By Sergiy Leysk, director, research & analysis

Since the start of the COVID crisis, real estate equities have faced significant headwinds, with different segments of this market suffering to varying degrees.

By the end of 2020, the FTSE EPRA Nareit Developed Index had underperformed the FTSE Developed Index by almost 30% in US dollar terms.

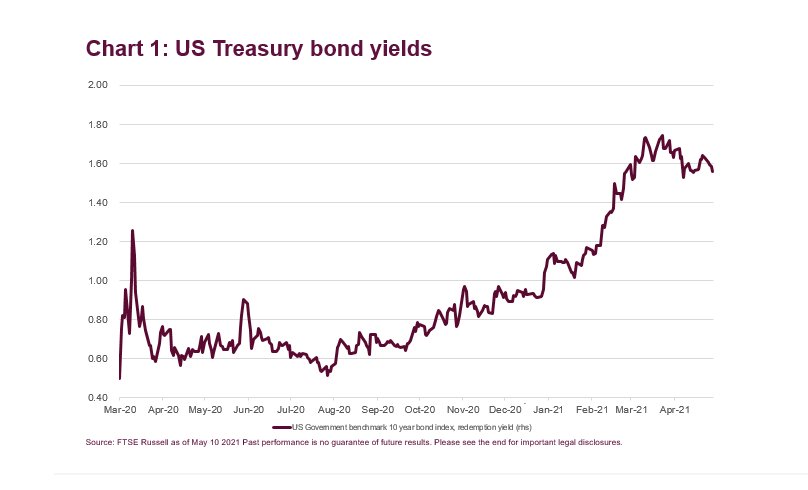

Moreover, since August 2020, listed real estate equities have been confronted by a new challenge ‒ rising bond yields (Figure 1) as a higher discount rate and cost of capital would tend to imply lower equity valuations.

Since the great financial crisis (GFC), there were two notable periods when bond yields have risen significantly: The 2013 “taper tantrum” and the 2009 post-crisis recovery. But for each period, listed real estate equities performed differently.

Taper tantrum

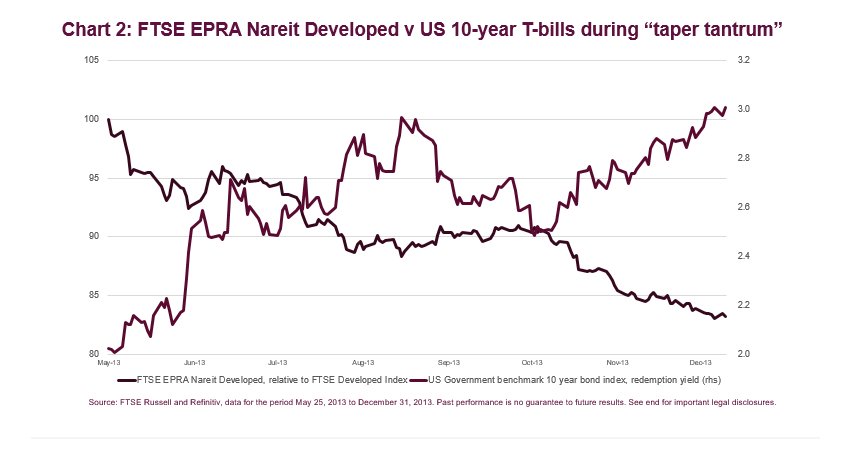

The last time bond yields jumped by a similar stark 1% was during the so-called 2013 “taper tantrum,” when real estate equities underperformed by more than 15% from the end of May 2013 to the end of that year, as Figure 2 shows.

Recovery in 2009

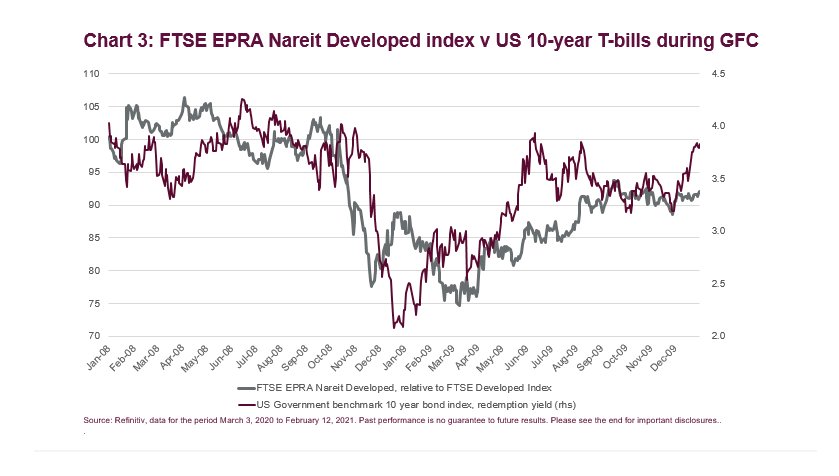

In contrast to the 2013 taper tantrum, during the post-crisis market recovery in 2009, real estate equities outperformed the wider equity market as bond yields rose (Figure 3).

However, real estate performance during the COVID-19 phase is reminiscent of what was observed during the post Global Financial Crisis recovery.

After the initial COVID shock in March 2020 and sharp decline, listed real estate equity returns held up relatively well versus the wider equity market, while bond yields rose.

One of the reasons for their relatively stable performance might be explained by the rising bond yields and changing weights structure of the listed real estate sector.

Inflation fear is one consequence of rising bond yields. Similarly to the period immediately after the GFC in 2009, the market is fearful of rising inflation stemming from significant monetary expansion by central banks to stimulate the global economy.

As previous research demonstrated (see references [1]-[3]), higher inflation expectations are particularly supportive of residential real estate prices. We have witnessed recently that residential is one of the best performing components of listed real estate.

There are other reasons for strong performance of residential real estate, for example, the structure of financial support for business and households during the COVID crisis, stamp duty relief in the UK and ban on evictions in the US, to name just a few.

Investors should exercise caution going forward, however. Some drivers of the real estate price growth may be removed and investors need to watch the space.

This post first appeared on May 27 on the FTSE Russell blog.

Photo Credit: kjarrett via Flickr Creative Commons

References:

[1] Fama E., Schwert, G. Asset returns and inflation. Journal of Financial Economics, 1977, 5, pp. 115-146.

[2] Rubens, J., Bond, M., Webb, J. The inflation-hedging effectiveness of real estate. Journal of Real Estate Research. 1989. 4, pp.45-46.

[3] Bill Wheaton. Has Real Estate Been a Good Hedge Against Inflation. CBRE blog July 2017.

© 2021 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) MTSNext Limited (“MTSNext”), (5) Mergent, Inc. (“Mergent”), (6) FTSE Fixed Income LLC (“FTSE FI”), (7) The Yield Book Inc (“YB”) and (8) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “MTS®”, “FTSE4Good®”, “ICB®”, “Mergent®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, FTSE Canada, Mergent, FTSE FI, YB or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

The FTSE EPRA Nareit Global Real Estate Index Series is designed to represent general trends in eligible real estate equities worldwide. The FTSE Developed ex US Index is part of a range of indexes designed to help USinvestors. benchmark their international investments. Investors can’t invest in an index directly.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a licence from FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and/or their respective licensors.