By Pierre Debru Head of Quantitative Research & Multi Asset Solutions at WisdomTree in Europe

Building a house on weak foundations is a recipe for disaster. This is also true for equity portfolios. While core holdings may not be the most exciting, a portfolio’s success will often hinge on their quality. Investors should look for four main characteristics in an asset they choose for the core of a portfolio:

- Reliable outperformance over the long term, anchored in known and proven investment principles

- Resilient behavior across the business cycle

- Defensiveness in crises

- Asymmetric risk profile, i.e., capturing more of the upside than the downside

Highly profitable companies are often regarded as great core holdings, since they easily tick all four of the boxes above. At WisdomTree, we believe that a high-quality strategy is the cornerstone of an equity portfolio. It is the key to building resilient portfolios that can help investors build wealth over the long term and weather the inevitable storms along the way.

Reliable Outperformance with the Quality Factor

Among practitioners, selecting stocks based on their quality attributes has a long track record. Warren Buffett does not stand alone in his focus on high-quality stocks. His mentor, Benjamin Graham, a founding father of value investing, recognized the value of high-quality companies as early as 1934 (Graham and Dodd 1934).

More recently, academics have also recognized the long-term outperformance of quality stocks. In 2014, Fama and French extended their three-factors model (market, size and value) to a five-factors model that includes two quality factors.1

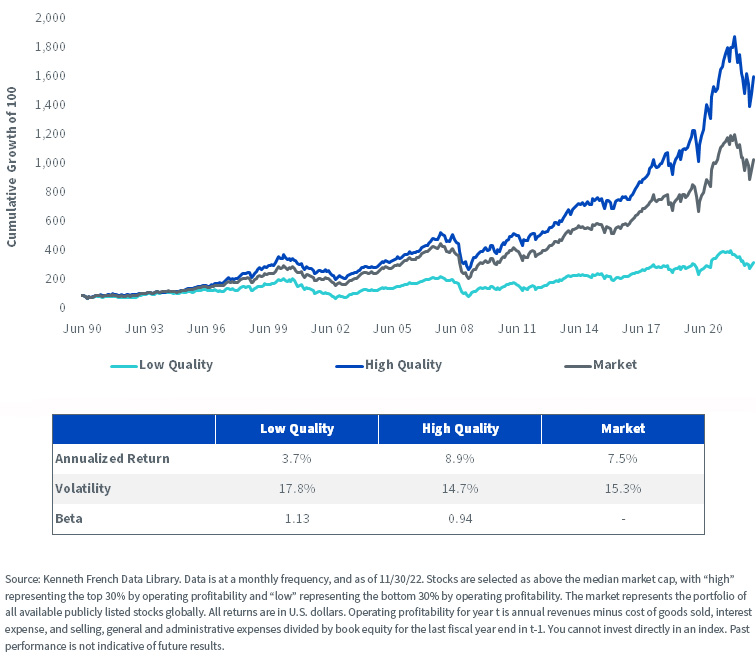

Figure 1: High-Quality Stocks Historically Outperform the Market with Less Volatility

In figure 1, the high-quality portfolio, which includes the 30% of stocks with the highest operating profitability in the global developed equities universe, outperforms the low-quality portfolio (which includes the 30% of stocks with the lowest operating profitability) by more than 4.5% per year since 1990. The high-quality portfolio also outperforms the market by 1.4% per year while delivering lower volatility, demonstrating its credentials as a recognized equity factor.

Historically, quality stocks have exhibited higher long-term returns and lower volatility, which creates a very attractive risk-return profile for core holdings in investors’ portfolios.

Steady as Quality Goes

Quality stocks benefit from strong business models and steady financial results over time. Their financial performance is, therefore, more consistent and predictable from one period to the next. When building investment strategies focused on quality stocks, this translates into steady, robust returns in a large array of market scenarios. When compared with other equity factors, the quality factor tends to deliver more consistent periods of outperformance.

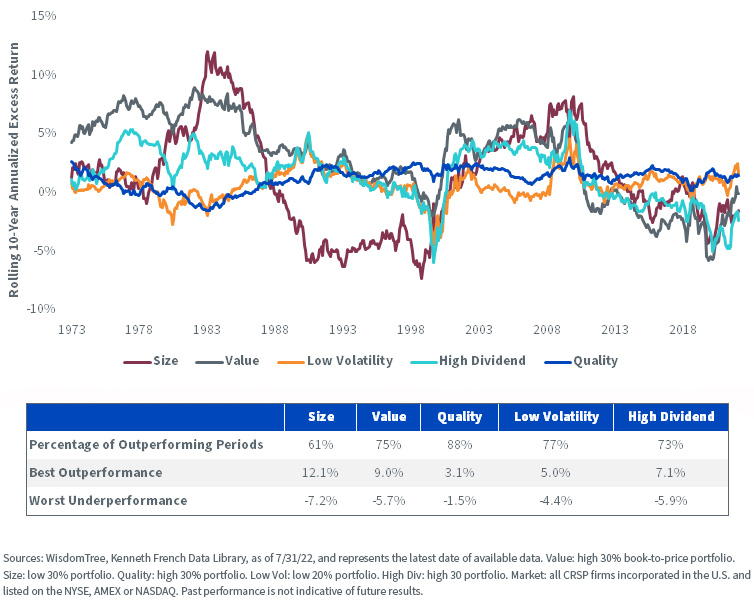

Figure 2: Rolling 10-Y Annualized Performance of U.S. Factors versus U.S. Equities as a Whole

In figure 2, we show the rolling outperformance of different equity factors relative to the U.S. equity markets over periods of 10 years. We observe that size outperforms 61% of the period . In other words, an investor holding a small-cap investment for 10 years (at any point between 1960 and 2022) would have had six chances out of 10 to outperform. Other factors exhibit outperformance around 70% of the time. Quality stands out with a historical occurrence of outperformance of 88%.

While the quality factor in many years may feel more like the Tortoise than the Hare, let’s not forget La Fontaine’s old adage “slow and steady wins the race.”

Weathering Uncertainty and Market Drawdowns by Focusing on Highly Profitable Stocks

When investing strategically in equities, investors should look for strategies that can weather unexpected and unpredictable events. Core holdings need to be able to withstand drawdowns as they do not have a vocation to be traded in and out of the portfolio at every sign of trouble.

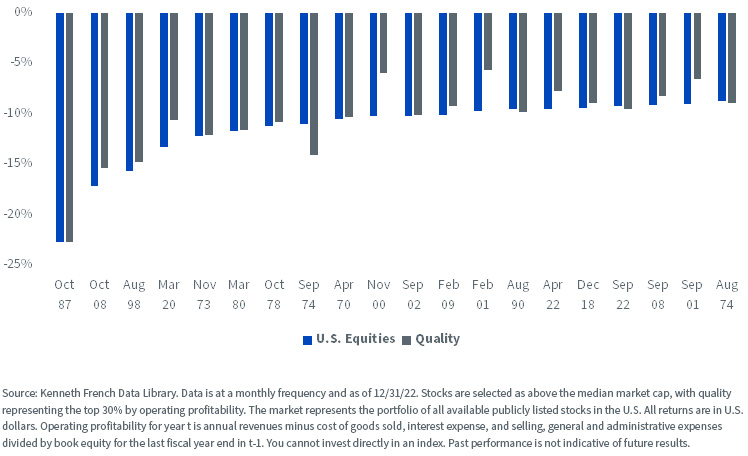

Quality is not the only defensive factor, of course. It is not, in fact, the most defensive factor, a mantel that min volatility claims easily. It is a defensive factor nonetheless, and it has demonstrated time and time again that it can protect investors’ portfolios when equity markets turn south. Looking at the last 60 years, we can see that in 12 out of the 15 worst months in U.S. equities, the quality factor cushioned the drop and lowered the drawdown. In April 2022, for example, U.S. equities lost 9.45% while the quality factor lost only 7.73%, an improvement of 1.72%. Or, in March 2020, U.S. equities lost 13.26% while the quality factor lost only 10.62%, an improvement of 2.64%.

Figure 3: Performance of the Quality Factors in the Worst 15 Months for U.S. Equities since 1963

This is also the case over longer time periods. During the Covid crisis (i.e., between February and March 2020), the S&P 500 lost 29% while quality lost 25.75%, cushioning the blow by 3.3%. In 2022, it reduced it by 12%.2

Overall, the quality factor delivers outperformance in most crises, providing well-needed respite to investors when they need it the most. However, contrary to other defensive factors, the quality factor can also participate in the upside, making it an ideal candidate for long-term investments.

The All-Weather Factor

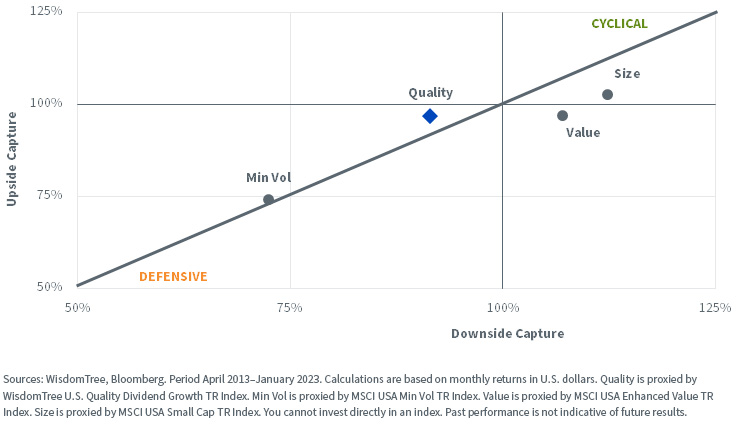

Over the long term, the key to a successful investment is to capture more of the upside than of the downside. A strategy that demonstrates such an asymmetric profile will thrive over the long run. Figure 4 shows the upside capture and downside capture ratio of the quality factor relative to other strategies, calculated on monthly returns. The upside capture ratio is the percentage of market gain captured by a strategy when markets go up, and the downside capture ratio is similarly the percentage of market losses endured by a strategy when markets go down.

Figure 4: Upside and Downside Capture Ratio of Various Equity Factors and Peers

Strategies that sit above the gray line have a strong advantage over the ones sitting below the line. Their upside capture ratio is bigger than their downside capture ratio, which means that they capture more of the upside when the market is up than they lose when the market is down.

Quality is the strategy furthest above the line. So, it benefits from having a very asymmetric profile with an upside capture ratio of 97% and a downside capture ratio of only 91%. In other words, it is a factor that can both grow and defend.

Looking at our list of four characteristics, quality investments tick all the boxes. Anchored in academic research, quality strategies have the strength to grow over the long term and also to weather any temporary storm. This makes quality an ideal candidate for a strategic, long-term, core investment in equities.

Originally Posted March 17th, 2023 WisdomTree

PHOTO CREDIT: https://www.shutterstock.com/g/captureandcompose

Via SHUTTERSTOCK

1 (Fama and French, A Five-Factor Asset Pricing Model 2014)

2 Sources: WisdomTree, Bloomberg. Periods 2/19/20–3/18/20 and 12/31/21–12/31/22. Calculations are in U.S. dollars. Quality is proxied by the WisdomTree U.S. Quality Dividend Growth TR Index. You cannot invest in an index. Above numbers include back tested data. Past performance is not indicative of future results.

Pierre Debru is an employee of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management Inc.’s parent company, WisdomTree Investments, Inc.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}