Coronavirus cases are now beginning to rise across the country and, in my view, this may severely damage the bull market narrative of a smooth US economic reopening in the second half.

Remember, the bullish argument rests on two factors: 1) a V-shaped economic recovery and 2) a Fed liquidity-driven event. In my view, both have serious issues right now.

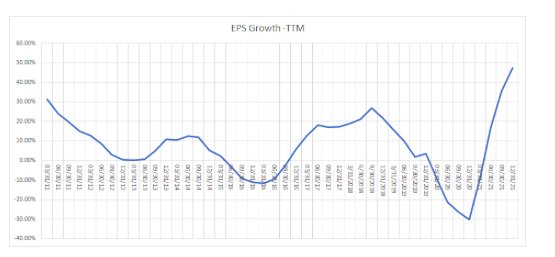

The V-shaped recovery is still very much priced into the market based on the shape of the recovery in earnings estimates, according to my analysis. The latest earnings-per-share growth data from S&P Dow Jones show just that, with earnings forecast to plunge by 30% in 2020 to $109.48, and then snap back in 2021 by 47.5%, to $161.51.

Shifting Outlook

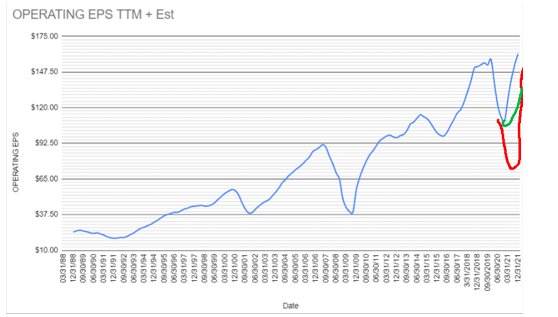

In my opinion, this profit outlook will need to change in one of two ways. Either earnings for 2020 will need to fall even further, or estimates for 2021 need to be pulled lower, creating a more extended recovery period.

I attempt to show in this rough drawing below. The reason for this is simple: Texas and Florida have started to walk back their reopening processes. Other states, in my view, will follow if new virus cases continue to rise.

If earnings estimates for 2021 are too upbeat, then the market will need to start repricing the possibility of that and that likely means lower stock prices, according to my research.

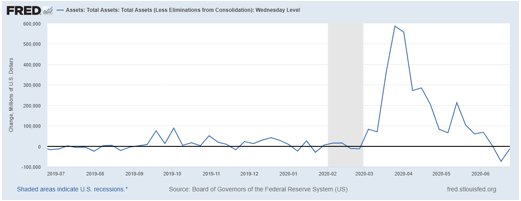

Fed Balance Sheet

The other issue, in my opinion, is that the US Federal Reserve’s balance sheet has contracted for two weeks in a row.

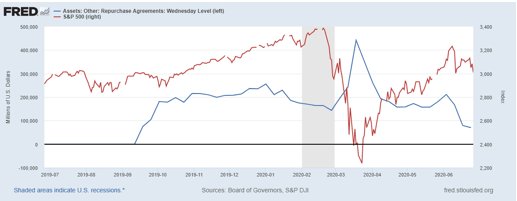

The reason for the decline is because the Fed is reducing its repurchase operations (repo). Notice that repo activity started to slide off the week of June 3, and stocks have steadily declined since that week.

In my view, it’s also significant that the market bottomed and began to recover the week after the Fed started its massive repo programs, and topped as the repo programs have slowed.

This is precisely how the Fed’s liquidity program has helped to fuel the market’s rise. This is how the Fed adds and drains liquidity from the banks. If the liquidity is declining, and should it continue to decline, it is likely to add yet another headwind to the market.

These are two pieces of the bull narrative that need to be monitored very closely in my opinion.

Photo Credit: herval via Flickr Creative CommonsMott Capital

Management, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Past performance is not indicative of future results.

{kind=link}