By: Kevin Flanagan, Head of Fixed Income Strategy

With the calendar year 2023 barely more than six weeks old, volatility in the money and bond markets has taken center stage. For the U.S. Treasury (UST) market, January (and the first two days of February) could be characterized as a full year’s rally occurring in only about one month’s time frame. However, over the just completed fortnight (that’s two weeks, so you don’t have to Google it), UST yields have completely reversed course, as the market’s narrative has changed dramatically.

This “fortnight” timeframe is what I wanted to go a little bit deeper on. The aforementioned rally to begin the year had its genesis in the notion that the economy would more than likely show signs of heading into recession territory, while at the same time, inflation would continue on its recent “cooling” path, bringing with it increasing talk that disinflation was now the new trend. Of course, these two outlooks don’t happen in a vacuum. In other words, Fed rate hikes would soon be coming to an end, ushering in the next phase of monetary policy, rate cuts, happening sooner rather than later.

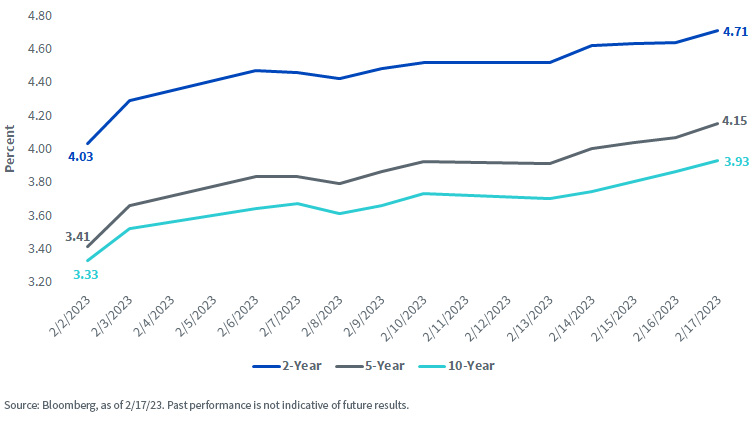

U.S. Treasury Yields

So, what happened? A blockbuster jobs report, to begin with. The completely unexpected surge of more than a half-million new jobs being created in January, combined with the lowest unemployment rate since 1969, represented a direct challenge to the “inevitable recession” narrative. The very solid jobs data was then followed by back-to-back “hotter” than anticipated inflation readings. While declines in year-over-year readings for both CPI and PPI were registered, the actual levels themselves were higher than consensus forecasts. As a result, the disinflation thesis “took a hit” as well.

Against this backdrop, the Fed outlook also underwent a rather noticeable shift. The notion of just one more rate hike at the upcoming March FOMC meeting has now been replaced by the prospect of potentially three more 25-basis-point (bp) increases occurring before Powell & Co. go on an extended pause. To provide perspective, on February 2 (the day before the jobs report), the implied probability for Fed Funds Futures had the terminal rate peaking at 4.90%, but as of this writing, the level has increased to just under 5.30%.

Needless to say, the UST market experienced a reversal of fortune, with yield levels rising considerably all along the curve. The UST 2-Year yield actually reached as low as 4.03% on February 2 and has since surged nearly 70 bps to as high as 4.71%, on an intraday trading basis, over the last two weeks. The UST 5-Year yield followed a similar pattern, increasing by nearly 75 bps. Meanwhile, the UST 10-Year was not to be “outdone,” as a 60-bp increase brought its yield level to within hailing distance of the 4% threshold (3.93%) as of this writing.

Conclusion

As I’ve noted before, this type of heightened volatility should be expected when the Fed and, by extension, the UST market come into full data-dependent mode. We still have a way to go before the next FOMC meeting on March 22. For the record, the policy makers and bond market investors are scheduled to receive one more jobs and CPI report before this convocation. Could the narrative experience another “wind of change”? If the aforementioned data “rolls over,” sure, it’s possible, but right now, I’m leaning in the direction of it not being probable. In this context, it is entirely within the realm of possibility that Treasury yields could still have more room to move to the upside.

Originally posted February 22nd, 2023, WisdomTree

PHOTO CREDIT: https://www.shutterstock.com/g/andrej7

Via SHUTTERSTOCK

Disclosure

Important Risks Related to this Article

Investments in fixed income securities are subject to interest rate risk, credit risk and market risk, each of which could have a negative impact on the value of the Fund’s holdings.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}