By: Michael Kramer

We have a hectic week ahead. The Fed meeting is on Wednesday, followed by the Bank of Japan meeting on Wednesday night and Thursday morning in Japan. We’ll also get retail sales on Tuesday and PCE on Friday. A lot is happening this week. After that, there won’t be much activity for the rest of the year. Whatever impressions the market takes away this week will likely drive the final weeks of trading until we head into 2025.

The yield curve has begun to steepen. I posted a video over the weekend discussing the yield curve, which you can find on my YouTube channel. In particular, the 2-10 spread has been widening again. Based on the chart in the write-up, it appears to be forming a bull flag. If that projection plays out, the 2-10 spread could widen to around 85 basis points. This is something to watch closely, especially if the Fed can’t cut rates as much as people expect due to persistent inflation and a relatively stable job market. In that scenario, we’re likely to see a bear steepener, where the 10-year rises relative to the 2-year, driven by higher rates on the long end of the curve.

Interestingly, the real yield curve (based on TIPS) is already positive across the entire curve. That’s an important development. The nominal curve is still inverted, but it’s moving closer to being positive, with the 10-year minus the 3-month Treasury bill turning positive recently. This breakout could lead to a spread as wide as 114 basis points.

The way this steepening unfolds is critical. If the steepening comes from the 10-year rising, it could be problematic for risk assets due to higher long-term rates.

Liquidity strains are also becoming apparent in the market. Last week, we discussed deteriorating euro basis swap spreads, euro spreads, and 10-year SOFR spreads. U.S. dollar/Japanese yen swap spreads are also showing signs of stress, indicating tighter liquidity. Central banks globally, engaging in quantitative tightening, are straining dealer balance sheets. This pressure is reflected in metrics like the New York Stock Exchange advance-decline line, which has been declining, as well as the equal-weight S&P 500, which isn’t performing well.

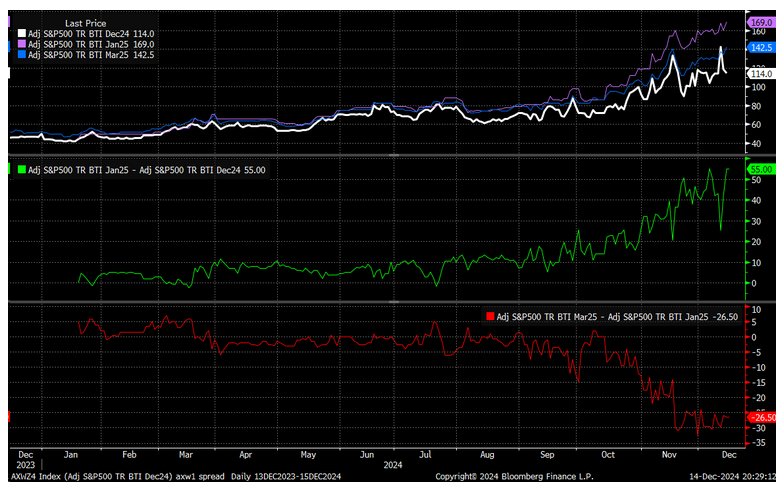

In the S&P 500 total return December futures contracts (BTIC), carrying costs are rising, particularly for January and March contracts, while December contracts have declined. The spread between January and December contracts has widened to 55 basis points, signaling increased carrying costs. Additionally, March contracts are trading 26 basis points below January contracts, which could indicate backwardation and rising liquidity strain.

Cycles are also playing a role in the market narrative. The 10-year Treasury futures are coming out of a 195-week cycle bottom, which took the form of a lengthy consolidation. This suggests the 10-year rate could reach a new high in this cycle, potentially surpassing the 5% peak from October 2023.

A similar cycle is playing out in the dollar index, which appears to be turning upward after a 180-week cycle bottom. The dollar index could rise past its October 2023 highs.

Meanwhile, the S&P 500 is nearing a 180-week cycle peak, which may signal a period of sideways movement or a decline heading into 2025. Historically, these cycles have aligned well with market peaks and troughs, such as in 2000, 2007, and 2021. This suggests we’re heading into a period of stronger dollar, higher rates, and potentially weaker equity markets as we approach 2025.

Originally posted on December 15, 2024 on Mott Capital blog where this article can be read in detail.

PHOTO CREDIT : https://www.shutterstock.com/g/Micin+Lovers

VIA SHUTTERSTOCK

DISCLOSURES

Charts used with the permission of Bloomberg Finance L.P. This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.

{kind=link}