How high will stocks fly? A friend of mine recently asked me that question. To his surprise, I answered: “I don’t know. It is not relevant for me.”

I only need to know that the price of financial assets sometimes moves in trends and then ride it as long as the trend persists. Momentum is the modern cousin of trend and basically describes the same anomaly. The Active Momentum and Technical Swing portfolios try to capture the effect and have therefore benefited from the strong equity market environment in June.

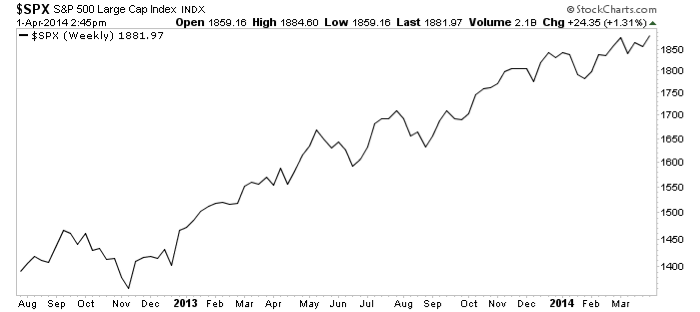

The resilience of stocks this year has been surprising. Important sentiment indicators flashed strong warning signs last quarter, which prompted us to be defensive in the Technical Swing portfolio and was reason for underperformance so far this year.

High Beta stocks, which tend to be very sensitive to broad market movements, performed sluggishly during the first months of the year, but had a very strong comeback in June. The PowerShares High Beta Portfolio ETF (SPHB) tells the story: from January until May, SPHB traded flat. However, from mid-May until the end of June, the ETF gained almost 10%.

The performance of the iShares 20+ Year Treasury Bond ETF (TLT) may be instructive in the coming months. Interest rates have been declining during the first half of the year, which is why TLT gained around 13%.

However, interest rates seemed to initiate a trend reversal. If the US economy is indeed gaining traction, TLT should be under pressure in coming months. The Technical Swing portfolio currently owns the ProShares UltraShort Lehman 20+ Year Treasury Bond ETF (TBT), the inverse ETF to the iShares product in order to participate in this trend.

Fundamentally, a trend towards higher interest rates make sense: ADP employment data for example came in much stronger than expected on July 2. Global manufacturing numbers are in expansion mode. It will be interesting so see how stocks will master this possible theme change. Should economic strength continue, we might hear more hawkish comments from U.S. Federal Reserve figures.

Stocks have been resilient, but they are also overbought and a minor three to five percent correction could happen anytime. However, given the low interest rate environment, investors have not many alternatives to owning stocks, even if the 10-year Treasury yield should move from currently 2.5% as of July 3 to over three percent. As a reminder, in 2006 before the Financial Crisis when stocks did well, the 10-year yield was hovering around five percent.

DISCLAIMER: The investments discussed are held in client accounts as of June 30, 2013. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.

{kind=link}