By: Jose Torres, Interactive Brokers’ Senior Economist

Central banks’ efforts to curtail persistent price gains while achieving an economic soft landing were dealt a major blow this morning by OPEC +’s newest actions that are causing oil prices to soar at a time when the ISM Purchasing Managers Index has hit a new cycle low of 46.3. The oil price shock and the ISM data collectively reflect powerful forces supporting higher inflation amidst deteriorating economic growth.

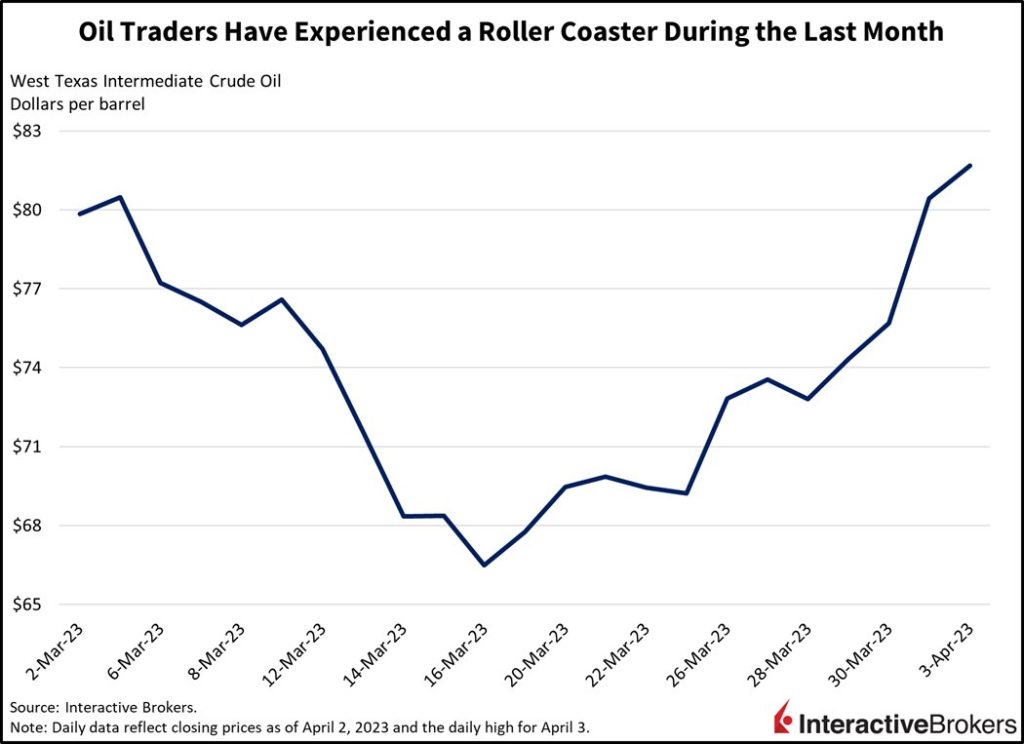

After bouncing along 15-month lows of approximately $70 a barrel for West Texas Intermediate Crude last month and even falling briefly to $65, oil prices jumped to $81.69, a whopping 8% daily gain, after OPEC + announced additional production cuts this weekend. Moreover, energy analysts forecast that oil prices could climb to above $95 a barrel. The cuts involve OPEC + members such as Saudi Arabia, Kuwait, Algeria, and Iraq reducing production by 600,000 barrels a day. This follows an OPEC + decision in October to cut production by 2 million barrels a day, or about 2% of global demand, and occur as Russia’s energy exports have been throttled by sanctions targeting the country in response to its invasion of Ukraine.

The OPEC + announcements sent shares of U.S. oil producers soaring this morning on expectations that higher petroleum prices will boost energy companies’ profits. From a longer-term perspective, higher oil prices make oil fracking in the U.S. more competitive in global markets. The OPEC + announcement, therefore, could lead to an increase in domestic energy production that offsets production shortfalls.

While the announcement may be good news to U.S. energy companies and their shareholders, it is creating another challenge for central banks that are seeking to stymie price increase without sparking recessions. In the U.S., for example, Federal Reserve bank leaders forecast an anemic 0.4% 2023 real GDP growth rate, according to the March Summary of Economic Projections. That was a decline from the 0.5% forecasted in the December summary. Fed leaders in March also forecasted core PCE of 3.6% for this year, up from the 3.5% forecast in December.

While the core PCE excludes oil and food prices, it isn’t immune from the impact of higher energy costs. For example, higher diesel may cause freight fees to increase for goods producers, who may then pass the higher costs on to consumers by increasing their prices. Service providers may also increase their prices in response to higher transportation costs. The inflationary impact of higher energy costs can also tip the economy closer to a recession as consumers may cut back on spending when facing pain at the gasoline pump, which is making the Fed’s efforts of tightening monetary policy to fight price increases without sending the economy into a downward spiral more difficult. For decades, low, disinflationary commodity prices helped the Fed maintain relatively low policy rates.

Manufacturing Weakens Further

This morning’s ISM’s report on manufacturing reached a new cycle low of 46.3, battering expectations of a modest decline to 47.3 from February’s 47.5 level. The new orders and employment segments weighed on the headline number, coming in deeply negative at 44.3 and 46.9, an accelerated contraction from the previous period’s 47 and 49.1 levels. Supplier deliveries are speeding up while work backlogs are slowing as manufacturers trim labor against the backdrop of order books that face pressure. As manufacturers fulfill backorders and experience a decline in new orders, they are scrutinizing their production capacity as they look ahead to the risks of a potential recession.

Markets Rotate Out of Growth

The one-two punch of higher inflation and rising recession prospects is punishing the growthier areas of the market while cyclicals are faring better. The NASDAQ index is down almost 1%, the Dow Index is up 0.7% and the S&P 500 Index is roughly flat. Yields are down across durations as bond traders place more emphasis on recession risk rather than inflation prospects. The two and 10-year Treasury yields are down roughly seven basis points (bps) to 3.99% and 3.43%, respectively. The Dollar Index is down 36 bps to 102.15 as traders fight the Fed by pricing interest rate hikes and a year-end fed funds rate of 4.42%, a 71-bp discrepancy from the Fed’s 5.13% projected year-end rate.

This morning’s data remind us that the inflation conundrum is not over as the commodity complex continues to pose problems against the backdrop of challenging geopolitical quarrels. With services prices continuing to increase, commodity prices that remain in the woods and a banking system that hasn’t made the first page of the newspaper in about a week, investors are now pricing in a 57% chance of a 25-bp hike in May

Stagflation Risks Increase

This morning’s data remind us that the inflation conundrum is not over as the commodity complex continues to pose problems against the backdrop of challenging geopolitical quarrels. With services prices continuing to increase, commodity prices that remain in the woods and a banking system that hasn’t made the first page of the newspaper in about a week, investors are now pricing in a 57% chance of a 25-bp hike in May. At a time of a climbing fed funds rate, slowing labor market conditions and persistent inflation, stagflation is in the cards.

This post first appeared on April 3rd, 2023 on the IBKR Traders’ Insight Blog

PHOTO CREDIT:https://www.shutterstock.com/g/doimogoju

Via SHUTTERSTOCK

DISCLOSURE: INTERACTIVE BROKERS

Information posted on IBKR Campus that is provided by third-parties and not by Interactive Brokers does NOT constitute a recommendation by Interactive Brokers that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with permission from IBKR Macroeconomics. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and IBKR is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation to buy, sell or hold such security. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

DISCLOSURE: FUTURES TRADING

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

{kind=link}

{kind=link}