By Matthew J Bartolini, CFA, Head of SPDR Americas Research

Broad-based equities have registered gains so far this year, supported by accommodative monetary and fiscal policies, encouraging economic data and higher COVID-19 vaccine rates than case rates. Yet, this is not just a broad beta rally.

The current market environment appears highly conducive to sector investing based on two variables: correlation and dispersion. Simply put, a high dispersion of returns across sectors indicates opportunities to generate alpha by correctly over- and under-weighting certain market segments. And a low pairwise correlation across sectors, where assets are moving more independently from one another, means returns are not clustered around one driving market force.

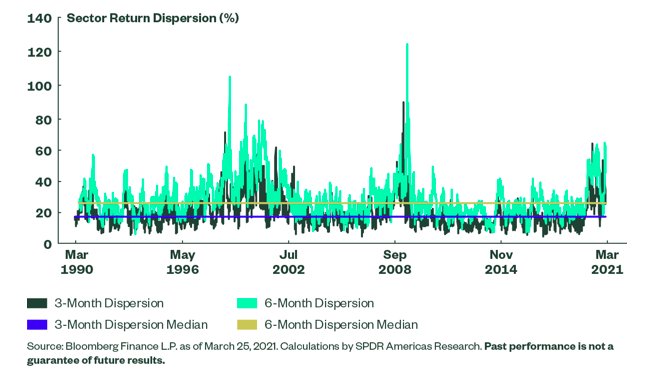

Sector return dispersion elevated

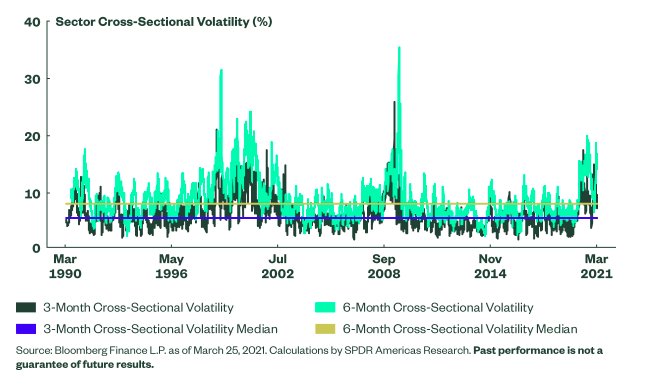

Return dispersion equates to the difference between the best- and worst-performing asset (in this case, S&P 500 GICS Sectors) within a group over a specified period. Here, we analyzed three-month and six-month return periods. As shown below, both three- and six-month return dispersions (29% and 56%, respectively) are well above the median level historically, as well as in the 80th percentile. In fact, the six-month return dispersion figure is in the 96th percentile.1 And this is not just the by-product of lopping off weaker and more similar returns, as the three-month return dispersion figure has remained above the 80th percentile for 60 consecutive days. That consistency has not been seen since 2008.

Another way to examine dispersion is to look at the cross-sectional volatility of assets. And in this case, dispersion is also elevated, as shown below.

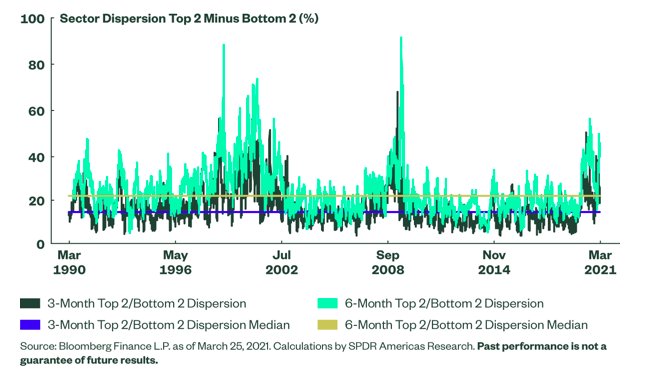

While the two examples above suggest an environment that may lead to alpha opportunities, a third study may refute any notion that dispersion is being led by one high performer and one weak performer, with the rest of the sectors registering muted returns. For this, we calculated the average returns of the top two and bottom two performing sectors over both rolling periods. As shown below, this top two/bottom two dispersion sort also illustrates a constructive dispersion environment for over- or under-weighting specific sectors. This differential sits in the 82nd and 96th percentiles, respectively.

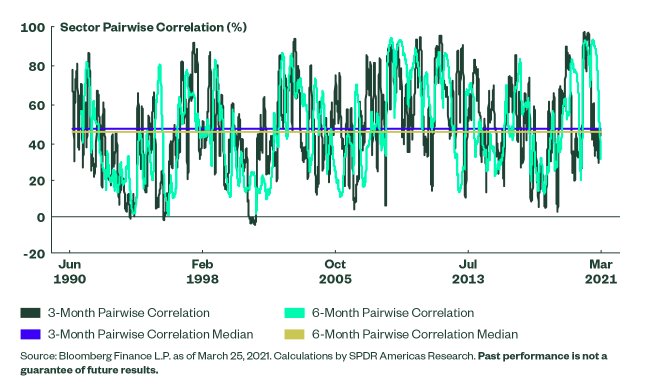

Correlations are constructive

Low correlations among sectors (pairwise correlations) and high return dispersion support the alpha argument. Sectors moving more indifferently to each other signify less of a clustered return environment where returns are being driven by a confluence of macro or fundamental variables — rather than by just one factor (e.g., beta). As shown below, rolling three-month and six-month pairwise correlations for sectors are below the historical median correlation figure and have been for some time — adding to the persistency argument.

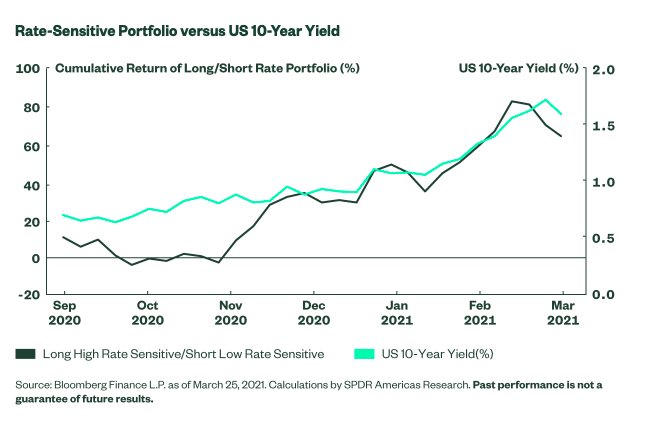

The differentiated correlation environment can be partly attributed to the reflationary rate regime shift that we are witnessing, where higher rates are having a disparate impact on sectors based on how sensitive the firms within those markets are to the US 10-year. This is evident when comparing the returns of two sector portfolios (a high rate- sensitive and low rate-sensitive) over the past few months. The high rate-sensitive portfolio contains Energy and Financials, while the low rate-sensitive portfolio contains Real Estate and Consumer Staples, based on the data from our dashboard. Both portfolios for this example hold each sector at equal weights and rebalance weekly. The cumulative long/short returns versus the trend in the US 10-year yield are shown below.

Rate-Sensitive Portfolio versus US 10-Year Yield

Beyond the impact of rising rates, there are other factors at play in our current environment that help illustrate the differentiated return trends: higher commodity prices, stretched valuations for past winners (i.e., Tech and Discretionary), earnings growth revision trends (i.e., Energy and Financials), and what sectors will lead or lag based on the uncertain vibrancy of this recovery.

Constructing sector portfolios

There are generally four ways to analyze sector strategies to implement alongside core exposures.

- Top Down: Examine macro trends and data to understand the business cycle tendencies and what sectors may be conducive for environments when specific macro variables (rates, oil, inflation, dollar, business confidence) are in favor.

- Bottom Up: Survey sector-level fundamentals such as valuations or earnings sentiment to create a portfolio that aligns with your fundamental view of the world. For instance, based on February’s quantitative monthly scorecard, a two-sector value portfolio would contain exposure to Energy and Financials

- Technical: Allocate based on volatility information, technical indicators or momentum data in order to seek out areas with positive trends — or defensive properties for a low-beta or defensive sector portfolio. As shown in our February scorecard, the top two sectors with positive momentum are currently Financials and Technology.

- Thematic: With a more specific focus than top down, seek out areas that align with a particular theme, such as Retail for the increase in consumer spending amid a hopeful recovery. Or position for changes in a post-pandemic world with funds focused on innovation. We detail the latest trends in our monthly dashboard and our quarterly sector investment outlook.

Taking a sector focus now

While the return dispersion and correlation figures are backward-looking metrics, the persistency of the data combined with the ongoing evolution of this recovery portend an environment that may continue to support specific sector allocations as a way to pursue alpha.

To read this entire article, which first appeared on the SPDR blog on April 1, please click here.

Photo Credit: thenails via Flickr Creative Commons

Footnotes

1 Bloomberg Finance L.P. as of March 25, 2021

2 Bloomberg Finance L.P. as of March 25, 2021

DISCLOSURE

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The views expressed in this material are the views of SPDR ETFs and SSGA Funds Research Team through the period ended March 25, 2021 and are subject to change based on market and other conditions and do not necessarily represent the views of State Street Global Advisors or any of its affiliates. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or

developments may differ materially from those projected. The information provided does not constitute investment advice and it should not be relied on as such.

Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs.

Diversification does not ensure a profit or guarantee against loss.

Because of their narrow focus, sector investing tends to be more volatile than investments that diversify across many sectors and companies. Concentrated investments in a particular sector or industry tend to be more volatile than the overall market and increases risk that events negatively affecting such sectors or industries could reduce returns, potentially causing the value of the Fund’s shares to decrease.

Passively managed funds invest by sampling the Index, holding a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. This may cause the fund to experience tracking errors relative to performance of the Index.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions. Funds investing in a single sector may be subject to more volatility than funds investing in a diverse group of sectors.

Investing involves risk including the risk of loss of principal.

Growth stocks may underperform stocks in other broad style categories (and the stock market as a whole) over any period of time and may shift in and out of favor with investors generally, sometimes rapidly.