By Steve Sosnick, Chief Strategist at Interactive Brokers

Does anyone doubt the resolve of the Federal Reserve to maintain an accommodative monetary policy? Monetary stimulus has been a key feature of the stock market’s relentless rise since the depths of the covid crisis, and easy money has almost undoubtedly boosted prices of bonds, commodities, and non-traditional assets as well. I’ll stop short of asserting that modern financial markets are addicted to central bank liquidity, though investors have a near-Pavlovian response to news of fresh monetary stimuli.

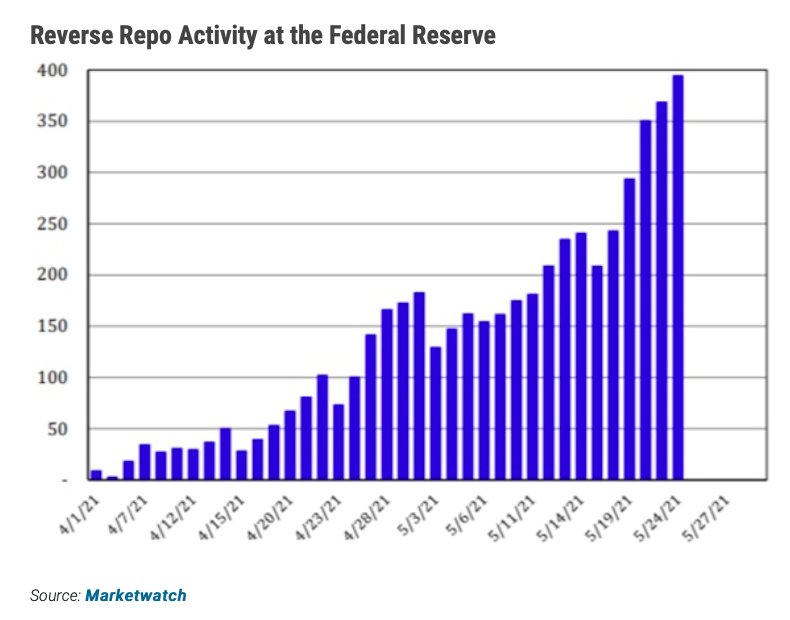

Why then is the Federal Reserve actively draining cash from the banking system? This is evident from the reverse repo activity that has been growing rapidly over recent days. The following graph illustrates that trend:

A general rule of thumb for understanding how the Fed adds or subtracts liquidity from the system is to see whether it is buying or selling securities. Buying securities adds cash to the system. If the Fed is buying securities, it exchanges money for them. That money enters the financial system in the form of cash or cash equivalents. The Fed increased its balance sheet in an unprecedented manner over the past year. Much of that rise was achieved by purchasing Treasury notes in the open market, and that money flowed into the banking system. If the Fed is selling securities, that means that they receive cash in exchange for them. That cash leaves the banking system.

On a short-term basis, the Fed can manage systemic cash flows via the use of repurchase agreements, more commonly known as repos. A repo is a temporary purchase of securities. The Fed buys securities from primary dealers and agrees to sell them back at a predetermined date. It is effectively a short-term loan of cash to the financial system. A reverse repo does the opposite. The Fed sells securities to dealers with an agreement to buy them back at a predetermined date. That temporarily removes cash from the banking system. And that is the activity that is increasing rapidly over recent days.

The Federal Reserve Bank of New York (FRBNY) operates the main trading arm of the Federal Reserve system via its open market operations, and their website is an excellent way to keep track of their activities. We see that they have been engaging in overnight reverse repos at a far greater pace than “regular” repo activity. On a one-day basis, this would hardly be newsworthy. There are many benign reasons why the Fed might see the need to drain excess reserves from the banking system for a day. It is quite common for the Fed to help banks smooth out their cash flows and balance sheets around quarter or year-ends. That said, they are engaging in a temporary measure that grows daily and it is not a customarily seasonal time. It appears that greater scrutiny may be required.

The obvious answer is that there is simply too much cash sloshing about the system, and the Fed is offering banks a place to park it. If that is true and persistent, will this force the Fed to reconsider the pace of its monetary stimulus? Another answer is that there is a shortage of short-term government securities that banks can invest excess cash in. That could be caused by the Fed’s relentless purchase of Treasury notes and might also cause the Fed to reconsider the pace of its activities. Neither is a happy prospect for investors who crave central bank liquidity.

The FRBNY’s FAQ web page explains that reverse repo activities don’t have a lasting effect on the Fed’s balance sheet. The assets remain the same, though the associated liabilities shift from one counterparty to another. For that reason, we don’t see the reverse repo activity causing immediate market worry. There is no evidence yet that the Fed is shrinking the growth of its balance sheet, let alone shrinking it outright. If there is a concern, it is on the horizon, not in our face. But keep two factors in mind: 1) that monetary policy tends to impact stocks on a 6-week to 3-month lag, and 2) that markets tend to discount events months in advance.

Those two factors are in conflict though. If I’m forced to guess, I would think that markets would be more likely to ignore unhelpful concerns about monetary policy until they become evident sources of worry. Last week’s release of Federal Reserve meeting minutes indicated that they might be “thinking about thinking about” changes to monetary policy. This is the financial market’s equivalent of what goes on in a high school cafeteria. If one of my friends or I liked a girl but didn’t want to face rejection, we would put out very tentative initial feelers that one of us was thinking about thinking about asking out the girl in question.

A tentative yes meant that we could drop the first “thinking about” from the discussion. Since I didn’t hang out with a bunch of Casanovas, the actual thinking could then proceed over a period of weeks and could be dropped anyway. This is not at all different from the Fed’s current thinking, except that public rejection would have far greater consequences than a momentary humiliation on the bus home. So far, investors have taken the Fed’s tentative comments in stride, along with the minor steps to drain liquidity via reverse repos. We’ll see over coming weeks whether the tentative comments become more concrete, and whether markets accept or reject the Fed’s next moves.

This post first appeared on May 26 on the Traders’ Insight blog.

Photo Credit: Kurtis Garbutt via Flickr Creative Commons

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}