By: Sreeni Meka, Lakeland Wealth Management

What Is the Trade Balance?

Understanding the trade balance involves looking at accounting identities within the balance of payments, which tracks a nation’s international transactions, including exports, imports, investments, and changes in foreign reserves.

National income, mostly expressed as GDP, is created by producing a range of different products (including services): consumption goods (C), government spending (G), investment goods (I), and export goods (X).

GDP=C+I+G+X−M

That income is then spent on either private consumption (C), government consumption (G), or savings (S).

GDP =C+G+S

By combining these equations, we derive:

X−M = S−I

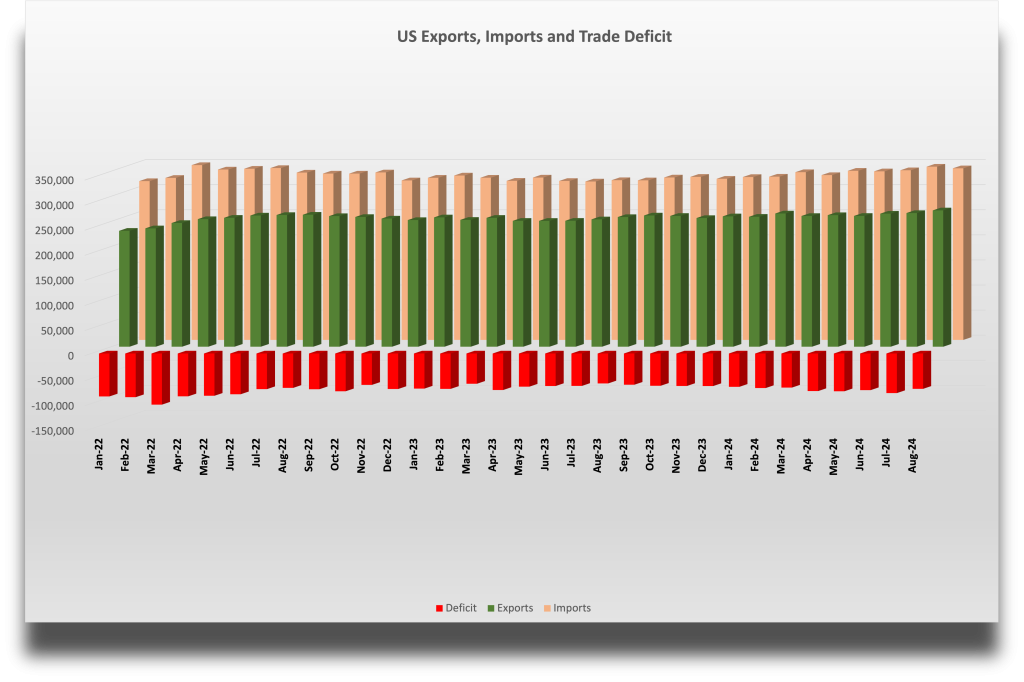

This shows that exports minus imports (the current account) equals savings minus investment (the capital account). This relationship holds for all trading nations.

If domestic savings are insufficient for domestic investment, a country borrows from abroad, indicating foreign confidence in its economy. The U.S., as a net borrower, sees its current account deficit matched by a capital account surplus.

Net capital inflows, such as foreign direct investment, can fund U.S. businesses and potentially create jobs, helping explain why trade deficits don’t always correlate with higher unemployment. Additionally, countries often invest in the U.S. to hold dollars as a reserve currency, which can result in “free” loans, sustaining the U.S. capital account surplus.

Consequently, many economists believe that as long as the dollar remains the world’s primary reserve currency, the U.S. will likely run trade deficits regardless of other economic factors.

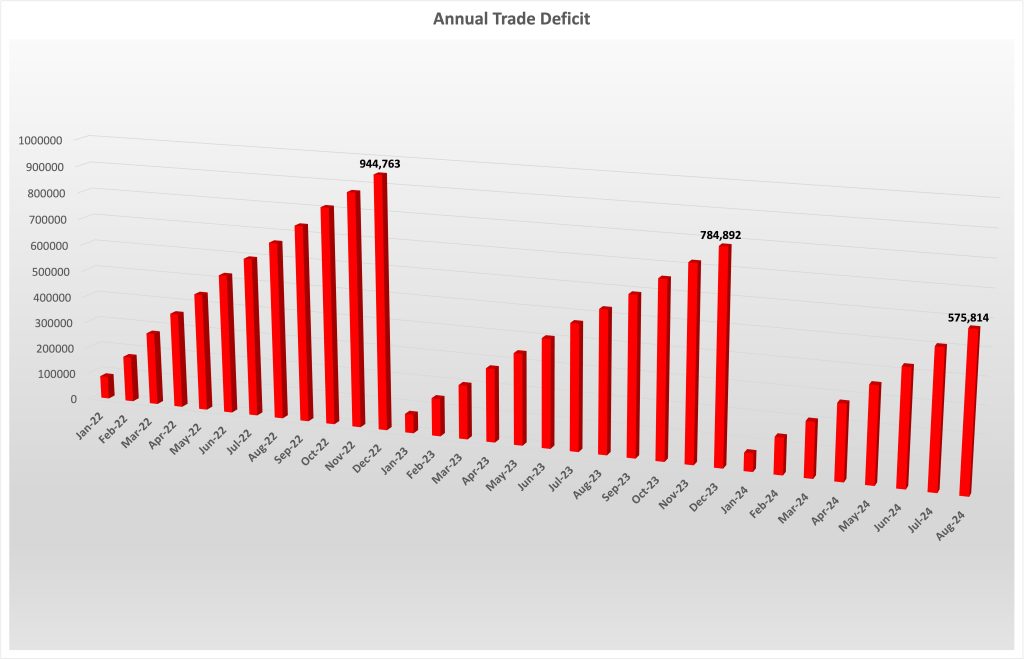

A nation’s trade balance is influenced primarily by its savings and investment levels, not by trade policies like tariffs. A trade deficit occurs when the current account balance (exports – imports) matches the capital account balance (savings – investment). Therefore, any policy aimed at altering the trade deficit must shift the balance between national savings and investment, as these are the core drivers of trade imbalances, rather than trade policies.

Understanding a country’s balance of payments involves viewing it as the sum of its citizens’ international transactions. The deficit isn’t driven by the nation itself but by its citizens and firms engaging in trade and investment abroad. The Treasury’s bond sales to foreign investors are a minor factor in this broader economic picture.

Savings Rate and Trade Balance: US vs. Germany

Individual savings rates vary with age. People save during working years (15–64) and dissave during retirement, while younger individuals rely on others’ savings. Thus, younger populations generally save less.

In the US, a relatively young population saves a smaller income share, and high investment demand creates a savings shortfall, leading to a current account deficit. In contrast, aging Germany saves more and invests abroad, resulting in net capital outflows and a trade surplus. These trade balances reflect economic and demographic differences, not competitiveness or trade practices.

Rethinking Trade Deficits: Germany vs. the United States

Economic theory suggests trade deficits are less problematic than often believed, though not all balance of payments outcomes are ideal. Germany’s trade surplus, for instance, stems from high domestic savings and underinvestment at home rather than aggressive trade policies. The surplus could be reduced by increasing private and public investments.

In contrast, the US has a younger population with lower savings, high business investment, and large federal deficits, all contributing to its trade deficit. The issue isn’t trade practices but low national savings, especially within the government. Therefore, rather than restricting trade, the US should aim to raise its savings rate. In short, the US trade deficit reflects domestic savings and investment choices. Its impact depends on whether the borrowed funds are invested wisely.

PHOTO CREDIT: https://www.shutterstock.com/g/iLixe48

VIA SHUTTERSTOCK

DISCLOSURES

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit nor guarantee against a loss.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.

{kind=link}

{kind=link}