By Anqi Dong, CFA, CAIA, Senior Research Strategist

While the broad US equity market posted its sixth straight month of gains in Q3, the tug of war between value and growth has intensified, evidenced by record high volatility of return differences between value and growth indices.1

Meanwhile, our economists believe that although inflation driven by supply chain disruptions and pent-up demand during the pandemic recovery might be peaking, rising rent and housing costs may keep inflation elevated next year.2

While the market historically has tended to be bumpier in Q4, inflationary pressure and some secular industry trends may persist regardless of short-term market sentiment. Therefore, we see three industry opportunities for the final quarter of 2021.

REITs: Pursue Income and Total Return in an Inflationary Environment

With interest rates near pre-pandemic lows and actual inflation as well as inflation expectations elevated, US REIT funds’ ability to provide dividend income exceeding inflation has attracted investors this year. Because most leases are tied to inflation, income from leases and property values tend to increase when overall price levels rise.

This supports REITs’ dividend growth and helps investors to pursue real income during inflationary periods. In all but three of the past 20 years, REITs’ dividend increases have outpaced inflation as measured by the Consumer Price Index.3

Although the dividend yield of the US REITs industry has declined to around 3% as some REIT share prices increase, this income level is still much higher than inflation expectations and yields of investment-grade bonds.4 As the REITs sector continues to recover from the economic downturn, increases in lease payments likely will boost dividend distributions.

Total Return

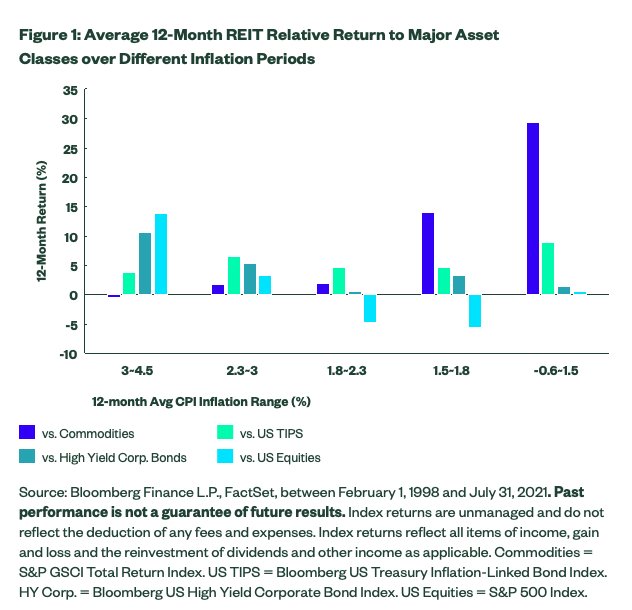

From a total return perspective, REITs also provide investors a powerful tool for inflation hedging. Rolling 12-month average of CPI inflation rate has increased for six straight months in August and now sits at 3%, well above the historical median. While inflation has shown signs of peaking recently, it’s likely to remain elevated in the coming months as the economic recovery continues.

And when 12-month average CPI inflation has been in the top two quintiles, REITs have outperformed broad equities, US Treasury Inflation-Protected Securities (TIPS) and high yield bonds and been on par or slightly exceeded broad commodities, as shown in the chart below. This underscores REITs’ total return advantage over other assets in a high inflationary environment.

Although REIT mutual funds and ETFs have attracted more than $12 billion on a trailing 12-month basis, flows relative to the sector’s asset base are around the historical median of 6% and well below the average of 11% from 2010 to 2012 when the US economy recovered from the last recession.5 This may indicate investors are not overcrowded in terms of sector positioning.

Semiconductors: A Beneficiary of Surging 5G Adoption and World Digitalization

The worldwide semiconductor market is projected to grow 25% to $551 billion in 2021, following 6.8% growth in 2020, according to World Semiconductor Trade Statistics.6

Strong demand for chips may persist in the coming years driven by increasing penetration of 5G smartphones, Internet of Things, and a post-pandemic digital transformation that spurs demand for data centers and cloud services.

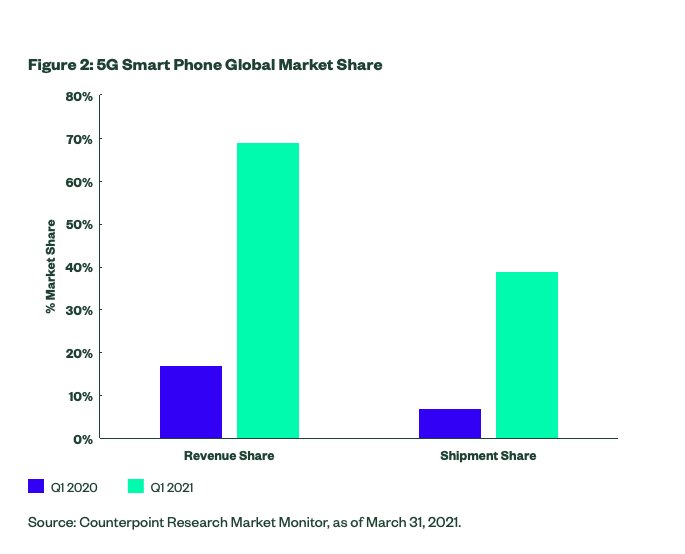

5G smartphones have rapidly gained mobile phone market share, as shown in the chart below. With more mobile phone brands launching 5G-compatible models, the momentum is expected to continue. IDC forecasts that 5G smartphones’ share of global shipments will increase to 69% in 2025.7

As one of the most critical and high-value components of 5G smartphones, smartphone semiconductors are estimated to capture nearly two thirds of the revenue from 5G smartphones,8 one of the largest beneficiaries from the increasing penetration of 5G handsets.

IoT Dynamics

The Internet of Things (IoT) presents long-term and diverse growth opportunities for semiconductors in the 5G era — from smart home devices to industrial and automotive applications.

Integrated circuits that process and store data and execute commands are the essential element of IoT, enabling fast and energy-efficient connections for machines and devices. The IoT may significantly boost semiconductor revenues by stimulating demand for microcontrollers, sensors, connectivity, and memory chips.

Another secular tailwind for the semiconductor industry is the pandemic’s acceleration of digital transformation. The increase in remote work and migration of digital assets to the cloud are two of the largest enterprise shifts that will most likely remain after the crisis.9

The strong demand for data center capacity in enterprise markets has spurred capital expenditure by hyperscale data center operators such as Amazon AWS, Microsoft, Google, and Oracle this year.10 The memory integrated circuit makers are the key beneficiary of this rapid growth, as the segment is the industry’s largest growth contributor.11

Biotech: A Secular Growth Opportunity with Attractive Valuations

The biotech industry had a maximum drawdown of 32% since its peak in February this year.12 Even after rebounding 12% from its August trough, the industry still lags the healthcare sector and broader market by 23% and 25% year to date.13

Over the past 15 years, there were only two periods when the industry suffered a loss greater than 30% over a six month or longer period: 2015-2016 triggered by Hillary Clinton’s tweets about drug pricing and 2008-2009 during the global financial crisis.14 Both times biotech recovered from the downturn to stage a strong multi-year rally.

Historically, when the biotech industry has had more than a 10% drawdown, returns for the following years have most often been quite positive, as shown in the histogram chart below. The average return for the next 12 months after a 10% drawdown was 24%, with 81% of the time producing positive returns.

Longer-term performance was even stronger, with 46% and 65% average cumulative returns for the following two and three years, respectively. Therefore, historical statistics suggest this year’s biotech selloff might create a great entry point for investors who are looking for long-term growth opportunities but can also stomach the sector’s high volatility.

To read this post in its entirety, click here and visit the State Street Global Advisors blog.

Photo Credit: phsymyst via Flickr Creative Commons

Footnotes

1FactSet, as of 10/1/2021. Value and Growth are represented by the S&P 500 Value and S&P 500 Growth indices.

2Weekly Economic Perspectives Quarterly Edition, September 27, 2021.

3Nareit, S&P Global Market Intelligence, as of December 2020.

4Bloomberg Finance L.P., as of 9/24/2021.

5Morningstar, as of 8/31/2021.

6Worldwide Semiconductor Market Outlook, World Semiconductor Trade Statistics, 8/16/2021.

7IDC, as of 3/10/2021.

8IDC forecasts $522B semiconductor market in 2021, May 2021.

9How COVID-19 has Pushed Companies Over the Technology Tipping Point and Transformed Business Forever, McKinsey, October 2021.

10AWS, Microsoft, Google Lead $38B Data Center Capex In Q1, CRN.com, June 2021.

11Worldwide Semiconductor Market Outlook, August 2021, World Semiconductor Trade Statistics.

12Bloomberg Finance L.P., as of 9/23/2021.

13Bloomberg Finance L.P., as of 9/23/2021.

14Bloomberg Finance L.P., as of 9/23/2021.

15FactSet, as of 9/16/2021.

16Biotech Industry Survey, CFRA, September 2021.

Disclosure

This communication is not intended to be an investment recommendation or investment advice and should not be relied upon as such. All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The views expressed in this material are the views of SPDR ETFs and SSGA Funds Research Team through the period ended September 28, 2021 and are subject to change based on market and other conditions and do not necessarily represent the views of State Street Global Advisors or any of its affiliates. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Past performance is not a reliable indicator of future performance. Investments in small-sized companies may involve greater risks than in those of larger, better known companies. Targets are estimates based on certain assumptions and analysis made by SSGA. There is no guarantee that the estimates will be achieved.

Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs. Concentrated investments in a particular sector or industry tend to be more volatile than the overall market and increases risk that events negatively affecting such sectors or industries could reduce returns, potentially causing the value of the Fund’s shares to decrease. Passively managed funds invest by sampling the Index, holding a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. This may cause the fund to experience tracking errors relative to performance of the Index.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions. Funds investing in a single sector may be subject to more volatility than funds investing in a diverse group of sectors. Investing involves risk including the risk of loss of principal.

Real Estate Investment Trusts (REITS) investing may be subject to risks including, but not limited to, declines in the value of real estate, risks related to general economic conditions, changes in the value of the underlying property owned by the trust and defaults by borrowers.Technology companies, including cyber security companies, can be significantly affected by obsolescence of existing technology, limited product lines, and competition for financial resources, qualified personnel, new market entrants or impairment of patent and intellectual property rights that can adversely affect profit margins.

{kind=link}