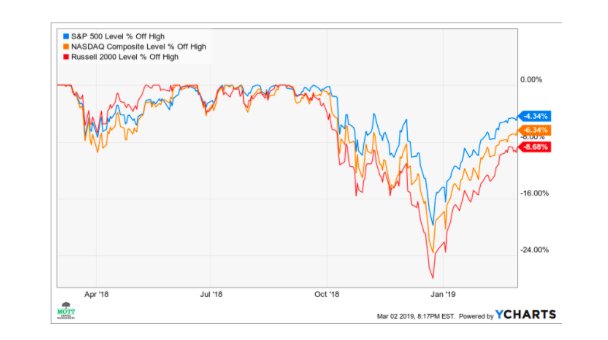

Stocks continue to perform well and have mounted a sizeable come back since the December lows.

At this point as of March 2, the S&P 500 Index is less than 5% off from its all-time high, while the NASDAQ and the Russell 2000 are roughly 6% and 8%, respectively, off their tops.

It is yet to be seen if the indexes can manage to reclaim their earlier highs.

Upside Potential

Despite earnings estimates declining, in my opinion there’s more room for positive stock market gains in 2019 and 2020.

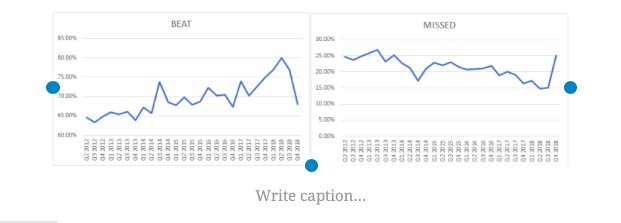

The fourth quarter earnings season has turned out to be one of the worst in some time in my view.

With 96% of companies having reported results as of March 2, 68% of them have beaten, while 25% have missed, and only 7% met.

The last time we saw results this bad was in the fourth quarter of 2016, when 67% of companies beat estimates and 22% missed, while 11% met.

Good News

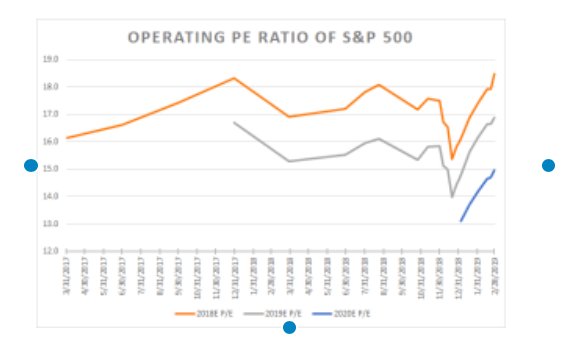

But, in my view, there’s a hint of good news: The S&P 500 is still trading at less than 15 times 2020 earnings estimates.

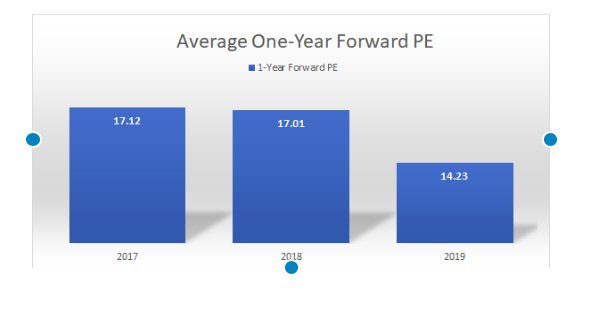

The next chart below shows how the PE ratio versus 2020 estimates is well below the historical norm of the past two years.

Valuation Shift

In fact, in 2017 the S&P 500 averaged a one-year forward PE ratio of 17.1 times 2018 estimates.

In 2018, the S&P 500 averaged a one-year forward PE ratio of 17 times 2019 earnings. This year the average is just 14.2.

Takeaway

Assuming the S&P 500 reaches its historical multiple of about 17 times 2020 earnings estimates, in my opinion the S&P 500 could rise to roughly 3,186.

If we assume earnings estimates for 2020 fall by 10% from their current levels, it will send the forecasts down to $168.66 per share leaving the S&P 500 trading at 16.6 currently.

At the very least in my view, we could probably assume at this point that the S&P 500 is fairly valued.

And, in my opinion, should the earnings outlook for 2020 stabilize, then one could argue that stocks are very cheap.

Photo Credit: Wonderlane via Flickr Creative Commons