By: Lori Heinel, CFA, Global Chief Investment Officer, Gaurav Mallik, Chief Investment Strategist, Simona M Mocuta, Chief Economist, State Street Global Advisors

Monetary tightening is increasing the risk of a technical recession, i.e., two quarters of negative economic growth, but we don’t see substantial risk of a recession that is longer than that.

Last month our Global Market Outlook warned of the risk of a policy mistake. Today, risks are even more skewed to the downside. As central banks navigate inflationary impulses and markets react to the daily news cycle, we are assessing the implications for longer-term growth prospects and the ways in which investors should respond. Given persistent inflation prints and the commitment by central bankers to “get ahead of the curve,” prospects for avoiding a technical recession are declining.

Despite the feedback loop between inflation, wage pressures, and corporate earnings, the past decade has shown us that central bankers do have the tools they need to stimulate growth. We still remain constructive on select risk assets, favoring higher-quality companies that can drive bottom-line growth. We see increasing opportunities in fixed income, given higher yields and the potential for capital appreciation. And we believe that diversification is key, including exposures to assets that are uncorrelated to equities.

Below, answers to six of the most urgent questions we’re receiving from clients help explain our rationale for these views.

1. What is your take on the macro environment and the Fed’s recent actions?

The Fed’s brisk walk toward policy normalization has turned into a veritable sprint with June’s 75 bps hike. The FOMC has made a “whatever it takes” pledge to bring inflation down and that, unfortunately, means serious headwinds for growth. In fact, we seem to be just a hairbreadth away from a technical recession already.

Whether the final Q2 data plays out that way or not, the reality of a sharp growth slowdown is upon us. We look for below-potential growth in 2023 and the possibility of even worse outcomes if the Fed proceeds with all of the hikes it has penciled in. We continue to believe that the data flow over the next few months may allow the FOMC to slow the tightening pace in time to avoid a worst case scenario, but risks are clearly skewed to the downside.

2. What is most concerning to investors about an inflationary environment?

In addition to the macroeconomic effects of higher prices, what concerns us most is the way in which inflation is putting pressure on corporate earnings – i.e., it challenges companies to maintain their margins in a much more fluid business landscape

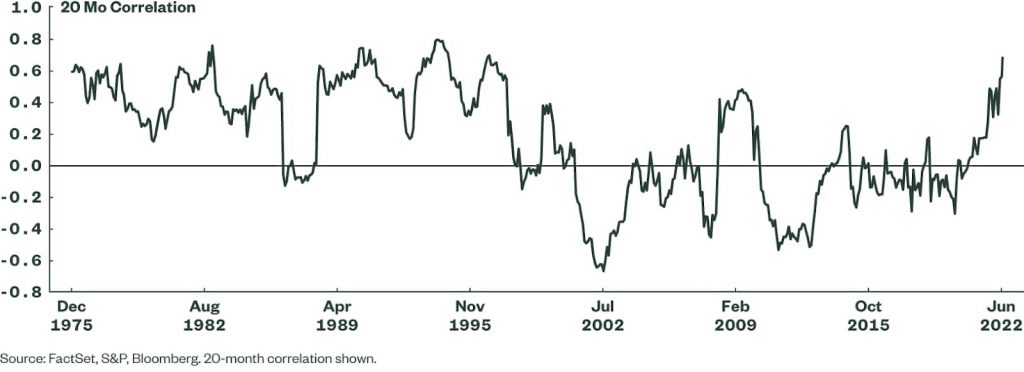

From a portfolio management standpoint, inflation is also concerning because it makes stocks and bonds much more correlated, especially in a slower-growth environment, which limits the options that investors have for portfolio diversification.

Figure 1: Correlation of S&P 500 and Bloomberg US Aggregate Total Return

December 31, 1975 – June 14, 2022

3. Are we approaching a market bottom?

We may be close to a bottom, but close to a bottom is not called a bottom. Macro concerns are unresolved, and there is likely still more pain to be felt by investors in the immediate future. Looking beyond the near term, though, equity markets do display several resilient signs.

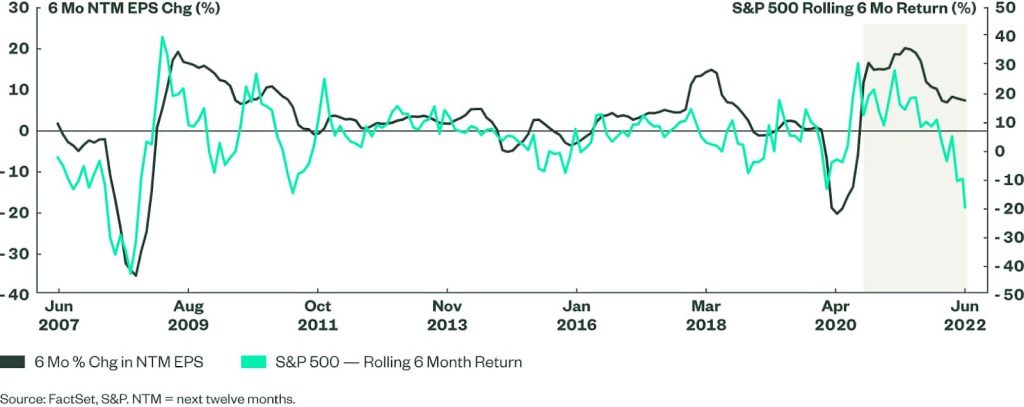

Valuation multiples are below long-term averages and are in-line with the higher rates we are seeing. Earnings have not slowed, and earnings expectations show a continuing upward trajectory. The disconnect between earnings per share (EPS) estimates and market performance is as large as we have seen over the last 10 years (see Figure 2). And while analyst estimates often lag markets, this historically large gap suggests that markets may have overcorrected for an earnings decline.

Current analyst expectations for Q2 EPS is +5.2%, and +9.2% for full-year 2022. In a typical recession, we would see an EPS decline of about 26%, and this level of decline seems unlikely given our expectations for a relatively short technical recession. Conversely, a ~20% decline in the S&P 500 is closer to what we expect to see in protracted recessions. The S&P 500 declined by 29.7% in 1974 (recession lasted 16 months) and by 38.5% in 2008 (recession lasted 18 months). Since 1990, for a typical recession (10 months) the decline is 8.8%.

Figure 2: S&P 500 Rolling 6-Month Returns versus 6-Month % Changes in NTM EPS

June 30, 2007 – June 14, 2022

4. What should I think about portfolio allocation in inflationary times?

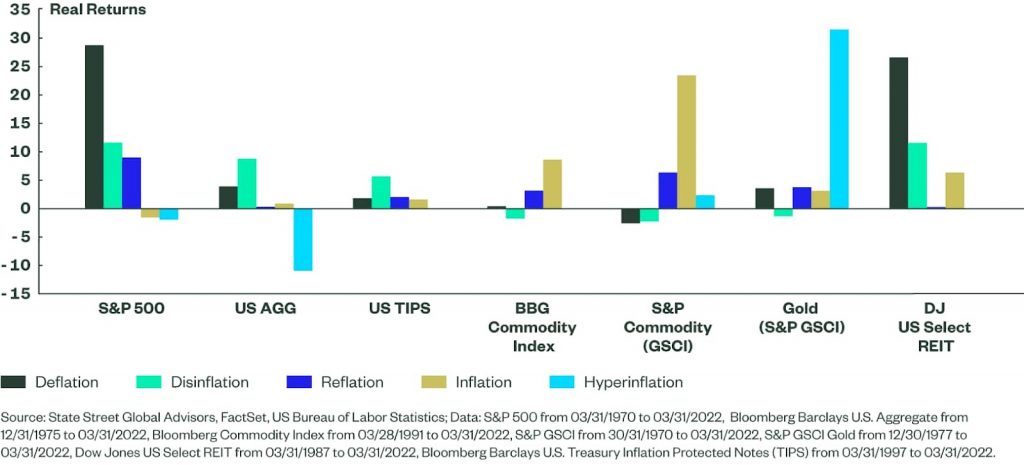

Investors should expect equity assets to underperform in the near term. Figure 3 shows the real returns of various asset classes during different types of inflationary regimes. Given the current high correlation between the returns of stocks and bonds, investors should build hedges. Based on the performances shown in Figure 3, today’s investors might be well advised to hold onto their real assets, which provide the best real returns in inflationary times.

Figure 3: Real Returns of Various Asset Classes, by Inflationary Regime

We Have Been in an “Inflation” Regime Since June 30, 2021

State Street’s current tactical allocation reflects this thinking as well. We are marginally underweight equities, with our view supported by the earning trends and valuations noted earlier. We maintain an underweight to bonds, but are watching cyclical developments and market technicals that might shift that view. We remain overweight to cash and commodities as a hedge to inflation.

5. Where do you see opportunity?

Though we would still expect most investors to be underweight fixed income, strategic investors with longer time horizons should consider buying. Specifically, income-oriented investors are now able to lock in quite attractive yields. Corporate DB pension plans may want to take the opportunity to liability-hedge given high funded ratios, and public pensions can now approach their long-term return targets using only diversified fixed income.

While it is unclear whether we’ve seen a peak in the US 10-year Treasury yield, we’re certainly not too far from it. So it may make sense for investors to consider buying duration. Corporate borrowers remain in strong shape from a balance sheet and earnings standpoint. With regard to High Yield, the potential for recession – and rising defaults – gives us pause. Lastly, valuations in Emerging Market Debt are attractive but are threatened by US Treasury rates and the strength of the dollar.

In sum, while there is value emerging in lower credit, for the time being we would encourage investors to stay invested or add to higher-quality issuers.

6. What indicators are you watching?

There are many, but three indicators are top-of-mind at the moment.

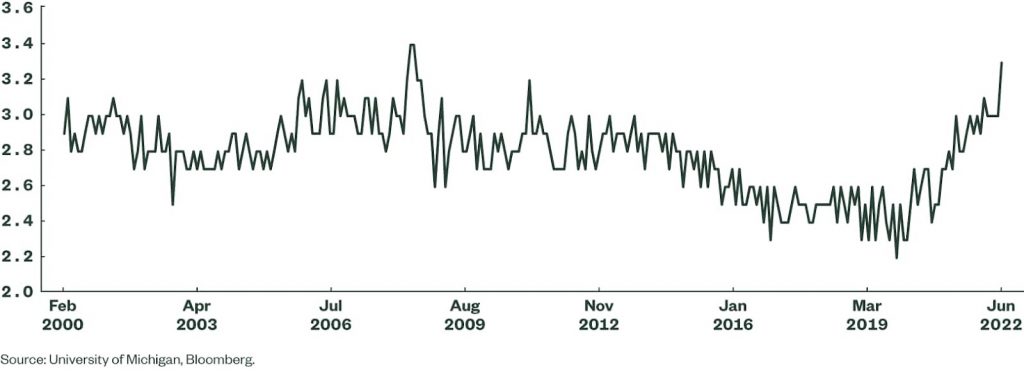

- University of Michigan’s tracking of the expected changes in prices during the next 5-10 years suggests whether inflation expectations are getting anchored. A recent move up of 30 bps suggests that increased inflation expectations are likely to persist (see Figure 4).

- As we enter Q2 earnings season, we are firmly focused on management’s response to policy tightening, as this will indicate companies’ confidence in their ability to manage their margins in the context of higher inflation and higher rates. We expect confidence levels to be reflected in EPS revisions leading into, and getting out of, the earnings season. We look to see if EPS downgrades catch up to the downtrend in equity markets.

- China’s policy path remains a key driver of global risk assets, as it has the ability to provide an easing of supply constraints and a demand stimulus. China’s Covid response has exacerbated supply chain distortions – a “softer touch” on Covid would signal an easing of supply constraints. Unlike other large central banks, the PBOC has been on an easing path, thereby providing a balance against global tightening and stimulating demand.

Figure 4: Expected Changes in Prices During the Next 5-10 Years

Monthly, February 29, 2000 – June 30, 2022

Bottom Line

The FOMC felt that June 15 was their “whatever it takes” moment and wanted to leave no doubt in anyone’s mind that they will do what’s necessary to bring inflation down. We believe that central bankers’ actions will create a steady drag on economic growth, which will likely lead us into technical recession. We do trust that central bankers will limit their actions as necessary to make sure that any such recession is not a protracted one. The “tightening tsunami” is upon us, and we continue to look for hopeful signs, in the markets and from central bankers, that a steady hand is at work.

Chris Sierakowski, Matt Nest, Chris Carpentier, and Keith Snell contributed to this article.

This post first appeared on June 17th, 2022 on the State Street Global Advisors blog

PHOTO CREDIT: https://www.shutterstock.com/g/Bignai

Via SHUTTERSTOCK

Disclosure

Important Information

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

The views expressed in this material are the views of State Street Global Advisors through the period ended June 16, 2022 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research and (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The information provided does not constitute investment advice as such term is defined under the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell any investment. It does not take into account any investor’s or potential investor’s particular investment objectives, strategies, tax status, risk appetite or investment horizon. If you require investment advice you should consult your tax and financial or other professional advisor. All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.

Investing involves risk including the risk of loss of principal.

All the index performance results referred to are provided exclusively for comparison purposes only. It should not be assumed that they represent the performance of any particular investment. The Standard and Poor’s 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United State. The Bloomberg Barclays US Aggregate index provides a measure of the performance of the U.S. dollar-denominated investment grade bond market, which includes investment-grade government bonds, investment-grade corporate bonds, mortgage-pass-through securities, commercial mortgage-backed securities and asset-backed securities that are publicly for sale in the United States. The Bloomberg Commodity Index (“BCOM”) is designed to be a highly liquid and diversified benchmark for commodity investments, which provides broad-based exposure to commodities with no single commodity or sector dominating the Index. S&P Commodity (S&P GSCI®) is a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities. S&P Gold (Gold Index) is designed to provide an investable index of global gold securities. The Dow Jones U.S. Select REIT Index tracks the performance of publicly traded REITs and REIT-like securities and is designed to serve as a proxy for direct real estate investment, in part by excluding companies whose performance may be driven by factors other than the value of real estate. You cannot invest directly in an index.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates rise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

Increase in real interest rates can cause the price of inflation-protected debt securities to decrease. Interest payments on inflation-protected debt securities can be unpredictable.

There are risks associated with investing in Real Assets and the Real Assets sector, including real estate, precious metals and natural resources. Investments can be significantly affected by events relating to these industries.

Investing in foreign domiciled securities may involve risk of capital loss from unfavorable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations.

Investments in emerging or developing markets may be more volatile and less liquid than investing in developed markets and may involve exposure to economic structures that are generally less diverse and mature and to political systems which have less stability than those of more developed countries.

© 2022 State Street Corporation.

{kind=link}