By Anqi Dong, CFA, CAIA, Senior Research Strategist, State Street

- High metal prices, relatively lower energy costs and increasing global demand stand to benefit US metals and mining companies

- Attractive valuations and strong growth prospects combined with geopolitical tailwinds for renewables may bode well for clean energy

- The continued recovery in health care services spending and aging baby boomers boosting Medicare enrollment may support Health Care Service’s growth

With the impact of the Omicron surge fading, Russia’s invasion of Ukraine took center stage of investors’ concern, driving up commodities prices and inflation expectations while posing downside risks to global growth. Meanwhile, the Federal Reserve continued its hawkish shift to rein in multi-decade high inflation, raising its median rates projection for this year by 1% to 1.875% in its March meeting. To help investors navigate geopolitical uncertainties and elevated inflation against a tightening monetary policy backdrop, we identified three industry opportunities to balance near- and long-term opportunities emerging from geopolitical tensions (the Metals & Mining and Clean Energy industries) and a defensive exposure on track for a cyclical recovery from the pandemic to cushion portfolios from the risk of an economic slowdown (Health Care Services).

Metals & Mining: A Favorable Supply Demand Backdrop

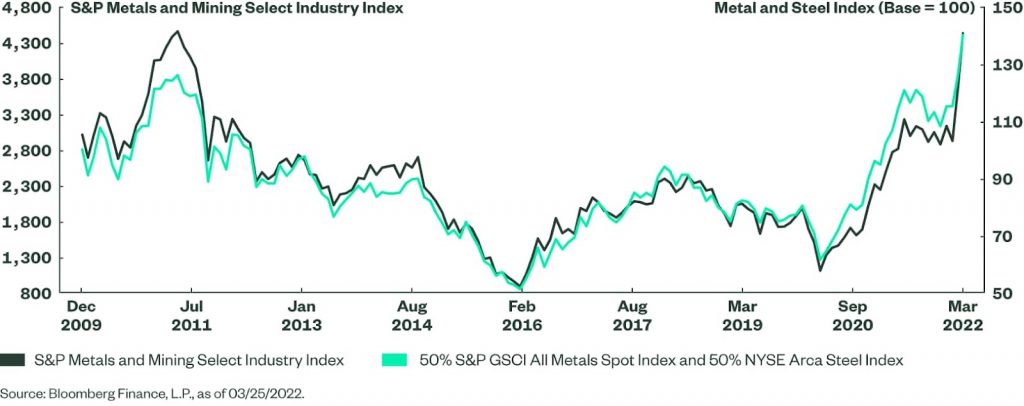

The metals and mining industry has gained more than 40% year to date on the back of surging metal prices amid Russia’s invasion of Ukraine, compared to 4.8% losses of the broad equity market.1 Russia is one of the largest metal exporters in the world, providing a tenth of the world’s copper and aluminum, 4% of steel, a fifth of battery-grade nickel, and over 40% of the world’s palladium.2 While western sanctions did not directly target Russian metals, trade flows on these commodities have been disrupted, as buyers and trade financiers are hesitant to deal with Russian producers in the context of difficulties in settling payments and sanction uncertainty. Furthermore, elevated coal and electricity prices in Europe pushed more European aluminum, nickel and steel producers to cut production, as high energy prices cause financial pains on energy-intensive metal productions.3 These supply disruptions threaten to further squeeze the already tight metal market in 2022, providing support for metal prices.

On the demand side, following weak growth in China last year due to the government’s efforts in deleveraging the real estate sector and taming infrastructure investment, prospects have improved since the end of last year. During the annual central government economic planning meeting in March, the Chinese government set an ambitious growth target for this year despite the domestic resurgence of COVID-19 and an uncertain global recovery, paving the way for more aggressive fiscal and monetary stimulus. The Chinese central bank cut loan prime rates (LPR) twice so far this year and has signaled greater availability of mortgage loans. Banks in more than 50 cities have lowered the down payment requirements for first home purchases and accelerated mortgage approvals after holding back for the second half of 2021. Easing monetary policies and less stringent control on the real estate sector may spur demand for steel in China.

US metals and mining companies stand to benefit the most from high metal prices, relatively lower energy costs and increasing global demand. These tailwinds have driven earnings growth upgrades for 2022 earnings — from negative to 12% since December.4 Even given its stellar year-to-date performance, the industry’s forward price-to-earnings ratio has been compressed further as upward EPS revisions outpaced stock price appreciation.

To capture the upside potential of metal prices, we think investors should consider investing in the SPDR® S&P® Metals and Mining ETF (XME).

Stocks of Metal Producers and Miners vs. Metal Prices

Clean Energy: Geopolitical Tailwinds for Renewables

The recent spike of fossil fuel prices has benefited traditional oil producers. However, if history is any guide, these price increases may ultimately accelerate renewable energy development to make major energy importers, especially those relying on Russia oil and gas, more independent from fossil fuel energy sooner. The oil crisis in the 1970s pushed governments to pass environmental legislation to improve energy efficiency and stimulate investments in renewable energy technology. Between 1974 and 1980, International Energy Agency (IEA) member governments more than doubled their spending on non-fossil-fuel energy R&D.5

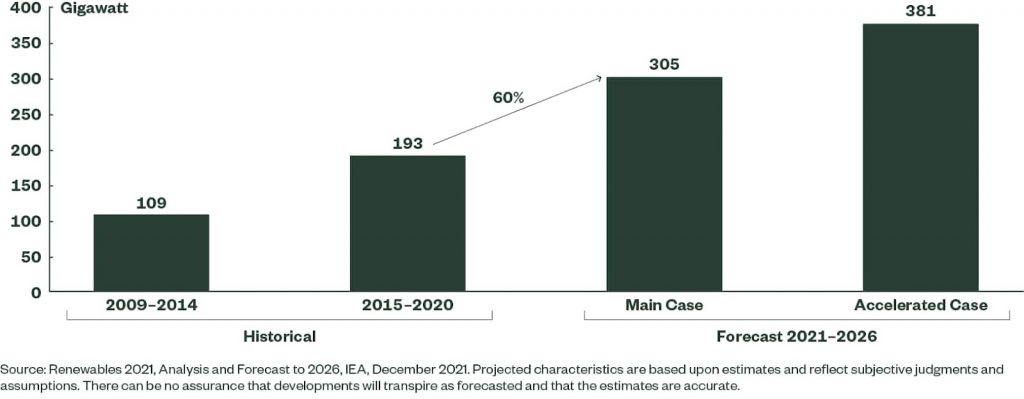

As the Russia-Ukraine War continues, European countries have laid out plans to boost their renewable energy capacity. Germany earmarked 200 billion euros for investment in renewable energy production between now and 2026 and will increase subsidies for consumer solar panel installation and auction off more wind power concessions.6 With the new push, Germany expects to have 100% of its energy coming from renewable sources by 2035, rather than 2050.7 More broadly, the European Commission recently proposed the REPower EU plan aiming to cut the EU’s dependence on Russian gas supplies by raising its climate ambition set under the ”Fit for 55 package”.8 The plan includes installing more solar panels, speeding up renewable project permitting, increasing imported and domestically-produced renewable hydrogen and doubling biomethane production. Even before the Russia-Ukraine War, the growth of renewable capacity was projected to accelerate in the next five years, increasing by nearly 60% and accounting for almost 95% of the increase in global power capacity, given stronger policy support and ambitious climate targets announced for COP26.9 (See the chart below)

Average Annual renewable Capacity Additions

While recent rising raw material costs have reversed the cost reduction trends that the renewable energy industry has seen for more than a decade and weighed on manufacturers’ margins, wind and solar PV generation costs remain lower than fossil fuel, as fossil fuel prices have increased at a much faster pace. Given stronger government policy support and the industry cost advantage, the impact of higher costs on demand may be limited.

After falling nearly 50% from its record high in February 2021, the clean energy industry forward P/E ratio dropped to its lowest level since the pandemic.10 However, the industry’s attractive valuations and improved growth prospects have re-captured investors’ attention, as the industry has rebounded from its one-year trough since February 24th when Russia launched the invasion of Ukraine, outperforming the broad market by 10%, yet still 37% below its record high.11 To position for an acceleration of geopolitical tailwinds for renewables, in our opinion investors should consider investing the SPDR® S&P Kensho Clean Power ETF (CNRG).

Health Care Services: A Cyclical Recovery in a Defensive Sector

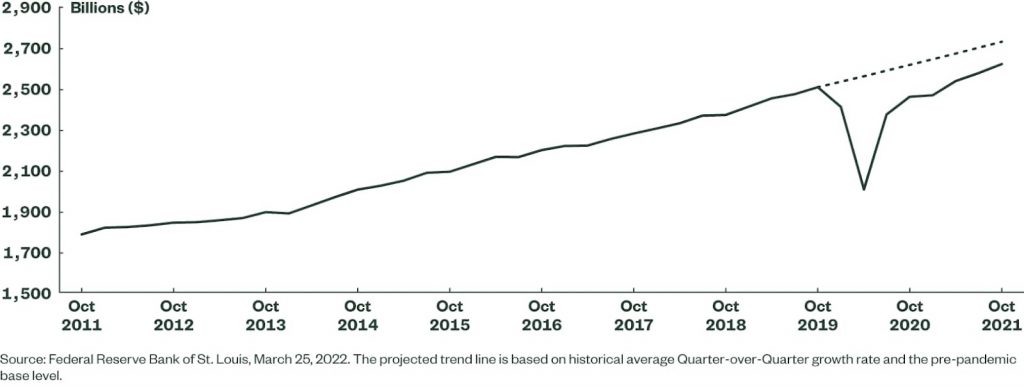

The pandemic has taken a toll on our health care system and disrupted how we manage our health. Data has shown that the rise in the number of COVID-19 cases has been accompanied by drops in non-COVID-19 hospital admissions, doctors’ office visits and elective surgeries due to hospital capacity constraints and patients’ concerns about potential risk of COVID infection at a health care facility. This led to sharp declines in health care spending across all health services at the beginning of the pandemic and slow recovery last year on the back of surging Delta and Omicron variant cases, as shown in the chart below.

Personal Consumption Expenditures: Health Care Services

However, as the Omicron variant turned out not as severe as the Delta variant and the number of cases receded quickly, we have moved from pandemic to endemic, with COVID-related restrictions being lifted and people regaining confidence in accessing the health care system to meet their general medical needs. Since many delayed health care services during the pandemic that cannot be deferred indefinitely, the below-trend spending over the past two years may create pent-up demand for health care services this year, bolstering profits of health care service providers.

Although increasing non-COVID health care utilization may pose headwinds for managed care organizations (MCOs) in the health care services industry by adding costs, their strong Medicaid enrollment growth during the economic downturn may continue due to the lagging effects on enrollment – similar to what was observed two years following the end of Great Recession.12 Meanwhile, aging baby boomers are also set to fuel Medicare enrollment growth through 2029 when the last members of the generation reach the eligible age. These positive enrollment trends may support the industry’s revenue growth and provide a stable source of income over the long run.

In our view the pent-up demand and non-discretionary and stable nature of the business in the industry are highly valuable for investors in the face of high inflation and increasing downside risks of economic growth. To pursue the upside of the continued recovery in health care services spending while seeking to cushion portfolios from the risk of an economic slowdown, we think investors should consider the SPDR® S&P® Health Care Services ETF (XHS)

This post first appeared on April 7, 2022 on the State Street Global Advisors blog

PHOTO CREDIT: https://www.shutterstock.com/g/HTWE

Via SHUTTERSTOCK

DISCLOSURE

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit nor guarantee against a loss.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.

{kind=link}