By: Simona M Mocuta, Chief Economist

In 2023, we described the US housing sector as being in recession but—unlike in 2009—not in “crisis.” At the start of 2024, we can already say that the housing recession— a period marked both by a collapse in home purchases and declining housing construction—is over: a nascent recovery is now underway. The housing sector should support the economy this year as lower interest rates allow pent-up demand to manifest again.

We are hopeful that this rebound will not cause inflation because lower rates will also unlock previously frozen supply (especially in the existing home segment). As housing-related spending picks up, parts of discretionary consumer spending like leisure and hospitality may see demand soften.

Housing Supports the Soft Landing Narrative

Housing is probably the most interest rate-sensitive sector in the US economy. As the Federal Reserve embarked on an aggressive tightening cycle in 2022, residential construction took a genuine nosedive. These declines were similar in intensity to what was experienced during the Great Financial Crisis (GFC), but were far shorter in duration. This reflects vastly different market dynamics. Leading into the GFC, there was a housing oversupply and a proliferation of poor lending standards. By contrast, following years of corrective under-investment post-GFC, the US housing sector entered the pandemic with a supply deficit. The only reason the recession even occurred was that surging mortgage costs crashed affordability and pushed potential buyers temporarily to the sidelines.

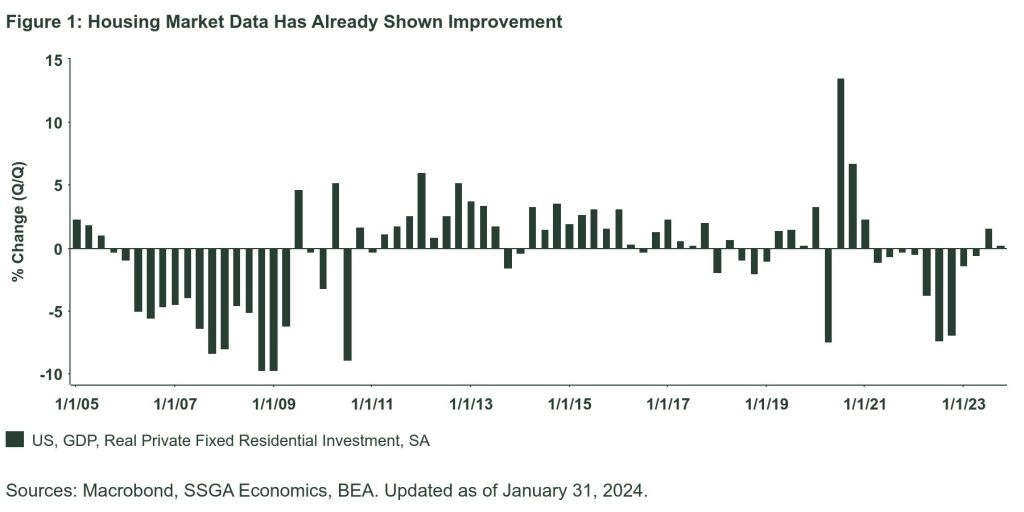

With rates coming back down, pent-up demand can materialize once again. We look for modest growth in residential investment in 2024. The improvement is already visible in Figure 1, with residential investment turning positive in recent quarters. Also, housing starts were up 7.6% y/y in December—the best yearly comparison since April 2022. Additionally, homebuilder sentiment jumped in January, with future sales expectations up by the most since June 2020.

Wouldn’t a Housing Rebound Prove Inflationary?

We think there are good reasons to believe it will not.

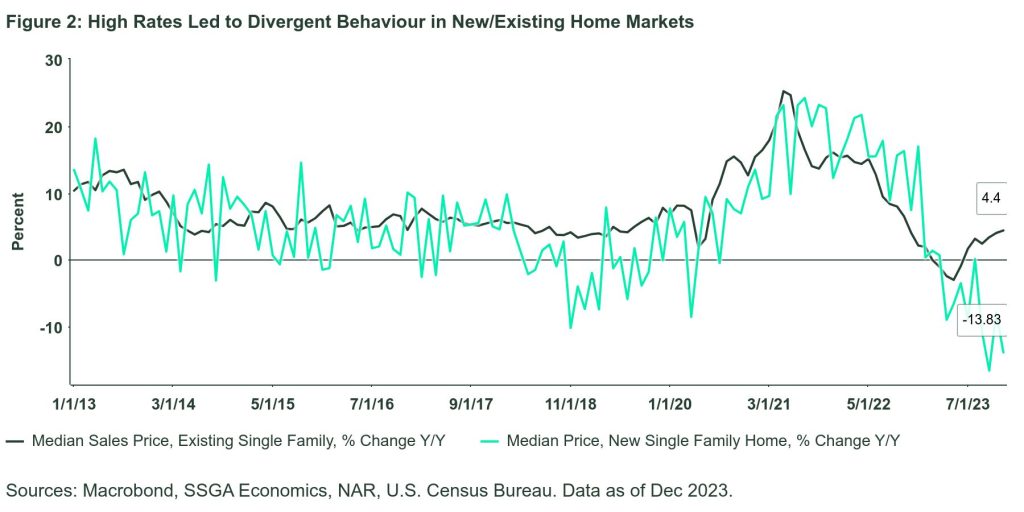

New Supply in the Wings. Normally, new and existing home prices move in tandem. But in 2023, new home prices corrected sharply lower while existing home prices barely declined. Rising mortgage rates became a major disincentive for homeowners to list their homes, as doing so would have implied swapping a low (possibly sub-3.0%) mortgage rate for a much higher (6.0%+) one. Due to the scarcity of inventory, the few existing properties made available for sale still managed to command elevated prices. By contrast, the median new home price was down 16.5% y/y in October 2023 and 12.7% y/y in Q4 2023 as a whole (Figure 2).

These dynamics should reverse over the course of 2024 as the Fed eases rates and Treasury yields pull back further in anticipation, lowering mortgage rates. While there is pent-up demand for homes, there is also some pent-up supply in the existing home space. On balance, the combination should limit the potential inflationary impulse.

Changing Homebuyer Frame of Mind. Buyer behavior is also changing. In December 2023, 16% of homes sold above asking price, down from 35% in July 2023 and a peak of 61% in April 2022. Even as mortgage rates come down, buyers should be less eager to bid up prices given depleting excess savings and more uncertainty around the employment outlook. Patience replaces euphoria.

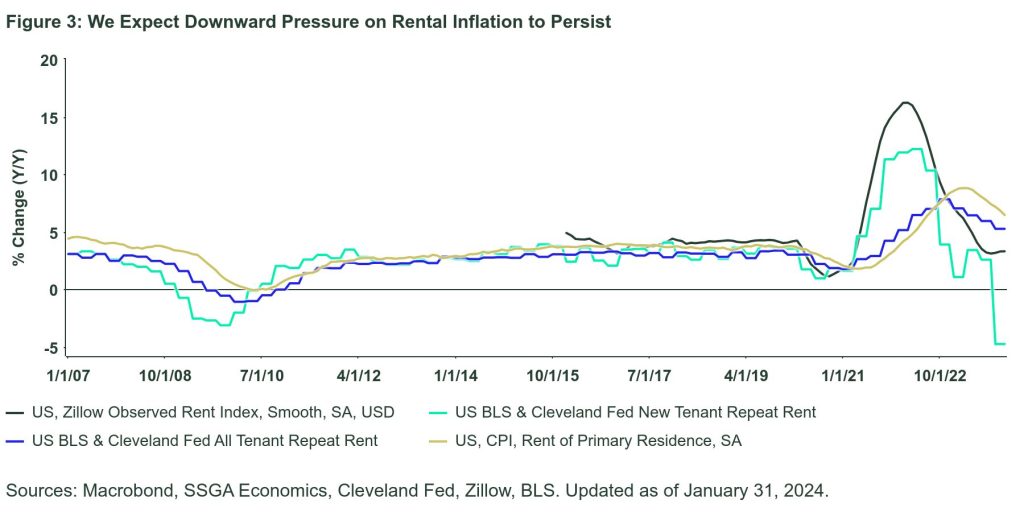

Hefty New Rental Supply. The other factor that can limit house price appreciation is that considerable new rental supply came onto the market in the multi-family space last year, offering an alternative. More will arrive in 2024. This message came out loud and clear in the Zillow Observed Rent Index (ZORI) data, and even more starkly, in the BLS/Cleveland Fed new tenant repeat rent index. The latter collapsed in Q4 2023 to levels not seen since the GFC (Figure 3). Even if the drop moderates going forward (which is likely), it still signals pipeline disinflation in rents that should cap house price appreciation.

Winners and Losers from a Recovery in Housing

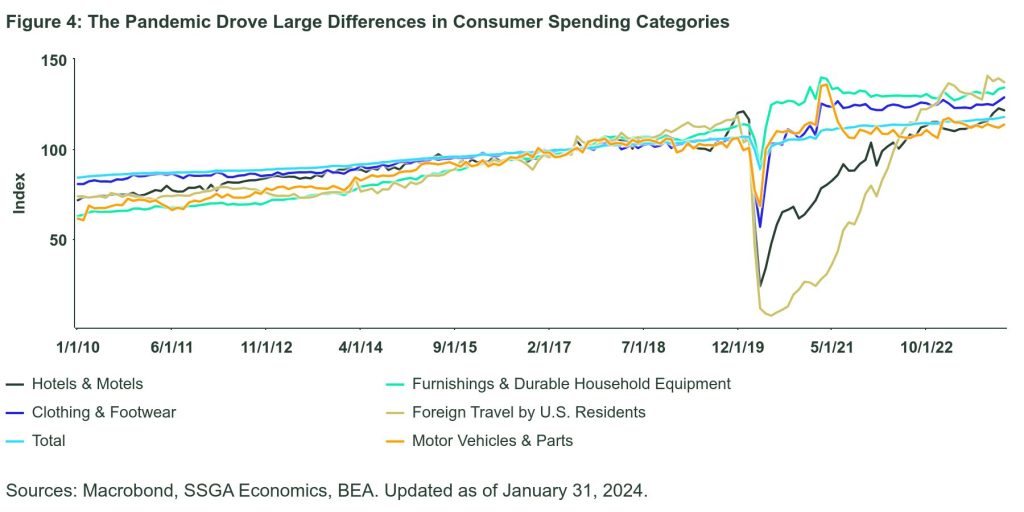

Despite a recession in housing and weakness in manufacturing, the US economy outperformed growth expectations in 2023 thanks to robust consumer spending. Will a housing rebound impact consumption in 2024, and how? It is unlikely that a bounceback in housing would meaningfully alter the pace of aggregate consumer spending since that performance is primarily driven by income growth, specifically labor income. However, the composition of consumption may shift at the margin. Different buckets of consumer spending have exhibited vastly different patterns during the pandemic, with areas like foreign travel and clothing far above pre-Covid levels. By contrast, spending on motor vehicles remains constrained by inventory limitations (Figure 4).

As supply limitations in the auto industry fade, and as the housing market strengthens, consumer demand may shift away from certain discretionary spending categories that have previously outperformed.

The Bottom Line

Easier Fed policy should support a resurgence of housing demand—a trend that is already in progress. We believe that a range of factors will mute the inflationary pressures that could come along with this rebound. The impact on consumer spending is likely to be modest overall and mixed in regards to industry segments.

This post first appeared on February 12th, 2024 on State Street Global Advisors’ blog

PHOTO CREDIT: https://www.shutterstock.com/g/k_nopparat

Via SHUTTERSTOCK

Disclosure

Marketing Communication

Important Risk Information

State Street Global Advisors Worldwide Entities

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

The views expressed in this material are the views of the Global Macroeconomics team through February 5, 2024, and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Past performance is not a guarantee of future results. Investing involves risk including the risk of loss of principal.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

For EMEA Distribution: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

© 2024 State Street Corporation – All rights reserved.

{kind=link}