After digesting the latest employment data, I couldn’t help but think of the classic Pink Floyd song, “Breathe.” You could almost hear Federal Reserve (Fed) Chairman Powell breathe a sigh of relief following the release of the May jobs report.

Pressure, external—and in some cases perhaps internal—seemed to be building for the Fed to begin their discussions about when/how to begin tapering their current quantitative easing (QE) program.

While the May employment data continued to show progress being made within the nation’s labor markets, it fell short of creating any urgency for the Fed to shift course in the immediate future.

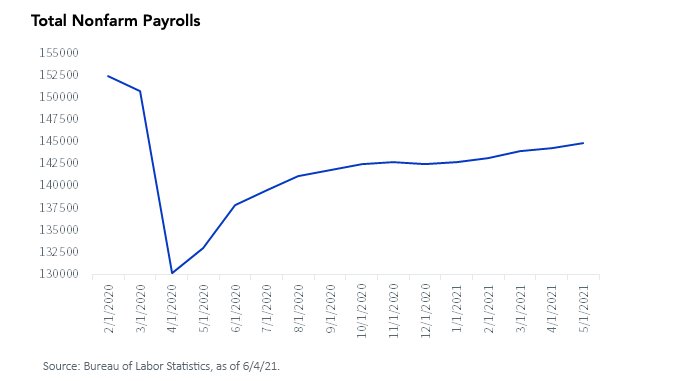

Total nonfarm payrolls (NFPs) rose by +559,000 in May, once again falling visibly below the consensus forecast of +675,000. If there is a silver lining, at least this time around, it’s that it wasn’t the “worst miss” on record. As you can see in the above graph, the pace of improvement for NFPs has definitely trailed off.

Through October, job gains had recovered 55% of the plunge in job losses that occurred during the height of the pandemic shutdown in March/April 2020. However, that figure has only managed to climb to about 66% through May. In other words, incremental progress of only a little more than 10% over the last seven months.

A great deal of attention has been placed on inflation of late, and rightfully so, in my opinion. However, Powell & Co. have tended to downplay that portion of their dual mandate (it’s just transitory, remember?) and instead focus on the employment aspect to continue to justify their unprecedentedly stimulative monetary policy.

While the unemployment rate fell -0.3 pp to 5.8%, this had more to do with a decline in the civilian labor force as the “participation rate” dropped during the month. Based upon the May jobs data, the employment part of the equation still has a way to go, especially in Powell’s eyes.

Certainly, there has been a lot of discussion as to why job gains are not necessarily lining up with the broader economic recovery. Without going too far down that rabbit hole, generous unemployment benefits that serve as a disincentive to return to work have been mentioned as one probable cause while childcare and continued health concerns also enter the mix.

There’s no doubt the Fed is fully aware of these potential factors as well, which is why, up to this point anyway, Powell has been taking a more cautious approach to removing any accommodation.

Conclusion

How about we wrap up this blog post with a quick thought about the upcoming FOMC meeting on June 16? While there are no meaningful changes expected to the Fed’s policy statement, I am curious to see how Powell responds to questions at the presser regarding any discussions that have taken place around an “exit strategy,” aka tapering.

Also, this meeting will have the Fed’s updated Summary of Economic Projections. Specifically, I’m looking at their Fed Funds estimates (blue dots). While 2024 was still the median forecast in March, the number of Fed officials looking for a rate hike in 2023 did increase a bit from the prior estimate. Will this trend continue? That’s what I’m interested to see.

This article first appeared on June 9 on the WisdomTree blog.

Photo Credit: marviikad via Flickr Creative Commons

DISCLOSURE

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

{kind=link}