Last year, the White House Council of Economic Advisers issued a stinging criticism of US financial advisers.

The White House economists estimated that some $17 billion in potential retirement savings for US families each year is wasted.

More to the point, the Obama Administration claimed that some financial professionals with conflict-of-interest issues charged excess fees that undermined returns for their clients.

Fiduciary Standard

Now, the US government is about to issue new regulations on stock brokers that will have big implications for the way Americans manage their money, according to the Wall Street Journal.

The US Labor Department will soon issue final regulations, requiring “brokers getting paid to provide investment guidance on a retirement account to act solely in the best interest of the investor.”

In other words, they will have to meet a fiduciary standard.

Excess Fees

In the past, brokers have only had to meet the less stringent standard of making sure their recommendations were “suitable” for clients.

Critics say that lower bar encouraged some advisers to charge excessive fees.

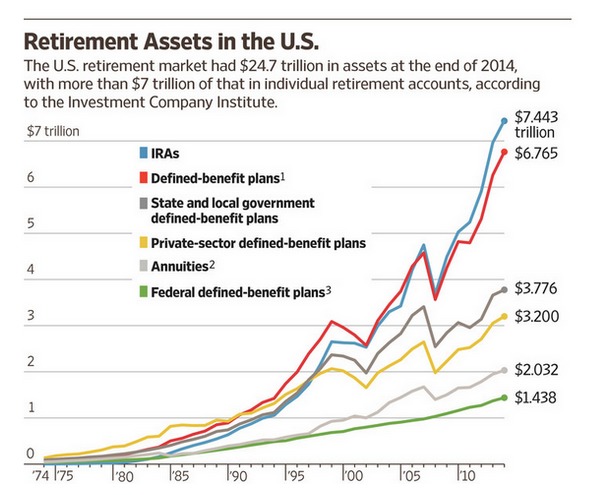

According to an analysis by Morningstar, the move will impact $3 trillion of retirement assets and $19 billion of revenue in the financial services industry.

Changes Ahead?

What does this mean for investors?

The Wall Street Journal reports that the new rule won’t ban commission-based sales.

However, experts believe financial advisers offering retirement financial advice for IRAs and 401(k)s will face higher administrative costs and might be incentivized to charge a fee for advisory services.

In its report, Morningstar predicts wealth managers may also convert commission-based IRAs to a fee-based compensation structure to better comply with the new rule.

Takeaway

Investors need to be vigilant and spend just as much time scrutinizing the fee structure of the investment as they do do calculating risk and potential return.

It requires a frank discussion in coming months with your investment adviser to understand the new regulatory environment and to make sure you’re getting straight answers about fees.

Photo Credit: 401 (K) 2012 via Flickr Creative Commons

{kind=link}