By: Simona M Mocuta, Chief Economist

We answer the three key questions that are top of mind for investors following the latest Fed meeting.

The March Fed meeting was never going to be about March, but about the rest of 2024. Heading into the decision, three questions were top of mind for investors:

- Timing of the first rate cut

- Magnitude of rate cuts for the year

- Timing of tapering of quantitative tightening (QT)

Our Take on the Three Key Investor Questions

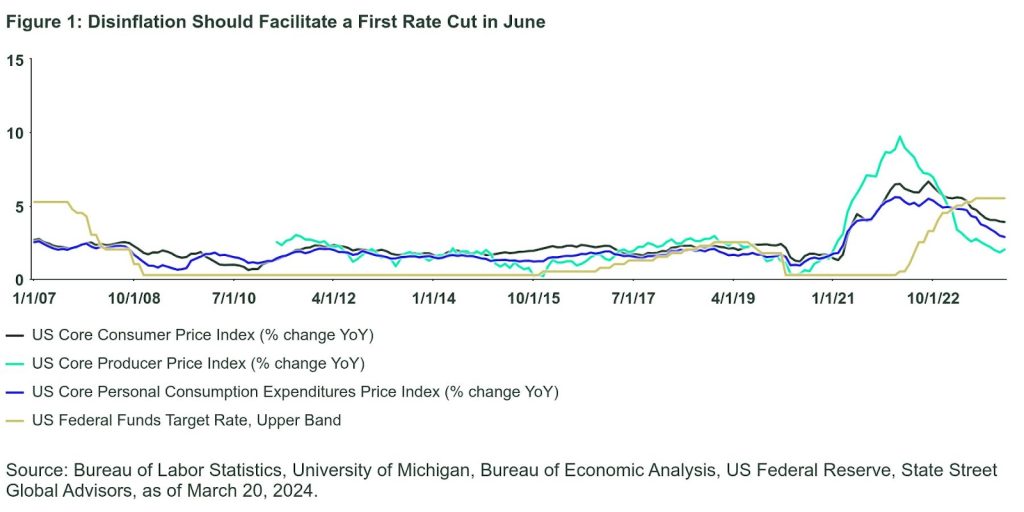

1. Timing of the first rate cut: June continues to be the most likely month to begin the easing cycle (Figure 1). By then, the Federal Open Market Committee (FOMC) will have three more inflation reports and labor market reports in hand – enough for them, in our view, to “gain greater confidence that inflation is moving sustainably toward 2 percent”.

2. Magnitude of rate cuts for the year: The dot plot continues to show three rate cuts this year, the same as in December. However, only three cuts are now expected in 2025 (versus four previously) and the long-run neutral rate was nudged up by a tenth to 2.6%. Given how uncertain the outlook is, neither change is particularly relevant for 2024 policy decisions. We continue to believe that there is room for more cuts this year but especially in 2025.

In fact, if the FOMC does not deliver the 4-5 cuts we expect for 2024, we believe more of them would end up clustered in 2025. The nudge upward in the neutral rate estimate is both minimal and unsurprising and should be taken to reflect a recognition of uncertainties rather than high conviction on the part of the FOMC.

3. Timing of tapering of QT: Regarding balance sheet policy, nothing was officially communicated in the statement, but Fed Chair Jerome Powell mentioned during the press conference that the time to slow balance sheet runoffs could arrive “fairly soon”. Reading between the lines, we would expect a formal announcement at the May meeting.

As pointed out by us before, Chair Powell highlighted the value of “slower for longer” on the balance sheet: by moving more carefully, the Fed can avoid triggering undue stress and needing to end QT before the balance sheet reaches the desired level.

Changes to Economic Forecasts

Finally, there were some changes to economic forecasts, most significantly for 2024. Q4/Q4 GDP growth was revised meaningfully higher—perhaps a touch too much in our view—and core personal consumption expenditures estimate was revised up two tenths to 2.6% YoY.

The latter matches our forecast but does not change our belief that, despite not being at target just yet, the Fed can afford to ease more, especially since we see upside risks to the Fed unemployment rate forecast.

Originally Posted March 21st, 2024, on State Street Global Advisors’ blog

PHOTO CREDIT: https://www.shutterstock.com/g/pabrady63

Via SHUTTERSTOCK

Disclosure

Marketing Communication

State Street Global Advisors Worldwide Entities

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

The views expressed in this material are the views of Simona Mocuta through the period ended 20 March 2024 and are subject to change based on market and other conditions.

This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Past performance is not a reliable indicator of future performance.

Investing involves risk including the risk of loss of principal.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

{kind=link}

{kind=link}