By Michael W Arone, CFA,Chief Investment Strategist

Throughout summer investors have been inoculated against various potentially infectious market diseases — the Delta variant surge, China’s regulatory crackdown across a number of domestic industries, D.C. dysfunction, Federal Reserve taper talk, the US withdrawal from Afghanistan, global weather disasters, plummeting consumer confidence and an economic growth scare.

Perhaps investors have already received their booster shots, fueling their feelings of invincibility against plausible market risks. Despite all the possible doom and gloom scenarios, markets are at all-time highs1 and valuations remain above their long-term averages.2 So, what is the engine that keeps stocks climbing that proverbial wall of worry to reach new heights? Simply, it’s outstanding corporate earnings results.

Come on Feel the Noise

Investors have quieted one noisy distraction after another this summer and that hairy list of risks hasn’t moved markets because revenues, earnings growth and profit margins have been phenomenal. And, it hasn’t been just the latest quarter (Q2’21) — it’s been the past five quarters dating back to last year (Q2’20). According to FactSet, S&P 500 companies on average over the past five quarters (Q2’20–Q2’21) are reporting earnings that are 19.3% above analysts’ expectations — an earnings surprise percentage notably above the 5-year average of 7.8%.

If, as most analysts expect, the second quarter represents the post-pandemic peak in revenue, earnings and profit margin growth rates, at least the quarter will have gone out with a bang! According to FactSet, as of August 13, 87% of S&P 500 companies reported both revenue and earnings surprises for the second quarter. This marks the highest percentage of S&P 500 companies reporting revenues above estimates (87%) and the highest revenue surprise percentage (4.9%) for a quarter since FactSet began tracking these metrics in 2008.

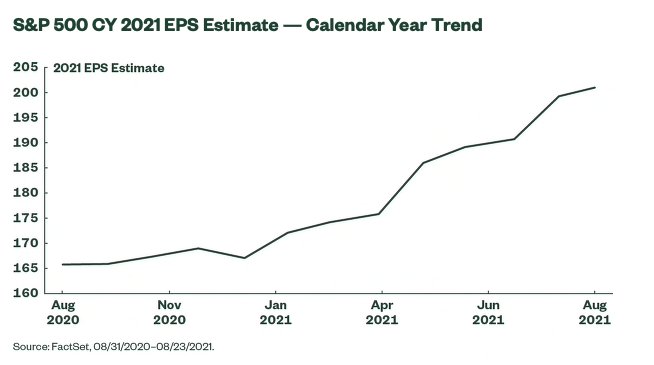

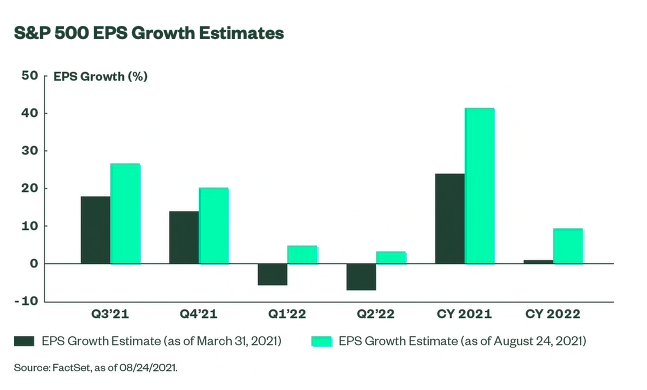

Amazingly, companies were able to beat revenue expectations despite the fact that analysts kept raising the bar. For example, on March 31, the estimated revenue growth rate for the S&P 500 for Q2’21 was 16.6%. By June 30, it was 19.4%. Today, the year-over-year revenue growth rate for the second quarter of 24.9% marks the highest reported figure by the S&P 500 Index since FactSet began tracking this metric in 2008.

The year-over-year earnings growth rate for the S&P 500 for the second quarter is a whopping 89%, the highest reported figure since the fourth quarter of 2009. The unusually high growth rate is due to higher earnings in Q2’21 and an easier year-over-year comparison to lower Q2’20 earnings as the result of COVID-19’s negative impact on a number of industries. All eleven sectors reported year-over-year earnings growth, led by the energy, industrials, financials, consumer discretionary, and materials sectors.

Earnings Landscape

The S&P 500’s second quarter net profit margin of 13% — above both the 5-year average of 10.6% and the previous quarter’s record 12.8% and the highest since FactSet began tracking this metric in 2008 — is the biggest surprise of the earnings season. With supply chain challenges and rising inflation making headlines all year, investors have widely expected higher costs to eventually slash businesses profit margins.

However, all eleven sectors are reporting a year-over-year increase in their net profit margins, led by the financials, industrials and materials sectors. So far, in aggregate, supply chain disruptions and higher input costs have not cut S&P 500 companies’ profit margins.

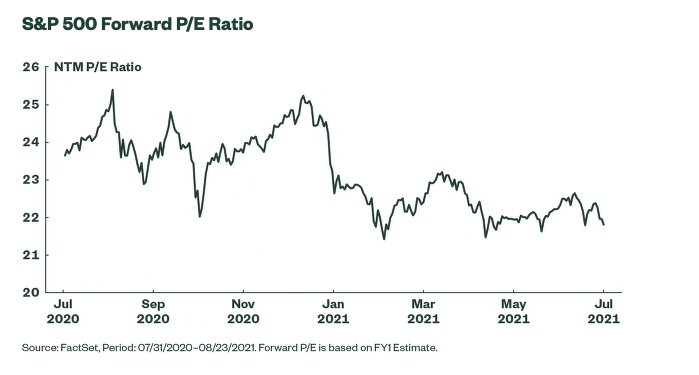

Finally, there’s another strange twist to all these magnificent corporate earnings results. While the market rally continues, stock prices have struggled to keep pace with surging earnings forecasts. As a result, forward price-to-earnings multiples have been declining, falling from 23.2 last August to 20.6 today. Lower price-to-earnings multiples give investors false confidence that valuations are becoming more attractive and that stock prices will catch up to earnings growth. This underscores how earnings have been the overwhelming driver of huge stock price gains during the past year.

Don’t Let it End

Ironically, if stellar earnings results are indeed the primary reason markets keep setting all-time highs, it just might be that future earnings results are the market’s biggest risk.

Revenue and earnings surprises have been so big over the past five quarters because analysts have persistently underestimated both since the middle of last year.

And as analysts have continued to increase their estimates to account for this unanticipated growth, declining forward price-to-earnings multiples have encouraged investors to look past stretched valuations and to assume that corporate earnings will always easily beat expectations.

To read this article in its entirety, please click here and visit the State Street Global Advisors blog.

Photo Credit: herval via Flickr Creative Commons

Footnotes

1 FactSet, Period: 01/03/1928–07/31/2021. S&P 500 used to represent the overall market.

2 FactSet, Period: 09/29/2006–07/31/2021. S&P 500 used to represent the overall market.

DISCLOSURE

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The Standard and Poor’s 500, or simply the S&P 500, is a stock market index tracking the performance of 500 large companies listed on stock exchanges in the United States. Investors can’t invest directly into indexes.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The views expressed in this material are the views of Michael Arone through the period ended August 25, 2021 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward looking statements.

Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal.

Past performance is no guarantee of future results.

All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.

{kind=link}