By: Christopher Gannatti, CFA, Global Head of Research and Mobeen Tahir, Associate Director, Research

Key Takeaways

- Investor sentiment in commodity markets has reached a five-year low, presenting potential opportunities for contrarian investors.

- Potential opportunities and challenges exist in industrial metals, energy, precious metals and agricultural commodities.

- Despite current bearishness, structural tailwinds like the global energy transition and geopolitical tensions could lead to a rebound in commodity prices.

Investor sentiment in commodity markets appears to have reached an extreme level of bearishness, with net speculative positioning on commodity futures at its lowest point in five years.1 This pessimistic stance has been shaped by several factors, including recent market volatility and ongoing economic concerns. However, this level of bearishness may be overstated, creating potential opportunities for contrarian investors, both tactically and strategically. In this blog post, we’ll explore the main subsectors of the commodities market—industrial metals, energy, precious metals and agricultural commodities—to assess whether this is an inflection point and what might come next.

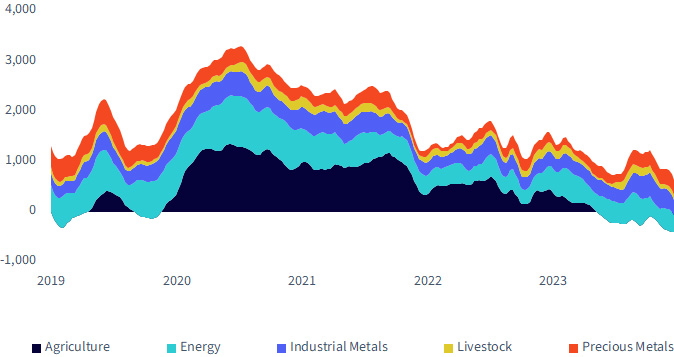

Figure 1: Net Speculative Positioning in Commodity Futures

Source: WisdomTree, Commodity Futures Trading Commission (CFTC), Bloomberg. Latest CFTC positioning data as of 8/6/24.

Industrial Metals: Overlooked Structural Tailwinds

Industrial metals have faced significant headwinds recently, driven largely by weak sentiment toward China. Concerns about that country’s economic slowdown, particularly in manufacturing, have weighed heavily on the sector. Additionally, the global trend of higher interest rates has further dampened sentiment toward industrial metals, as higher borrowing costs slow down investment in infrastructure and manufacturing. Another factor contributing to the bearish sentiment is the perception of ample supply in the short term, with rising inventories on exchanges suggesting that physical supplies are abundant.

Despite these challenges, there are strong structural tailwinds that the market seems to be overlooking. The global push toward energy transition and decarbonization will require a massive increase in the production of industrial metals like copper, nickel and aluminum. As the world ramps up investment in renewable energy, electric vehicles and battery storage, demand for these metals is expected to rise significantly. This long-term narrative is not currently priced into the market, making industrial metals an attractive opportunity for investors who are willing to look beyond the short-term noise. The current bearish positioning could thus set the stage for a significant rebound as the energy transition narrative gains traction.

Energy: A Tactical Buying Opportunity amid Volatility

The energy sector, particularly oil markets, has been characterized by significant volatility in recent months. Oil prices have fluctuated broadly within a range of $70–$90 per barrel, influenced by a complex mix of factors. Concerns about an impending recession in the U.S. led to a sharp decline in prices in July and early August. However, this was followed by a rebound in mid-August as equity markets recovered and geopolitical tensions in the Middle East resurfaced.

Despite these fluctuations, the International Energy Agency expects demand growth to be just under 1 million barrels per day (mb/d) in both 2024 and 2025, considerably below last year’s 2.1mb/d growth, but not necessarily alarming.2 The current low level of speculative positioning in energy markets, exacerbated by recent volatility, suggests that investors may be overly pessimistic. For contrarian investors, this could represent a tactical buying opportunity, particularly as oil prices recently approached the lower end of their trading range before rebounding. If supply struggles to keep pace with demand, especially during peak periods, we could see another upward shift in prices, potentially catching the bears off guard.

Precious Metals: A Steady Performer with Upside Potential

Unlike other commodity sectors, net speculative positioning in precious metals has remained relatively stable, hovering around its five-year average. Gold has shown resilience, supported by strong central bank buying, most notably by the People’s Bank of China (PBOC).3 This demand has helped gold maintain its strength despite headwinds from delayed rate cuts, which have put upward pressure on Treasury yields and strengthened the U.S. dollar—both typically negative factors for gold.

Looking ahead, several factors could further boost gold’s appeal. As the Federal Reserve eventually shifts to cutting interest rates, geopolitical tensions persist and uncertainties around global trade continue, demand for gold is likely to increase. Moreover, if investors in exchange-traded products, who have not fully participated in the recent rally, begin to increase their exposure to gold, we could see additional upward momentum in the sector. For investors seeking a hedge against economic and geopolitical risks, gold remains a compelling option.

Agricultural Commodities: Undervalued and Underestimated

Among all the commodity subsectors, agricultural commodities have seen the steepest decline in net speculative positioning, reaching their lowest level in five years. In recent years, agricultural commodities have often experienced strong rallies due to various disruptive events, including the Covid-19 pandemic, the Russia-Ukraine conflict, and extreme weather patterns like El Niño and La Niña. These events have led to significant physical disruptions in supply chains, contributing to supply shortages in agricultural markets.

The current extreme low in positioning suggests that the market may be underestimating potential risks on the horizon. Agricultural commodities are particularly vulnerable to sudden disruptions, whether due to geopolitical events, climate change, or unexpected shifts in supply and demand dynamics. With the market seemingly disregarding these risks, there could be a sharp reversal in sentiment if any of these potential disruptions materialize. For investors, the current bearish positioning in agricultural commodities may present a unique opportunity to capitalize on an underappreciated sector.

WisdomTree’s Approach to Broad-Based Commodity Exposure

In thinking about portfolio construction, the equity and fixed income asset classes tend to get the majority of our attention. Commodities, however, can provide a differentiated return profile.

One catalyst for commodity returns can be rising expectations of inflation, something that did impact commodity returns during 2022. At a time when broad-based equity markets were negative and fixed income saw interest rates rising, commodities were able to provide a differentiated return profile.

Another consideration for commodities regards how they are priced in U.S. dollars. Those seeing a chance for U.S. dollar strength shifting toward U.S. dollar weakness may look to commodities, as a weaker U.S. dollar could translate to rising commodity prices.

The WisdomTree Enhanced Commodity Strategy Fund (GCC) is an actively managed exchange-traded Fund and intends to provide broad-based exposure to the following four commodity sectors: energy, agriculture, industrial metals and precious metals, primarily through investments in futures contracts. The Fund may also invest up to 10% of its net assets in any combination of shares of one or more exchange-traded products that primarily hold bitcoin and in bitcoin futures contracts. The Fund will not invest in bitcoin directly.

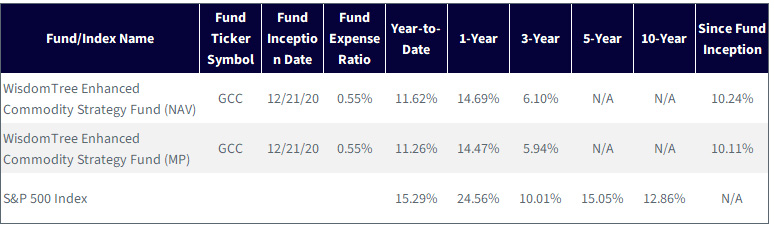

The following figures will give some perspective on GCC’s performance.

Figure 2a: Standardized Returns

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 6/30/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Prior to 12/21/20, the ticker symbol GCC was used for an exchange-traded

commodity pool trading under a different name and strategy. Past performance is not indicative of future results. Investment return and

principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their

original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and

standardized performance and to download the Fund prospectus, click here.

Figure 2b shows the year-to-date performance of GCC, shown with the S&P 500 Index for context. It was notable how GCC saw an acceleration of returns, roughly in April and May 2024, while the S&P 500 Index tended to drop lower. More recently, during the downdraft of performance in early August 2024, both GCC and the S&P 500 Index were impacted.

Figure 2b: Year-to-Date Returns for 2024

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 8/15/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment

return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less

than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-

end and standardized performance and to download the Fund prospectus, click here.

Figure 2c takes us back three years, to August 14, 2021. The transition from 2021 to 2022 was an important turning point in markets, as we started to see the inflationary consequences of all the stimulative monetary and fiscal policy during the Covid-19 pandemic. While the S&P 500 Index trended more in the downward direction, GCC moved sharply upward in early 2022. This was also the time of Russia’s invasion of Ukraine, which did create supply-side concerns and rising prices across an array of commodities, especially energy.

GCC did not necessarily keep pace as the S&P 500 Index recovered, but, from a portfolio construction perspective, 2022 did provide a notable proof-point of its differentiated return potential.

Figure 2c: 3-Year Returns Perspective

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 8/15/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment

return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less

than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-

end and standardized performance and to download the Fund prospectus, click here.

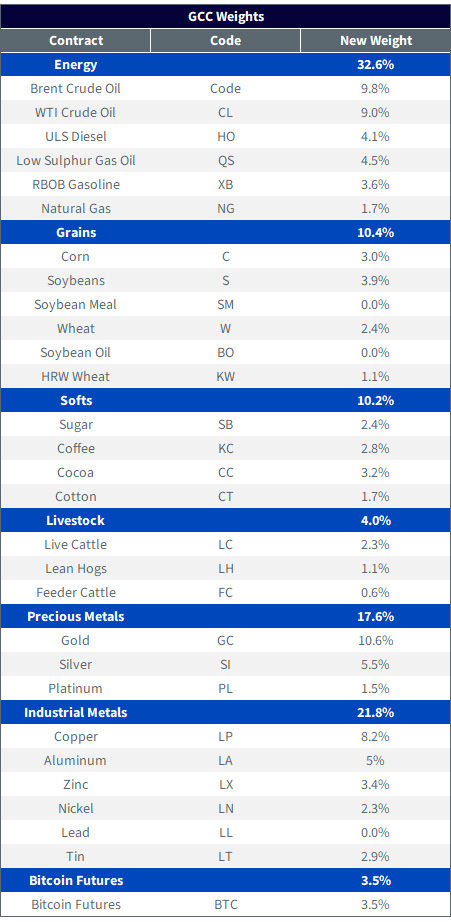

With any commodity strategy, one of the most important aspects is looking under the hood at the actual exposure. Some strategies have more weight in energy, while others attempt to be more evenly distributed. It’s critical to evaluate how the exposure looks relative to one’s economic expectations. Figure 3 indicates GCC’s breakdown across different commodity

exposures.

Figure 3: GCC’s Commodity Breakdown

Source: WisdomTree. GCC weights as of 6/30/24. As we rebalance the strategy, actual

weights on any business day may vary from rebalance weights due to market price

fluctuations. Contract refers to any listed commodity futures contract. Commodity

refers to basic good used in commerce, often inputs in the production of other goods

or service. The difference between commodity and contract is illustrated through this

example: the Crude Oil commodity is invested in through two different contracts: the

WTI Crude (NYMEX) and the Brent Crude (ICE) contracts.

Conclusion

While commodities have experienced a wave of bearish sentiment, reflected in the lowest net speculative positioning in five years, this extreme pessimism may be overdone. Each subsector—industrial metals, energy, precious metals and agricultural commodities—presents unique opportunities that could lead to an inflection point in the market. As history has shown, periods of extreme bearishness can sometimes precede significant rebounds, and contrarian investors may find attractive entry points in the current market environment. Whether this marks the start of another commodity supercycle or simply a cyclical upturn remains to be seen, but the potential for a shift in sentiment is certainly worth considering.

This post first appeared on August 28, 2024 on the WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/lightspring

Via SHUTTERSTOCK

1 Sources: WisdomTree, Commodity Futures Trading Commission, Bloomberg, as of 8/6/24.

2 IEA, Oil Market Report – August 2024, iea.org. https://www.iea.org/reports/oil-market-report-august-2024

3 Joseph Moss, “What’s behind China’s Gold-Buying Spree?” International Banker, 8/14/24. https://internationalbanker.com/banking/whats-behind-chinas-gold-buying-spree/

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.