The S&P 500 index returned +0.28% in the second quarter of 2015 compared to +5.23% in the same quarter last year.

The second quarter results were negatively impacted by the intensifying debt crisis in Greece when Prime Minister Alexis Tsipras announced a referendum to vote on the strict austerity and reform measures demanded by its creditors.

A resounding “no” vote by the people of Greece has now set the stage to a dangerous path that could lead to Grexit (the exit of Greece from the Eurozone monetary union).

China Rout

Also contributing to the second quarter malaise was the free fall in Chinese stocks to bear territory.

While the drama in Greece may not rock to boat much, I believe the situation in China could be a different story. Why?

Because the Greek economy is dwarfed by China’s. To put things in perspective, the Greek and Chinese economies amount to 0.3% and 13.3% of global GDP, respectively.

Dim Outlook

With the stock market as a leading indicator of what to expect of their real economies, the current outlook for China and Greece appears to be from bad to worse, respectively.

Additionally, with many markets trading at or near historic highs, now seems to be a good time to prepare for the next downturn in my opinion.

Over the past seven years, unprecedented accommodative monetary and fiscal policies have lifted asset prices from the precipice, but also have pushed some government finances to the brink.

Side Effects

In other words, the economic stimulants injected may have saved the patient, but also may have unintended side effects and consequences.

In this higher stock and bond price environment, there appears to be limited places to hide.

But with bonds falling in the past five months and commodities in the past year, I believe now looks like a good time to consider these two beaten down assets.

Treasuries

However, given the deflationary pressures in commodities as a result of the debt crisis in Greece and stock meltdown in China, I believe U.S. Treasuries may outperform most every other assets worldwide over the foreseeable future.

With a return on investment as well as a return of investment, holding bonds to maturity seems to be a better choice in my opinion compared to commodities.

It’s also worthy to note that Bill Gross of Janus Capital Group said that Treasuries have fallen to fair levels. He said 2.30% is “fair value.”

Portfolio Changes

In the second quarter, the largest change in the Prudent Value portfolio was replacing one low-yielding short-term corporate bond ETF with four laddered intermediate corporate bond ETFs; the Guggenheim BulletShares 2021 Corporate Bond ETF (BSCF), Guggenheim BulletShares 2022 Corporate Bond ETF (BSCM), Guggenheim BulletShares 2023 Corporate Bond ETF (BSCN) and the Guggenheim BulletShares 2024 Corporate Bond ETF (BSCO).

The extension of maturity and duration of the bond ETF portfolio increases the yield as well as interest rate risk.

The default risk remains unchanged with investment-grade corporate bonds held in the ETFs.

Corporate Bonds

In other words, the portfolio will experience higher bond interest earned along with higher sensitivity to interest rate volatility.

Additionally, the risk of capital loss is low provided that the bond ETFs are held until maturity.

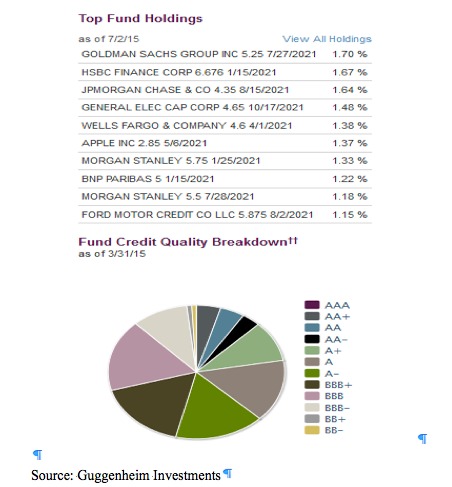

Below is BSCL’s Top Fund Holdings and Credit Quality Breakdown:

As we enter the third quarter and beyond, Prudent Value aims to protect capital first and create long-term equity-like returns second as the situation in Greece and China plays out.

Photo credit: Michael Arrighi via Flickr Creative Commons

The investments discussed are held in client accounts as of July 15, 2015. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.

{kind=link}