By Rohan Reddy, Research Analyst, Global X ETFs

The recent rally in energy prices has improved investor sentiment for midstream assets, even though US oil production remains well below pre-pandemic levels.

We believe higher-for-longer oil and natural gas prices could force exploration and production (E&P) companies to drill more and ratchet up production, resulting in greater volumes for MLPs. In the meantime, higher commodity prices have led to aggressive buyback and M&A activity throughout the space.

Further down the road, we anticipate that the master limited partnership (MLP) structure could enjoy an overhaul that potentially includes clean energy assets, which could set the segment up for revitalized growth.

Key Takeaways

- Natural gas is expected to be a major growth driver for the midstream sector in 2022, and the current supply shortfall makes the need for pipeline infrastructure all the more critical.

- We believe the market is discounting US energy production growth given tepid production hikes during the pandemic. However, US energy production is expected to increase in 2022, led by natural gas.

- Energy assets like midstream are more attractive than other sectors in an inflationary environment because of their ability to pass through rising costs to customers.

A Perfect Storm

Economies ramping back up and changing weather patterns that brought colder weather increased demand for natural gas in 2021. Gas prices began the year at $3 British thermal units (Bin the US, but then shot up to more than $5 and then above $6 in the late summer and early fall.

Prices could keep rising through the winter, particularly with natural gas infrastructure already operating at more than 75% of full capacity, which is another factor in the price run-up.1

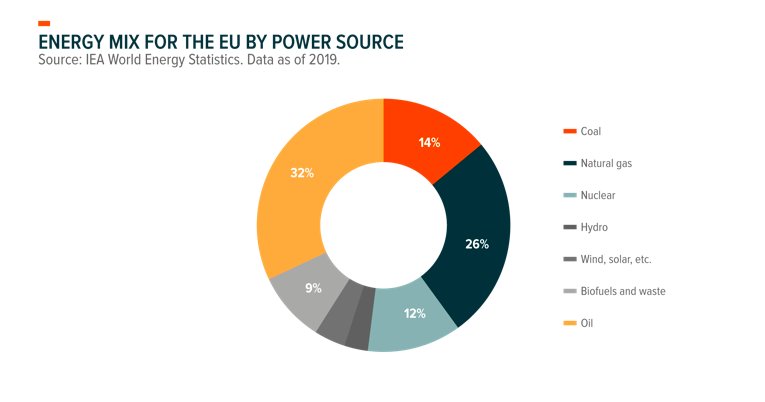

The energy crisis in Europe can be traced to its reliance on Russian gas supply and lower-than-expected wind power output putting additional strain on its oil and gas supplies. Natural gas represents over a quarter of the EU’s energy supply, so the disruption in Russian supply exacerbated an already challenged supply chain.

Inflationary Pressures

Higher oil prices are the result of improving global demand and inflationary pressures. West Texas Intermediate (WTI) hit $80 in early October, nearly double its price in October 2020.

Factors contributing to the increase in 2021 were China’s progress in its economic re-opening in the few months prior and increased global mobility with higher vaccination rates and travel restrictions lifted.

We believe that the resiliency of oil prices through multiple COVID waves, including the most recent delta and omicron variants, suggest that these types of setbacks aren’t enough to derail the trajectory of medium-term oil demand.

Emerging market (EM) demand is still forecasted to be a key source of oil and gas demand relative to developed economies. Rising international trade, resumptions in tourism, and manufacturing activity should serve to drive EM energy demand. Demand is on an upward trajectory, but the key is whether supply can keep pace.

Oil Supply

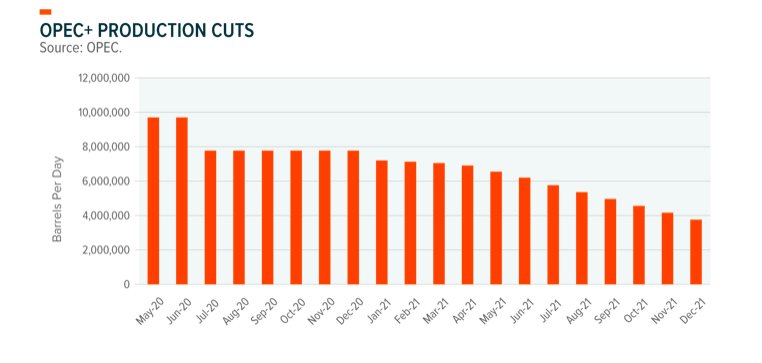

Higher oil prices aren’t just a demand story. Supply levels from major producers still haven’t returned to pre-pandemic levels for several reasons. OPEC+ is increasing its production quotas slowly.

Fears about lingering COVID-19 effects in the winter months may be factoring into the cartel’s decision to not be more aggressive.

Iran

Another reason is the ongoing nuclear negotiations between Iran and the West. If negotiations turn positive and sanctions on Iranian oil production are lifted, another million barrels per day or more could be reintroduced into the market. Iran claims they can produce up to 6.5 million bpd, yet their peak prior to the sanctions was around 3.8 million bpd.

Regardless, higher Iranian oil production would throw a wrench in OPEC’s gradual supply strategy given that the country is exempt from OPEC’s current production quotas. Considering OPEC+ is currently tapering production at a rate of 400,000 bpd, increased production from Iran and/or OPEC+ could drive prices lower. But it’s important to note the fluid nature of the negotiations and that this scenario appears unlikely at the moment.

US producers haven’t been rushing to increase production yet either. Part of their strategy likely speaks to the market’s current preference for more efficient use of capital relative to the macro environment in recent years and capital markets being relatively expensive.

How much longer US producers keep production levels tapered is a big question. Oil production was at just 11.5 million barrels per day at the end of October, well below the peak of 13 million barrels per day in March 2020. Production has been fairly range-bound for most of the pandemic.

Takeaway

Two scenarios could cause US production to rise meaningfully, in our view. First, if investors start rewarding companies for higher production, as was the case prior to the 2014 boom, capital allocation policies could shift to increase capital expenditure (CapEx).

Also, higher rig utilization, typically a precursor to rising production, could follow. Second, if oil prices remain above $80 for a sustained period, producers may not want to sit out the rally, as most projects become economical at those price levels.

When a project is well above its breakeven price, there is little incentive to not utilize the field and raise production. Even more expensive projects like offshore drilling become economical at $80 price levels. However, these scenarios are longer-term possibilities, and they’re unlikely to make a dent in supply heading into 2022.

To read this post in its entirety, click here and visit the Global ETF blog.

Photo Credit: troy_williams via Flickr Creative Commons

FOOTNOTES

Endnotes:

1. Federal Reserve of St. Louis. Data as of 11/30/2021.

Disclosure

This information is not intended to be individual or personalized investment or tax advice. Please consult a financial advisor or tax professional for more information regarding your tax situation. Indices are unmanaged and do not reflect the effect of fees. One cannot invest directly in an index.

Investing involves risk, including possible loss of principal. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume.

Investments in securities of MLPs involve risks that differ from investments in common stock including risks related to limited control and limited rights to vote on matters affecting the MLP. MLP common units and other equity securities can be affected by macro-economic and other factors affecting the stock market in general, expectations of interest rates, investor sentiment towards MLPs or the energy sector, changes in a particular issuer’s financial condition, or unfavorable or unanticipated poor performance of a particular issuer (in the case of MLPs, generally measured in terms of distributable cash flow).

MLPA is taxed as a regular corporation for federal income tax purposes, which differs from most investment companies. Due to its investment in MLPs, the fund will be obligated to pay applicable federal and state corporate income taxes on its taxable income as opposed to most other investment companies.