The explosive rallies at domestic exchanges in China are reordering the global pecking order among stock markets.

The Shanghai Composite Index is up nearly 80% over the last 6 months.

Dragon Rally

And, all told, some $4 trillion has been added to the total market value — now $7.3 trillion — of companies listed on all of China’s domestic exchanges over the past year.

That’s having a big impact on stock valuations around the world.

Do a stock screen of companies by market capitalization and you will see three Chinese companies in the top 10 as of April 28.

China Rises

Apple (AAPL) is still tops with a $722 billion market value. No. 2? It’s no longer ExxonMobil (XOM) but PetroChina (PTR) at $403 billion.

Further down the list, No. 7 and No. 8, are China Mobile (CHL) and Industrial and Commercial Bank of China (IDCBY), whose market caps each exceed $300 billion.

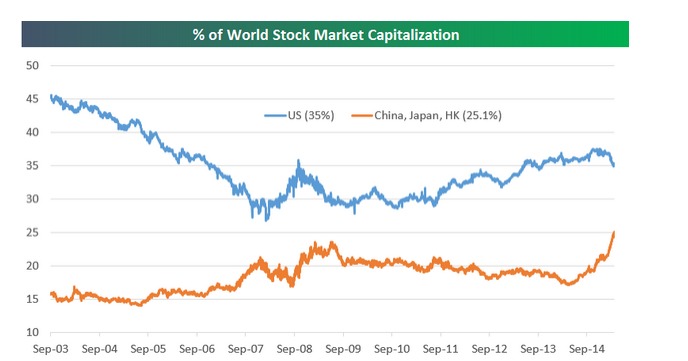

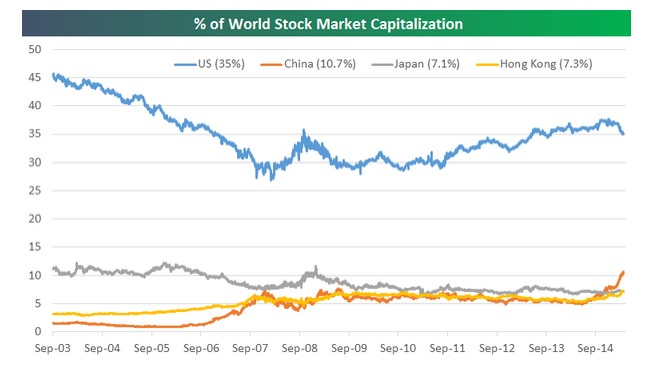

At the start of the year, the U.S. stock market made up more than 37.5% of total world stock market capitalization, according to an analysis by Bespoke Investments. Now, it’s 35%.

Asian Clout

If you take Asia’s three biggest stock markets — mainland Chinese exchanges in Shenzhen and Shanghai, Tokyo and Hong Kong–a more dramatic picture emerges.

In terms of percentage of global stock market capitalization, Asia is starting to converge with the U.S.

The total U.S. stock market capitalization still rules on a country-to-country basis.

However, its global share has fallen about 10 percentage points if you pull out the wide-angle lens and go back to 2003.

Takeaway

The days when US stock exchanges dominated global finance are long gone.

A rip roaring bull market in China has boosted the market capitalizations of the country’s major multinationals.

For a growing share of global investors, Asia is just as important as the US.

Photo Credit: Wilson Hui via Flickr Creative Commons

The investments discussed are held in client accounts as of April 29, 2015. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.

{kind=link}