By: Brian Manby CFA, Associate (Investment Strategy)

Key Takeaways

- A potential corporate tax cut to 15% under a Trump-led administration could boost U.S. equity index earnings by 5%, with mid-caps and small caps likely benefiting the most due to their higher domestic revenue exposure.

- The Financials and Communication Services sectors, particularly within small caps, stand out as the greatest beneficiaries of tax reductions, while Energy companies may see more muted earnings growth despite their typical alignment with pro-Trump policies.

- With a Republican-controlled Congress likely, fiscal policy catalysts could bolster corporate profits and sustain the equity market rally into 2025, despite concerns of overstretched valuations.

With the U.S. presidential election now in the rearview mirror, global markets are readjusting to reflect the anticipated realities of President-elect Trump’s second term in the Oval Office.

Much like his first victory in 2016, market consensus seems to be that his administration will be characterized by stimulative, pro-growth fiscal policies that equity markets will ultimately celebrate.

Markets received a strong dose of enthusiasm in the aftermath of his resounding victory. U.S. equities, cryptocurrency and the dollar rallied, while banks, the preeminent beneficiary of Trump’s desire for deregulation, enjoyed their best day of relative outperformance versus the S&P 500 Index since the 2020 election. Treasury yields initially climbed higher across the medium-to-long tenors of the curve, no doubt contending with the expected inflationary impulses as a consequence of the stimulative agenda.

However, the Congressional election results will certainly support the business-friendly environment Trump intends to create. Though votes are still being counted as we write, a “red sweep” of both houses of Congress looks increasingly likely and may give the President-elect ample runway to pursue his pro-growth crusade.

A few months ago, when the election outlook was less clear, . At the time, tax rate increases were a flagship policy of Vice President Harris’s campaign and warranted careful consideration for future equity allocations.

Today, those prospects have virtually disappeared, and markets contend with an opposite scenario, yet one they’re familiar with from Trump’s first term: potential cuts to the corporate tax rate.

We update our initial analysis below to reflect the potential equity market benefits should the Trump administration enact a corporate tax rate cut to 15%.

From Congress to Companies’ Bottom Lines

Unsurprisingly, we find that reduced tax rates would provide a meaningful boost to corporate profits with greater incremental benefits moving down the size spectrum.

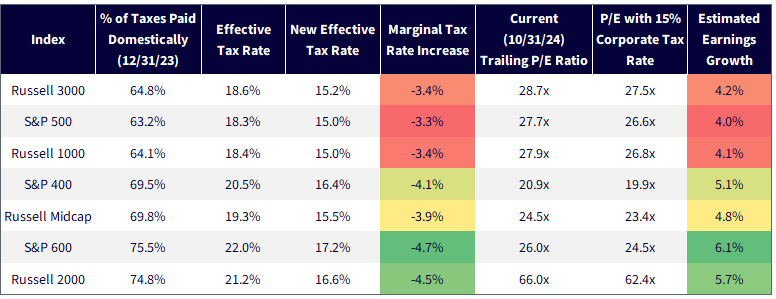

All else being equal, we anticipate that a 15% statutory tax rate (a six-percentage point reduction from the prevailing 21% rate) will result in 3.5%–4.5% effective tax rate reductions and boost equity index earnings by approximately 5%, on average, as shown in figure 1.

Figure 1: Potential Impact of a 15% Corporate Tax Rate

Price-to-earnings (P/E) multiples would contract by one point in large-cap gauges, whose earnings we estimate would grow by about 4% due to a 3% decrease in effective tax rates.

Consistent with our original analysis, mid- and small-cap indexes would exhibit more pronounced effects. These equity segments tend to be more reliant on domestic revenue sources and they consequently pay greater portions of their taxes, overall, to the U.S. government. Correspondingly, a reduction in the corporate tax rate would provide greater relief for these asset classes than it would for large caps, whose geographic revenue sources are more diversified.

We anticipate that mid-caps and small caps would absorb more benefit from slashing the statutory rate, with nearly the entire 5% reduction visible in the change to their effective tax rates. This would potentially boost earnings by 5%–6% and provide a much-needed tailwind for both asset classes.

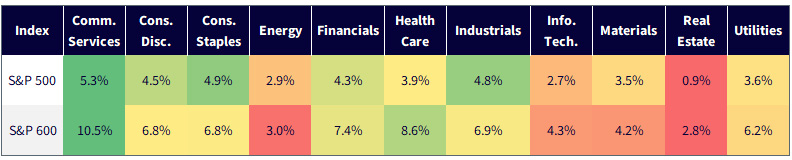

Figure 2 looks at the sector level, where Communication Services continues to be the greatest beneficiary in both large and small caps. Our original analysis modeled that the Communications Services sector would fare the worst under a potential corporate tax rate hike, so it follows that it might benefit the most from a potential reduction. Within small caps, we estimate double-digit potential earnings growth for the sector.

The earnings growth estimate for large-cap Financials is in line with the overall S&P 500 Index, but the pace picks up within the small-cap space. This is consistent with the market’s initial reaction in the aftermath of Trump’s election victory, as the duo of deregulation and tax rate reductions should be a strong tailwind for the beleaguered banking industry.

Energy, however, does not project as favorably in our model, which is ironic considering that Energy companies are typically labeled a “Trump trade” given his affinity to “drill, baby, drill” and dismissal of pro-environmental policy. We estimate the sector’s earnings will only grow about 3% despite a potential tax tailwind.

Figure 2: Estimated Earnings Growth under 15% Corporate Tax Rate

Tax Cuts Could Bolster Earnings amid Valuation Concerns

Though changes to corporate tax policy are never a foregone conclusion, we believe the joint presidential and Congressional election outcomes may create strong catalysts for equities. Fiscal policy proposals within a Trump-friendly Congress could directly flow through to companies’ bottom lines and bolster the corporate earnings environment.

If the Trump administration is successful in enacting a corporate tax rate cut to 15%, it could become the flagship policy of his second term, akin to the 2017 Tax Cuts and Jobs Act (TCJA) from his first.

Although markets may appear overstretched, prompting strategists to call for lower future returns over the near term, a potential corporate tax cut could propel the equity rally further into 2025, while simultaneously condensing above-average multiples from the accompanied earnings boost.

Originally posted on November 15, 2024 on WisdomTree blog

PHOTO CREDIT : https://www.shutterstock.com/g/bj8studio VIA SHUTTERSTOCK

DISCLOSURES:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.