By Chelsea Rodstrom, Research Analyst, Global X ETFs

Sluggish global growth and dovish monetary policies, paired with trade tensions, uncertainty around Brexit, and other regional geopolitical tussles in the Middle East and Asia, have prompted many investors to pivot towards more defensive assets. Accelerating flows into gold and silver funds, fixed income, and US-based assets, demonstrate a more risk-off environment in Q4. Yet while many of these perceived risks stem from a global macro-economic slowdown and a trend of greater geopolitical tensions, we believe there are selective opportunities abroad that have reduced vulnerabilities to these factors or have more attractive growth prospects.

Targeted Opportunities

Europe: Stagnating growth is roiling European markets this year, which are now set to face additional headwinds as the US imposes WTO-supported tariffs for illegal EU subsidies given to Airbus. Prior to the WTO ruling, US policymakers and the ongoing US-China trade war were two culprits of mounting pressures on other major European industries such as the auto industry in Germany and the wine industry in France, dampening economic data across the region. And while macro weakness and trade tensions continue to spread across Europe, there are pockets of opportunity for investors allocating to the region.

- Greece: In the euro-zone, Greece’s economic recovery continues to stand out. Despite the backdrop of a weak Europe, manufacturing continues to rebound into its 27th consecutive month of expansion.1 Unemployment is falling and GDP recovering steadily, while tourism booms, and the financial sector slowly regains its health. After a strong start to 2019, Greece still maintains its spot as the best performing emerging market.2 Greek equity markets rallied after the market-friendly New Democracy government took over for Alexis Tsipras’ Syriza party, and over the last month yields on short term Greek bonds turned negative, suggesting that investors are becoming increasingly confident in Greece’s prospects. Yet, despite the progress made in Greece thus far, further progress is needed for a full recovery. Ample runway is left for Greek markets to return towards pre-crisis levels – which makes valuations particularly attractive.

- Portugal: As with Greece, Portugal’s bond markets heated up over the last month after its sovereign bonds yields also dipped into negative territory. Attraction to Portuguese debt is in part owing to its ongoing economic recovery and improved financial health. Similar to Greece, but a few years ahead in its recovery, unemployment levels are beginning to normalize. And while progress in both countries continues to be made on reducing non-performing loan (NPL) exposures, Portugal is further along. This makes sense given that it experienced its contraction earlier. Perhaps benefiting these two countries, however, is that amidst external pressures, Portugal and Greece benefit from being somewhat insulated from broader trade tensions, with most of their exports destined for other EU-countries rather than US or Asian destinations.

- Nordic Region: Euro-centric investors may also look to the EU’s northerly neighbors if they are looking to maintain their European presence but mitigate their exposure to a slowdown or trade sensitivities in the Euro-zone. The region benefits from being relatively insulated from the trade and political tensions hurting broader Europe – and could potentially even benefit from some of it as Nordic technology and communications firms become favored over their Chinese competitors within US and European policy circles. Firms in these countries may stand to benefit from global government-sponsored infrastructure contracts. And when considering narrower country-exposure, Norway may offer the added benefit of higher correlation to oil prices without OPEC membership, thus benefiting from less sensitivity to geopolitics in the Middle East and price or output controls imposed on member countries.

Latin America: Policy uncertainty related to Brazilian pension reform, concerns with reversals of Mexican energy and education policy, or Argentine elections, contributed to an overall weaker outlook for Latam. But external pressures also dampened regional growth, with US-China trade tensions weakening commodity prices and reducing exports. Likewise, fiscal consolidation throughout the region is still needed, given high debt levels in Brazil and in Argentina.

- Colombia: Progress in Colombia over the last 10 years has been thoughtful and steady, and this gradualist approach has allowed the country to overcome challenges associated with its legacy of civil conflict and oil market volatility. With higher expected GDP levels and lower inflation compared to Latam on average, Colombia remains a bright spot. With a stable political climate, pending reforms, and planned infrastructure projects, Colombia continues to stimulate investor interest in a region replete with promise, but rife with missteps.

Asia: Although growth in China has begun to slow due to structural changes in the economy and the headwinds faced by US-China trade wars, the country is still projected to experience growth around 6%. This is slower, but still high compared to the US or Europe. Across the broader Asia Pacific region, growth has also slowed, but not in tandem across each country. In some countries – including ASEAN members Vietnam and Indonesia – growth is resilient despite external headwinds. With a combined GDP of $2.8 trillion, ASEAN refers to the Association of Southeast Asian Nations and is a free trade organization with some of the world’s fastest-growing economies among its members, including Indonesia and Vietnam.3

- Vietnam Despite contending with the negative impacts of trade tensions, the economy has been resilient, with GDP growth reaching a 10 year high of 7.1%.4 While growth is expected to be lower in 2019 at 6.5%, it is high on a regional basis, with the growth expectation of 4.6% in broader Southeast Asia. Fueling growth are Vietnam’s competitive labor costs and manufacturing capabilities, as well as an expanding middle-class driving consumerism on the demand side. Urbanization and reforms implemented by the Vietnamese government have also aided growth by expanding credit (in a prudently managed way), access to capital markets, and the private sector.

- Indonesia Despite being the largest economy in Southeast Asia, Indonesia has one of the highest growth rates in the region, with 5% GDP growth expected over the coming year.5 And although the economy faces headwinds related to trade, resulting in capital outflows in 2018, Indonesia has performed well, with falling net exports offset by domestic demand, credit growth, and responsive policy mechanisms. The outlook for Indonesia is also positive given the expected policy continuity given that the current administration just began its second term and has had a substantial reform agenda to improve infrastructure, streamline regulations in health and education sectors, allow greater foreign direct investment (FDI) and reduce the presence of state-owned-enterprises (SOEs) to boost competition and innovation.

Low Valuations can Provide a Tailwind in Lieu of Growth

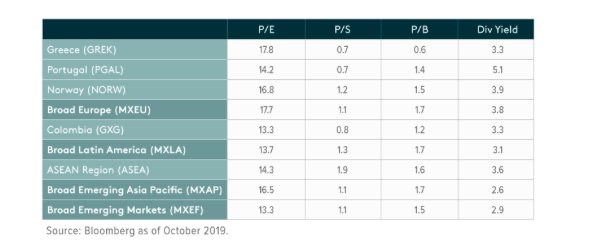

Despite the macroeconomic and geopolitical challenges facing the world today, many broad market indices are showing relatively full valuations. Some of this is attributable to the low interest rate environment, which has driven many investors to seek returns from equities over bonds, thereby pushing valuations higher for certain regions. Yet many of the bright spots highlighted above exhibit lower valuations than their regional benchmarks, adding to their appeal.

Relative to broader Europe, Greece, Portugal, Norway all exhibit comparable or lower valuations from a price-to-earnings (P/E), price-to-sales (P/S), and price-to-book (P/B) metrics. Similarly, Colombia and Southeast Asia exhibit lower valuations than their broad benchmarks. In a market environment with lofty valuations in many regions including the US and falling growth expectations, lower multiples can play an important role in contributing to returns should those valuations normalize, or dividends and buybacks support higher total returns.

Conclusion

With macroeconomic and geopolitical indicators flashing warning signs, it’s understandable that investors may seek safety and familiarity. Yet not all markets are impacted the same by these potential risks, and in fact many have attractive characteristics and valuations. We believe investors ought to consider a more selective approach to their exposure outside the US to capture such opportunities, or to avoid the risks that threaten broader benchmarks.

This article first appeared on the Global X blog on October 31.

Photo Credit: guido da rozze via Flickr Creative Commons

Disclosure:

Investing involves risk, including the possible loss of principal. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Securities focusing on a single country and narrowly focused investments may be subject to higher volatility. CHIQ is non-diversified.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. Global X NAVs are calculated using prices as of 4:00 PM Eastern Time. The closing price is the Mid-Point between the Bid and Ask price as of the close of exchange. Closing price returns do not represent the returns you would receive if you traded shares at other times. Indices are unmanaged and do not include the effect of fees, expenses or sales charges. One cannot invest directly in an index.

Carefully consider the Fund’s investment objectives, risks, and charges and expenses before investing. This and additional information can be found in the Fund’s summary or full prospectus, which may be obtained by calling 1-888-GX-FUND-1 (1.888.493.8631), or by visiting globalxfunds.com. Please read the prospectus carefully before investing.

{kind=link}