I have long been leery of September markets, as everyone leaves the beaches and countryside of summer vacation behind and heads back to work in a quasi-dazed state of mind.

It’s almost as if we haven’t awakened from a deep slumber quickly enough and are soon forced to make intelligent decisions before we really should. The kids head back to school, or off to college, and emotions jump on a roller-coaster of highs and lows.

The kids will finally be out of your hair, but yet another summer has slipped by and they are another year closer to leaving the nest for good. Although the ‘highs” seem to be on a trend line that has some real staying power, the ‘lows” begin to fade away pretty rapidly!

I just hope this roller-coaster stays on the boardwalk and doesn’t land in the ocean. I know October has certainly had its moments in the past as well, and frankly the next eight to ten weeks look to us like we should be prepared.

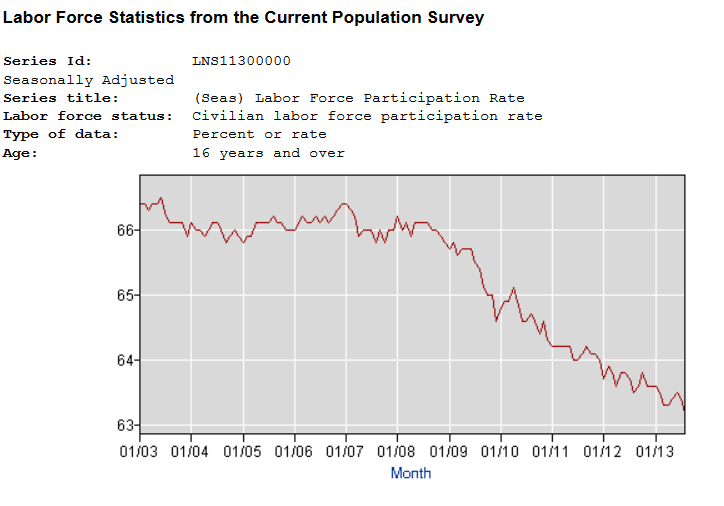

The August Employment numbers are really not even a mixed bag. The headline number came in at 7.3% unemployment, off .01 the prior month, which is good, but the actual number of nonfarm workers hired was 169,000 versus the consensus of plus 180,000.

Additionally, the previous month’s number of non-farm workers hired was revised down by 58,000 to 104,000 (-35%), which is not so good. Perhaps they added a couple of states twice, given the size of July’s revision.

Now more bad news, the Labor participation rate, the number of people who have a job or are looking (63.2%), dropped to its lowest point since 1978 and its estimated more than 300,000 people are just not looking for work.

This is not a good thing and would hardly seem to be the political “cover” necessary for the Fed to truly begin to taper back their bond purchasing program in September, an idea originally floated back in May. Given the volatility in the global, bond markets, domestically, and the carnage seen in some emerging markets, it just doesn’t seem like the right time.

This just isn’t a good commentary about the strength of the US Jobs market and therefore a September “tapering” of the Fed’s Bond purchasing program would seem to be premature and potentially risky. (On September 18, the Fed decided not to dial back its stimulus effort.)

Corporate debt is making a big comeback: Consider that Sprint (S) issued $6.5 billion in junk bonds and Verizon (VZ) is about to issue the largest bond sale ever, some $49 billion to finance the purchase of its stake from Vodafone.

In my opinion, Apple’s (AAPL) CFO Peter Oppenheimer is still the king of bond market timing, issuing $17 billion in Apple bonds on April 30, just as the yields on the 10-year bonds touched lows (about 1.67%) for the year.

Other factors keeping us on the edge of our seats this fall: obviously Syria is the number one wild card now. It is hard to know whether the agreement between the U.S. and Russia to transfer Syrian chemical weapons to international authorities will work.

Washington gridlock has been off the front pages for a while now as the world wrestles with Syria as the headline issue. I haven’t been feeling optimistic about the policy challenges in Washington: spending gaps, sequestration, debt ceilings, or potential tax hikes. It would seem like the pressure has only one way to go: up. Remember we came to the brink of disaster and then went through a downgrade? The current situation just doesn’t appear to be heading to a good outcome.

Also, how badly is the nomination of the next Federal Reserve chairman going? Shouldn’t President Obama be making a sincere effort for this to go smoothly; how about controlling the situations you can?

We are just stunned, the Middle East is in chaos, luckily Egypt and Libya have settled down a bit, but seriously you could not have scripted this any worse. This is potentially the most important person in the financial universe, every single gesture or facial expression of the guy in this job has been known to move markets.

So “handing over of the reins” of this powerful position should be done with aplomb; this should really be the easy stuff. Larry Summers, a top economic advisor to President Obama, has withdrawn his name from the running and the current frontrunner is Janet Yellen, Vice Chairwoman of the Fed’s Board of Governors.

Given her current role, six years as the president of the San Francisco Fed, and a past chair of the Council of Economic Advisers under President Bill Clinton, she is extremely qualified. Essentially an educator and public servant for her career whereas Summers has always been willing to leverage any public service role to his advantage in the private sector.

Microsoft (MSFT) is back in the news thanks to CEO Steve Ballmer’s planned retirement; the stock got a good pop off that before realizing that the planned $7.2 billion purchase of Nokia’s mobile phone business was perhaps not the best thing to be leaving your successor.

The deal increases the payroll by 32,000 employees and increases operating costs by about $19 billion annually. Of that total price, Microsoft is paying $2.18 billion for licensing Nokia’s patents. The deal lasts just ten years and doesn’t prevent Nokia from pursuing other deals, as reported by Techdirt.

We are not so sure the windows mobile phone operating system will threaten Android too quickly, and we hope this doesn’t later become a complete write off, like the $6.3 billion invested in aQuantive in 2007.

Nokia has introduced a new smart phone, the Lumina 1020, which comes with a super high resolution (41 mega-pixel) camera built in. The camera also offers a number of on-phone (camera) adjustments to help manipulate and crop your image, and costs about $100.00 more than other smart phones.

The phone is destined to be popular with photographers hoping not to drag their cameras with them everywhere. Any case, I trust the patents will produce enough income longer term, to at least partially offset the cost to Microsoft and the “new” hardware /software combination will help push their mobile technology to the next level. Microsoft will also acquire Nokia’s long-term license with Qualcomm for chip technology which should help.

.

Courtesy of Bloomberg

There are bright spots in the U.S. economy: US Automobile sales were up 17% year over year in August, and the housing market, despite the recent uptick in mortgage rates, is still doing well.

I still believe housing will be supportive of the US market going forward, perhaps at a bit more moderate pace, but supportive nonetheless.

The current situation regarding mortgage rate increases, I believe will serve to push many off the fence, and commit to a mortgage at current rates. In my opinion, we are at the end of a 30-year bull market cycle in interest rates, so even a move up of ¾ point of your mortgage rate will still represent a great rate historically.

These two engines of our economy seem to be chugging along and now that the economic data out of China is improving, I believe the global economy may stabilize. However, in my opinion the budget issues in Washington are a risk to the outlook.

Another potential curve-ball might also be an election upset , or a very close call, for German Chancellor Angela Merkel on September 22.

The AfD party (Alternative for Germany ) has made some inroads and if they draw 5% or more she may have to form a coalition, opening the door for some leftists in government.

We expect US market professionals to ride this domestic equity bull as long as possible. But remember they will not be willing to gamble their 2013 bonuses on it – chips will come off the table in 2013, it’s just a matter of how and when. Be prepared.

The investments discussed are held in client accounts as of August 31, 2013. These investments may or may not be currently held in client accounts. Certain information contained in this presentation is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The manager believes that such statements, information and opinions are based upon reasonable estimates and assumptions.

{kind=link}