What a challenging year. The S&P 500 Index started the year at 1848.36, which was a high for 2013. By mid-October of 2014, the index had traded down to 1820, over 1% off its 2013 high.

Furthermore, starting the fourth quarter, the world economy showed signs of trouble. China was telegraphing a slowing economy, with GDP figures nearly 1% off last year’s projections.

Geopolitical tensions

Russia was back to its Cold War self, seizing control of Crimea from Ukraine. Israeli and Palestinian tensions were at extreme highs, with almost daily reports of fighting and deaths.

Europe was confronting issues with Greece, again, as well as slow growth across the eurozone. The ISIS challenge in Iraq and Syria was unfolding with yet more beheadings, fighting and a renewed interest by America to maintain ground troops there. Then oil prices began to fall… fast.

The U.S. Federal Reserve continued to signal its measured approach to raising rates and later modified its language in policy statements to hint strongly that day is coming.

Yet, bond markets didn’t panic. Yields fell as investors snapped up bonds. Flight to quality? The bond market is painting a nervous picture for the future.

This was the picture on October 15.

Oil dividend

Then, things changed. The mood in the US suddenly improved. Unemployment seemed better, prospects of cheaper energy were good, growth was solid again, especially when compared globally.

This turnaround in attitude from the middle of October sent the markets up again, and the S&P 500 ended the year at 2058.90. Up over 13% from October 15th, and a gain of 11.3% for the year when looking at price.

So, 2014 witnessed a solid, double digit equity market, and a continuation of the prior few years of good equity market returns. But, the gains were choppy, and didn’t follow the logic we at Rockledge expected.

This led our Rockledge Covestor L2 portfolio to end the year up 8.6% versus the 13.69% return by the S&P 500.

Healthcare

The portfolio’s holdings in the Health Care Select Sector SPDR Fund (XLV) performed well in the year, though we missed a big run in the middle of 2014.

Our position in technology with the Technology Select Sector SPDR Fund (XLK) also gained ground.

On the negative side, the roughly 50% decline in oil prices hurt our investment in the Energy Select Sector SPDR Fund (XLE).

Other underperformers were the portfolio investments in Industrial Sector Select Sector SPDR Fund (XLI) and the Material Sector Select Sector SPDR Fund (XLB).

Rebalance

We rebalanced the portfolio in the middle part of the year, another detriment to performance.

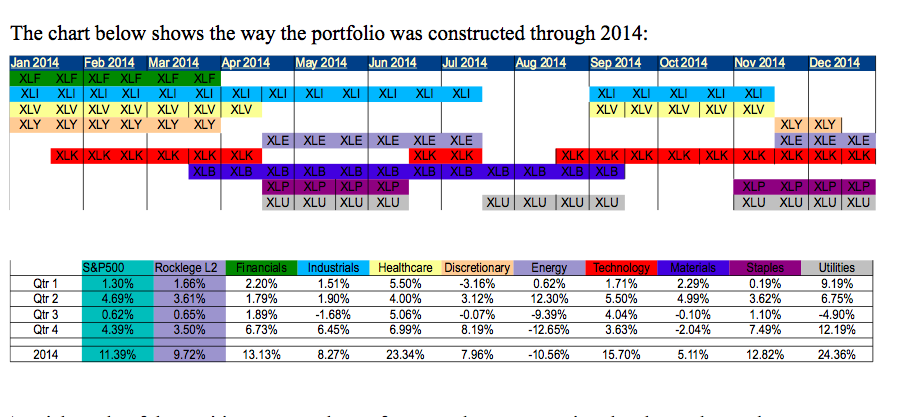

A quick study (chart below) of the positions versus the performance by quarter using the charts above, demonstrates how performance on Rockledge L2 was compiled.

Stay focused

Looking forward, Rockledge believes there may be more of the same ‘event’ driven issues that will impact the markets.

In our opinion, this suggests that using a sector focused strategy will likely yield better results than a stock picking strategy going forward.

We feel that we have a better chance to pick three sectors out of nine than to pick 30 stocks out of 500.

Furthermore, we believe that the markets will adjust to being more fundamentally driven than they have been. Earnings will again be important to valuation.

This past year, it seems that the rising tide lifted all the boats. This year the tide may not be as strong, or perhaps it may ebb.

Photo Credit: Dougtone via Flickr Creative Commons

DISCLAIMER: The investments discussed are held in client accounts as of December 31, 2014. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.