with further improvement on the inflation front proving to be “bumpy,” to borrow Fed Chair Powell’s description. These two forces have now put the Fed on a path for only two more rate cuts in 2025, based on the December Federal Open Market Committee (FOMC) dot plot.

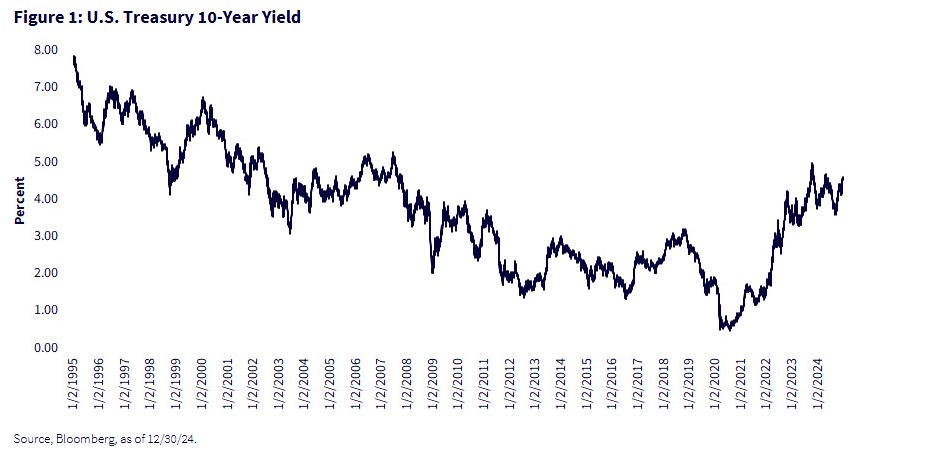

Post-election, the money and bond markets have been trying to also determine how upcoming fiscal policy will fit into the equation. However, this aspect and its potential attendant impact on rates carries more uncertainty. While tariffs can arguably be more easily and quickly implemented, any legislative initiatives take more time and may not be “in the books” until after mid-year, at the earliest. Figure 1 shows the historical trends of the U.S. Treasury 10-Year yield over the past 30 years.

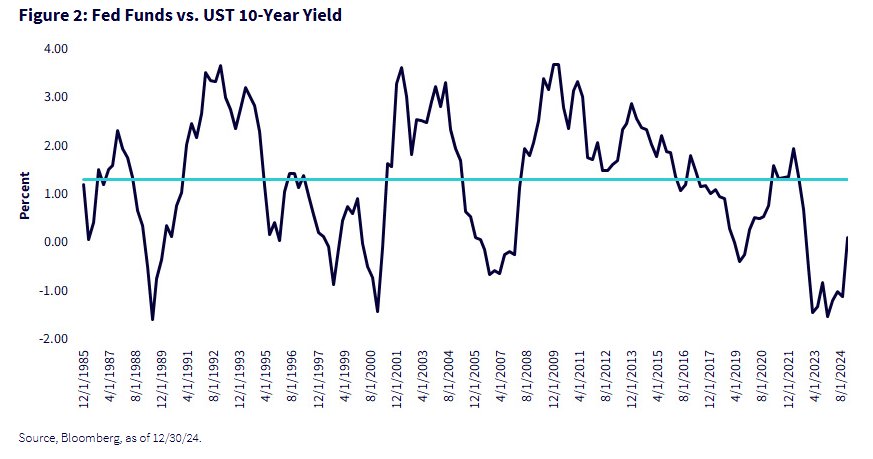

Against this backdrop, let’s go back to the macro/Fed setting and also look at history for some guidance. Let me ask you a question after you look at the above graph: What is the outlier here? Sure, you could go back to 1995–1997 and, say, 6%–8% yields, but I zoom in on the 2008-to-late-2022 period, when the yield fell below 4% during the financial crisis/great recession and ultimately plummeted to a pandemic-low of 0.50% before beginning its ascent to where we are today. Figure 2 compares the Fed Funds Rate with the U.S. Treasury 10-Year yield.

I would argue those two periods are the outliers and that what lies in between is a trading range of roughly 4%–5%. Not only is the macro/Fed backdrop conducive for this trading band, but history once again can teach us a lesson, specifically looking at the spread between the Fed Funds Rate and the UST 10-Year yield. The long-run average of this measure stands at about +130 bps—the UST 10-Year yield is higher than the rate for overnight money.

Investors have recently witnessed the Treasury yield curve un-inverting and moving back into positive territory. In fact, as of this writing, the Fed Funds/UST 10-Year spread came in at +17 bps. Based on the FOMC’s December Summary of Economic Projections (SEP), the median estimate is for Fed Funds to drop to 3.90% in 2025. If the curve continues to steepen in the new year—our base case expectation—and gravitates toward its long-run average, the math tells us that the UST 10-Year yield could be poised to reach the 5% threshold, if not actually a touch above.

Conclusion

After the December FOMC meeting, the UST 20- and 30-Year yields have already reached high watermarks of 4.90% and 4.82%, respectively. Perhaps the UST 10-Year will join the parade, where ultimately, the longest end of the Treasury yield curve all trades at, or above 5%, in 2025.

Originally posted on January 09, 2025 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/ungvar

VIA SHUTTERSTOCK

DISCLOSURES:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}