By: Tony Warburton CFA, Ph.D., Head of Active Portfolio Management

The response to the Chinese government’s stimulus package, designed to reinvigorate the economy and drive growth back towards the 5% target, has increased equity market volatility. The ripple effects from these actions as well as market participants’ reactions have been felt far beyond Chinese shores.

China’s Equity Market Stirs

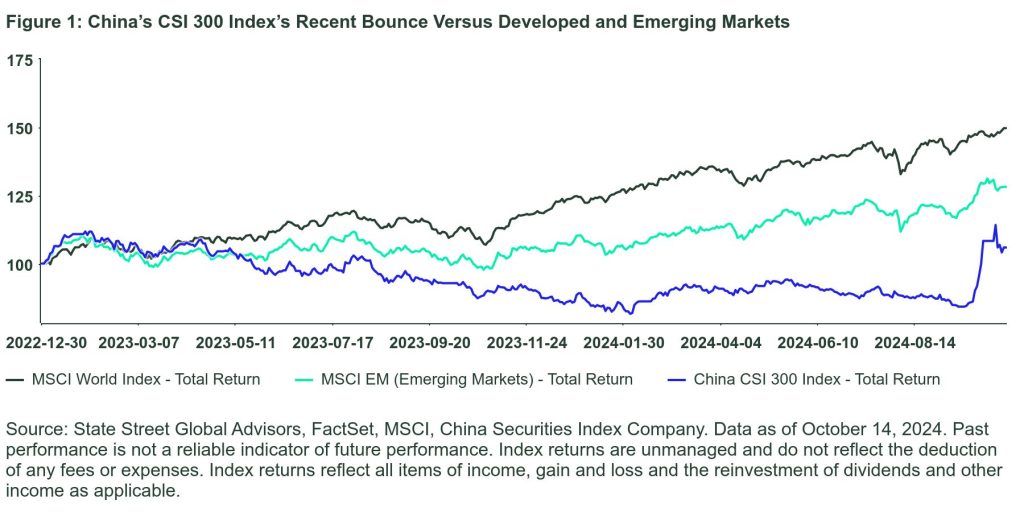

Over the past few years, the Chinese equity market has significantly lagged its counterparts, across both developed and emerging markets. Stimulus measures announced at the end of September resulted in a sizable re-rating of the Chinese equity markets, soon followed by a subsequent dip in early October.

While the jury is out on the economic and corporate effects of the stimulus , equity investors have reacted very quickly to the monetary and fiscal stimulus influx. Time will tell whether the Chinese market continues to rally, or whether investors take a more cautious approach and in turn wait to see how the economic effects of the stimulus flow through to companies and the real economy before continuing China’s re-rating.

This recent price action provides insight into the market exposure of foreign companies to China’s economy and stock market, and how the effect of local policy flows through global channels.

China-Exposed Corporate Performance

To understand the global effect of China stimulus on stocks, we looked to build a measure of China exposure for stocks in the MSCI World Index. A direct way of assessing this exposure is through their reported geographic revenues. We would expect companies with a greater proportion of revenues coming from China to have a higher economic exposure to recent stimulus, on average.

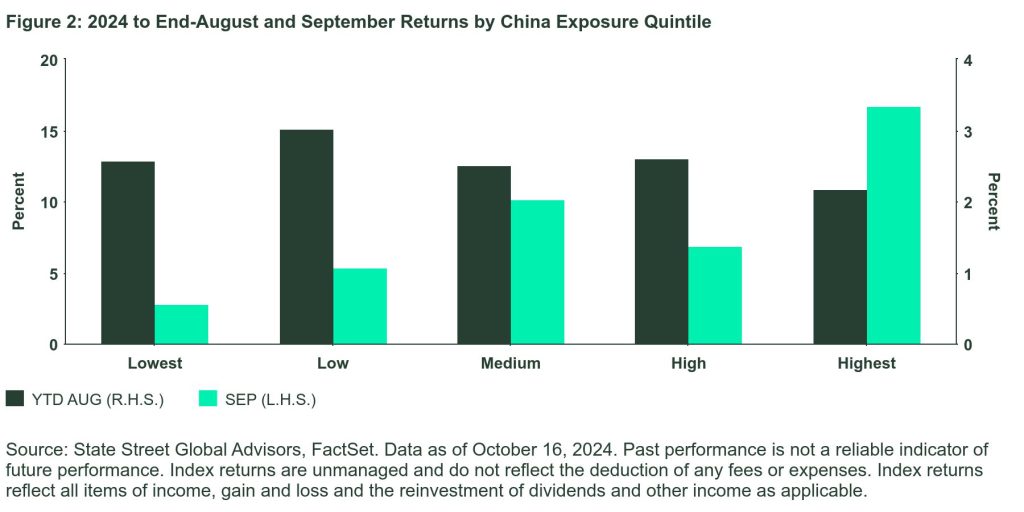

We can also construct a market-based proxy of exposure to the Chinese equity market by calculating the beta of developed market stocks to the CSI 300 Index returns, through the end of August.1 We combined the revenue-based measure with the market-based measure to create a China exposure metric, which enables a more nuanced view into how economic effects in China can propagate through developed markets.

To understand if China exposure is being priced into developed markets, we first bucketed our China exposure metrics into quintiles to enable a look through at average returns over the first eight months of 2024. We reassessed returns again in September, when the Chinese market rebounded suddenly. Notably, the highest quintile of China exposure has underperformed the broader market over 2024 until the end of August, when it then rebounded strongly, outperforming less exposed stocks.

Sector and Geographic Exposure

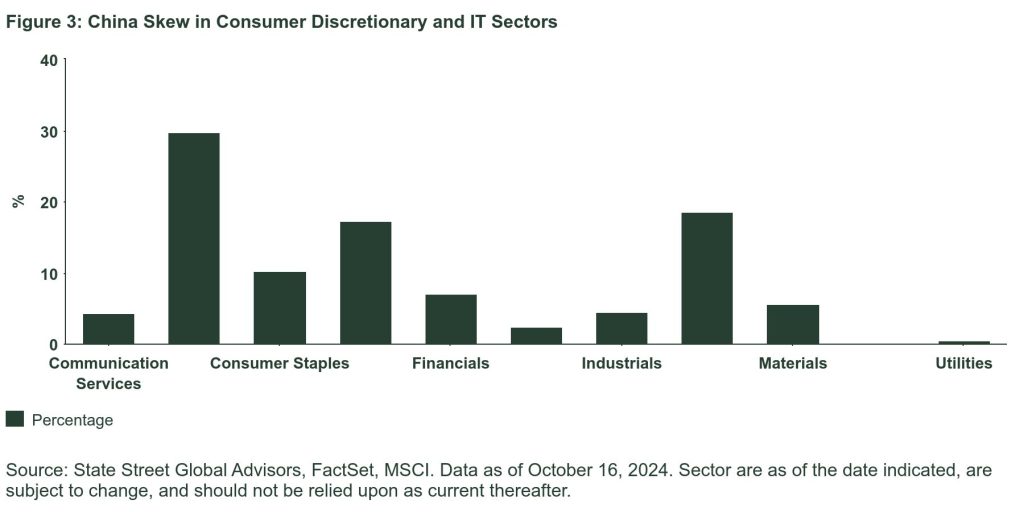

At a sector level, revenue sourced from China is highly skewed and concentrated in Consumer Discretionary (mostly automobiles and components), Information Technology, and Energy sectors. However, on a relative basis, nearly 50% of the revenues for the autos industry group is sourced from the highest quintile of China Exposure, while Energy has no exposure in the highest quintile with revenues more broadly diversified. Within Technology, the exposure is concentrated in a few large manufacturers sitting in the highest quintile of China exposure.

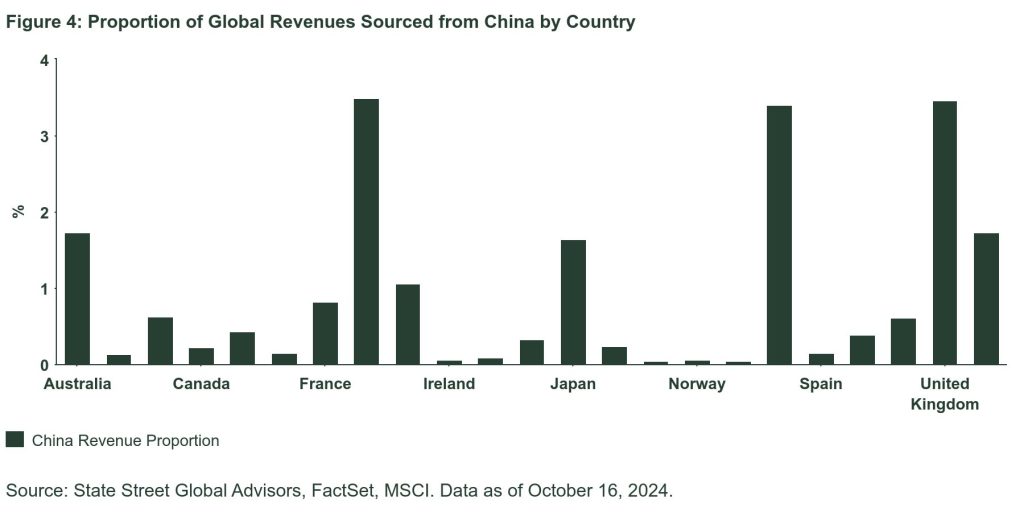

Through a country lens, the most-exposed countries are pockets of Europe, such as Germany through the auto sector, the UK through listed mining companies, and in the geographically proximate Asia-Pacific region. In Singapore, for example, an eclectic mix of Consumer Staples, Real Estate and Financial companies have significant Chinese links.

The Bottom Line

In the interconnected world in which we live, information shocks can ripple through the global economy and impact companies and economies far from an epicenter. The recently-announced Chinese stimulus has reignited animal spirits, not only for the Chinese equity markets, but also for companies and countries that stand to profit from any potential economic benefits.

This transmission mechanism does not only matter for headline-grabbing innovations such as the China stimulus. Our analysis above demonstrates the power of linkages and data flows to drive company returns and equity markets. Our research has shown that information travels more broadly through company supply chains, for example, from customers to suppliers and through companies, with innovation linkages. We explicitly take advantage of these features within our stock returns forecasting models to capture an edge. That information advantage comes from analyzing beyond the headlines and drilling into the nuanced ripples that flow between economies and companies.

Originally posted on October 29, 2024 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/Wlliam+Potter

VIA SHUTTERSTOCK

Footnotes

1 Calculated as the 36-month beta, to the end of August 2024, of returns to the current constituents of the MSCI World Index to the CSI 300 Index returns over the same period.

Disclosures

For use in EMEA: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons, and persons of any other description (including retail clients) should not rely on this communication.

Important Risk Information

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

The views expressed are the views of Systematic Equity – Active through October 17, 2024, and are subject to change based on market and other conditions.

Quantitative investing assumes that future performance of a security relative to other securities may be predicted based on historical economic and financial factors, however, any errors in a model used might not be detected until the fund has sustained a loss or reduced performance related to such errors.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

{kind=link}